In my last “five drivers” update on May 1st, the Australian dollar was at 93 cents and pointing lower. Since then the dollar did fall to 92 cents but has now rebounded to near 94 cents after threatening but failing to break the 2o14 high at 94.6. At this stage the model still favours falls ahead. The five drivers are:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth);

- investor sentiment and technicals; and

- the US dollar

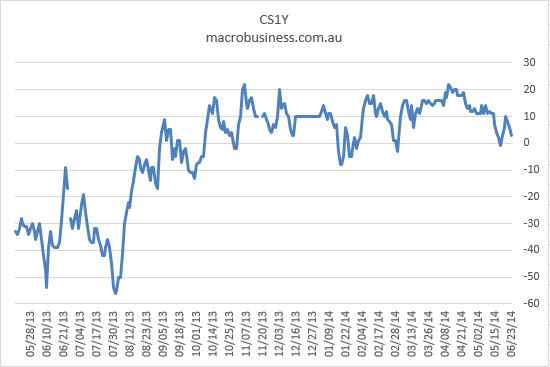

For the first, there is now no chance of local interest rate hikes this year with falling terms of trade, the capex cliff and a soft labour market already outweighing the bloom in activity in cyclical sectors. Indeed, the chance of another rate cut is rising as weakening local indicators mount up. Interest rate market conviction that that we’ll see rate rises in the year ahead has evaporated and they are pricing only 3bps, down from 13bps two months ago and in a down trend:

There is also mounting evidence that the Budget has created fiscal drag well beyond its direct impacts with a collapse in consumer confidence already felt in retail sales. A rebound can be expected but given the income cuts for households are permanent so to can a lower consumption path. Many economists are now discussing the return of the RBA’s easing bias.

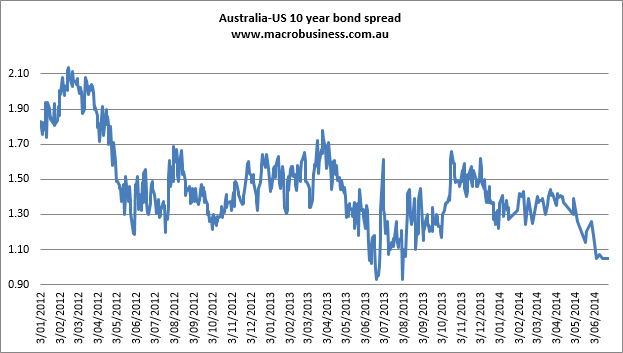

On the other hand, the rise in US bond yields that many expected this year has so far been cut short by the run of terrible economic data associated with a tough winter. However, in recent weeks US data has rebounded strongly and bond yields have stopped declining and have even risen again. The progress of taper appears on track and rate rises are a year away. That has meant that the carry spread between Australia and US ten year bond that rose this year has broken down and is currently sitting at 2014 lows:

With a repricing of rate cut chances locally still ahead it will compress further.

On driver two – global, local and Chinese growth – the jury is in. Global growth will accelerate this year but Chinese growth is going to slow over the next six months to 7%or so. Mini-stimulus has stabilised activity for the next three months but the ongoing housing shakeout will pressure growth again by Q4. Everything points to an ongoing cycle in which monetary and prudential policy is kept tight and fiscal policy lends targeted support. Property and steel are explicitly in the gun and infrastructure is expanding as an offset.

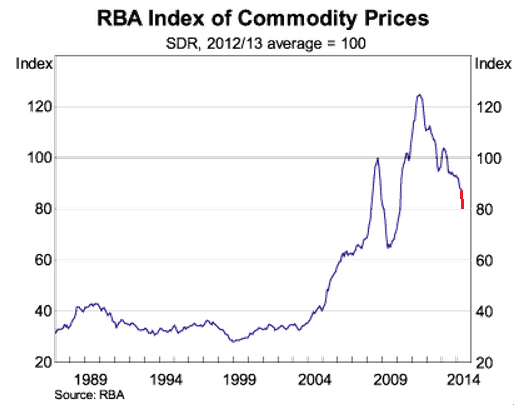

Australia’s terms of trade are thus under a lot of pressure. Iron ore has crashed to $90 and won’t rebound for long if at all. Coal has been smashed too and the falls in the terms of trade are close to “external shock” proportions already. My estimate of the falls in the ToT ahead as contract prices adjust is below (using the proxy of the RBA Index of Commodity Prices):

In Australian dollar terms, all bulk prices are near their 2012 lows.

Australian growth will follow suit. All things being equal, I expect another year of firmly sub-par growth, well under 3%, as the capex cliff, falling terms of trade and weak national income outweigh the cyclical forces of monetary stimulus.

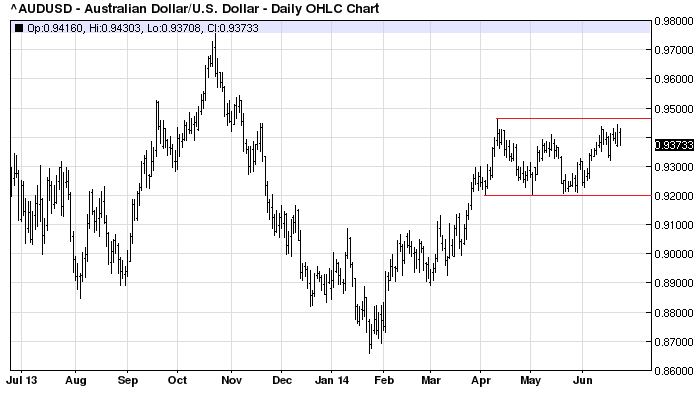

Drivers three and four, sentiment and technicals, look firmer. In technical terms, the Aussie has been range trading for several months between 92 cents and 94.4 cents. The breakout high is 94.6 cents which looks vulnerable this week but failed as US data marched in strong:

If either of these levels, up or down, breaks a bigger move is likely on. The weekly and monthly charts remain bearish.

