US liquefied natural gas exports won’t be cheaper for Asian customers than LNG that can be supplied from Australia, according to Santos chief executive David Knox.

In a speech in Brisbane on Thursday Mr Knox is set to paint a bullish picture of prospects for Australian LNG exports, playing down concerns that Australian exports could be priced out of the market because of cheaper shale gas-based exports from the US.

Mr Knox said that with US benchmark prices, known as Henry Hub, set to reach $US6 or $US7 per million British thermal units by the end of the decade, costs for processing and shipping, plus a margin for trading, would bring the price of LNG once it reaches Japan or Korea to about $US14-$US14.50, close to prices for conventional LNG based on oil prices.

I agree with that for the very long term (2020s). $14 delivered to Asia looks about parity to me, after a period of lower prices around 2018. It means Santos will make no money, given its the swing global producer at that price, but in the mean time hey, hey!

Late last week the US Department of Energy, that body that controls the export applications of energy firms, announced a new streamlined process to accelerate LNG export approvals. From Politico:

Advertisement

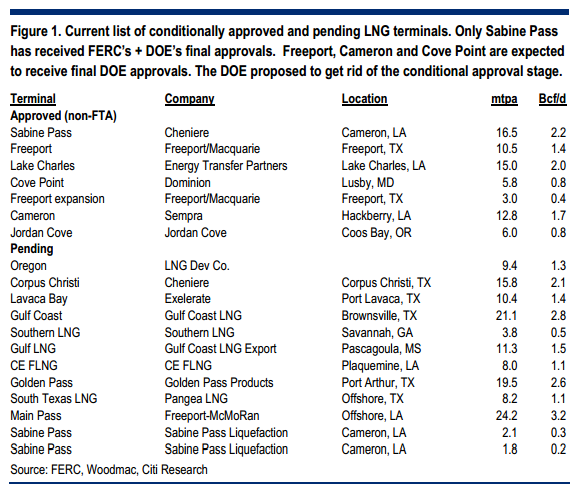

Amid heavy pressure from energy companies and lawmakers to speed up approvals of LNG export permits, DOE announced Thursday it planned to streamline its evaluation process. DOE plans to stop issuing conditional approvals for proposed liquefied natural gas plants before environmental reviews have been completed, and the agency will now issue that permission once a project makes it through a rigorous FERC process. But industry advocates say the changes will muddy the waters on LNG exports.

In the short term there may be more delays as applicants re-apply but the new system is clearly designed to get more LNG into the international market more quickly and will do so over the medium term. One of the driving rationale’s for an expedited process is a growing energy cold war with Russia and push to ensure its gas leverage does not grow any further.

Citi has a useful note today explaining that geo-political framework:

Advertisement

The US Department of Energy’s proposal to simplify the LNG export approval process and conduct two studies on the impact of exporting 12 to 20-Bcf/d of LNG could well accelerate and raise LNG exports post-2018. Before this, Citi expected 8 to 10-Bcf/d of LNG exports by 2020. The high cost of an FERC review as the first step of the overall approval process effectively changes the queue on approvals advancing the prospects of firms with strong financing/marketing backing.

We believe the new geopolitical jockeying between US and Russia could be fought over energy exports but Russia may be acquiescing so far. After the Gazprom deal with China, eroding the oil link in pipeline exports, the firm moved to shore up its European customers, conceding to ENI by giving a price reduction and an “important change in the price indexation.” Russia might now race to secure more markets before the global market temporarily saturates, especially with surging volumes from Austrlia. The loosening of US gas export rules could foretell the US’s stance on oil exports. Energy importers/overseas end users should be winners. The US may have a more credible strategy: it is cheaper to develop US’s export infrastructure than Russia’s Eastern Gas Strategy.

A rise in US gas prices looks inevitable but likely limited while global LNG prices should fall more. US prices in the $5 to mid-$5/MMBtu range should boost supply from Haynesville/Barnett. But global LNG prices could fall to the low end of the $11 to $14 range, near the delivered cost of Russian gas and US LNG into Asia.

The Australian resources manager handbook is quite clear. Over-estimate emerging market demand, assume no supply response, massively 0ver-invest and cash out while the equity market is drunk on capital flows, then deny, deny, deny as prices collapse along with your returns on equity and blame guv’ment for your shitty margins. You name the commodity.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.