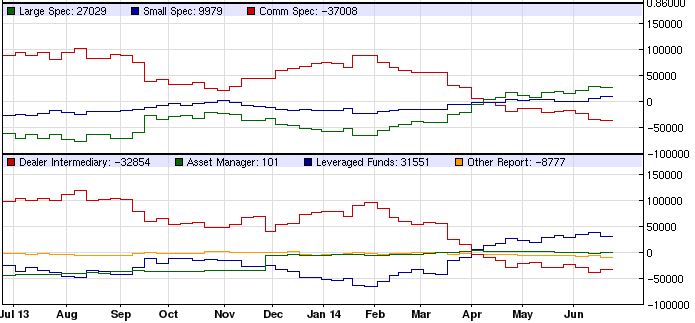

Turning to sentiment, the Commitment of Traders report is showing that the large and small speculators that control the market have continued to build longs. Exposure is still moderate and could rise further:

Adding to sentiment has been the jump in oil prices on geopolitical tensions, which Australia is seen to benefit from via the LNG pricing link. This is a medium term support that will slow declines in the ToT but LNG shipments rise only steadily over the next three years and ANZ shows the real impact is not real so much as sentiment driven:

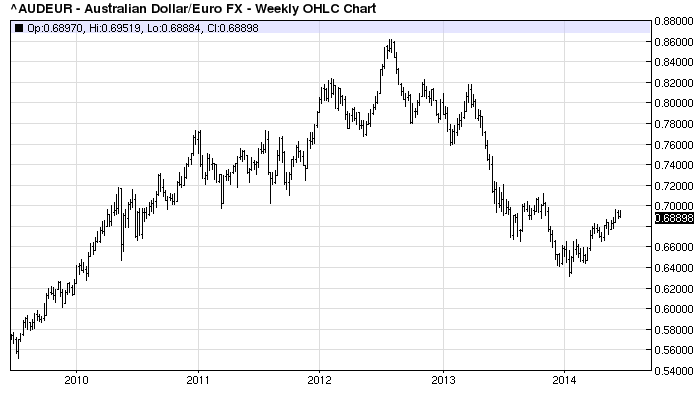

A minor support nonetheless. Another support to sentiment has been the push to negative interest rates in Europe. The euro is not an especially large funding currency for carry trades so that’s why I’ll call this a support to sentiment rather than an interest rate issue. The Aussie has been rising steadily as bearishness engulfs the euro and unlike against the Us dollar is already at 2014 highs around 69 euro. However the longer term charts are still a long way from any threatening recovery for the Aussie:

There is one other possible positive for sentiment. We know that central banks have been adding Aussie to there reserve portfolios for a few years. That has been a significant real support to higher valuations and general market sentiment around the currency. The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) report shows the accumulation was still aggressive in early 2013:

However, it is interesting to note that as the Aussie has regained its cyclical mojo and gotten cheaper, official buying has slowed to a trickle. That does not strike me as especially committed to the cause. Buying in the twin currency in Canada has remain much stronger. That’s not to say we’ll see a reversal in the holdings. But we aren’t seeing much in the way of bargain hunting either. This has not been updated since December.

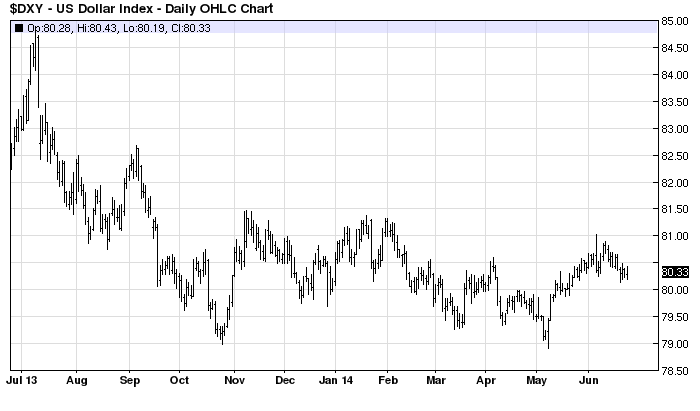

The final driver, the valuation of the US dollar, is also range trading. As growth improves through the year, taper continues and rate rises loom it should firm up though so far that has proved elusive and I think it fair to say that the Australian dollar can’t rely on a higher US dollar to weaken, especially if geo-politics keeps a bid under US bonds:

The upshot is that the conditions for Australian dollar weakness are there. The weakening of the drivers is most apparent in the fundamentals of Chinese rebalancing and local cyclical slowing which will bring the RBA back out of hibernation. The broader financial bullishness for the Aussie emanating from weak US and EU interest rates over time is still there but that should weaken over time as the global shift from emerging market growth to developed goes on.

Could it go higher in the near term? Sure. But my long term view remains unchanged – downside first to 80 cents and then lower again – given I see no real recovery in Australia until its below 80 cents permanently. I’ll concede it’s frustratingly slow but that will only ensure the ultimate falls are deeper and longer lasting as the damage is repaired.