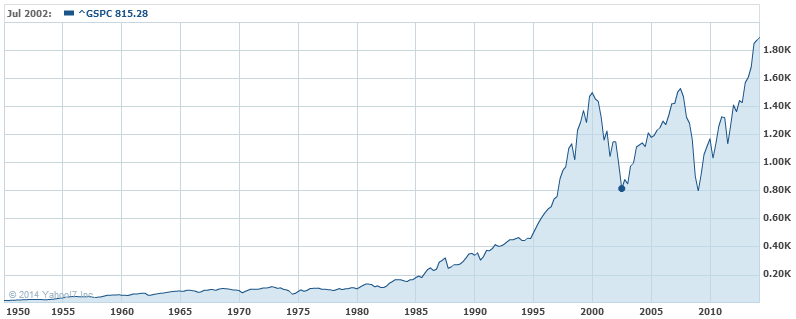

The S&P500 managed its first ever close above 1900 on Friday night:

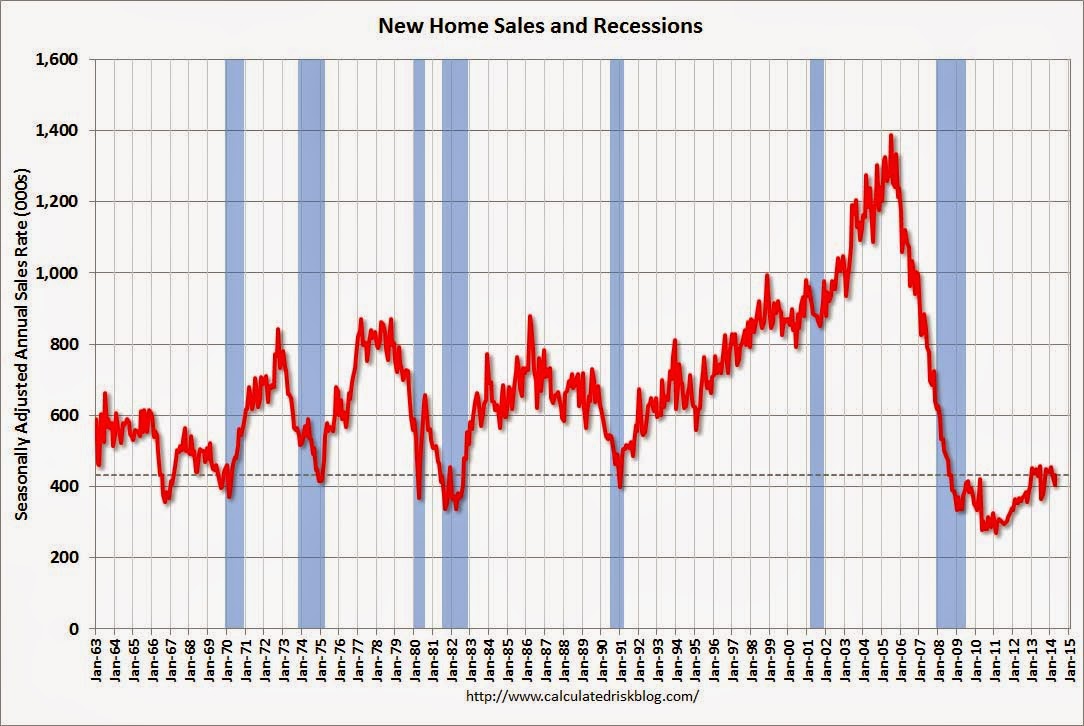

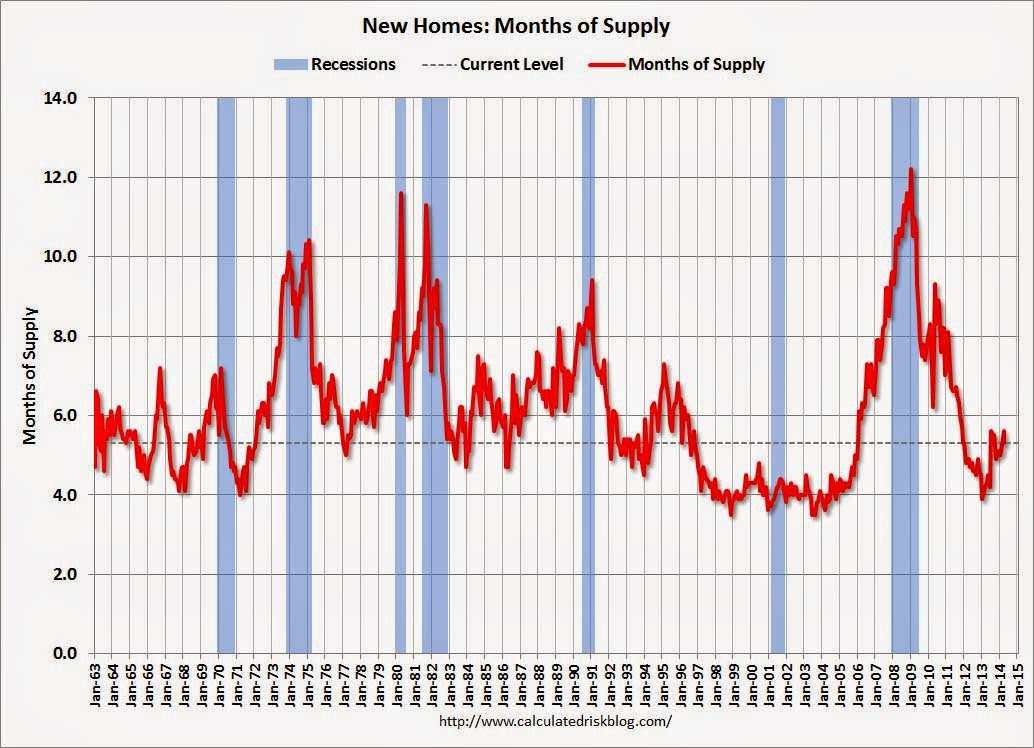

As a quick aside, I don’t know how anyone can look at this chart and not marvel at the recurrent bubbles that have defined our era in finance! But that aside, the new highs hit again on the S&P Friday night had little to do with an improving economy. On the contrary, the only data out Friday was new home sales and they were fair at best:

Sales of new single-family houses in April 2014 were at a seasonally adjusted annual rate of 433,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 6.4 percent above the revised March rate of 407,000, but is 4.2 percent below the April 2013 estimate of 452,000.

A little winter thaw but still down year on year even if above the 420k expected.

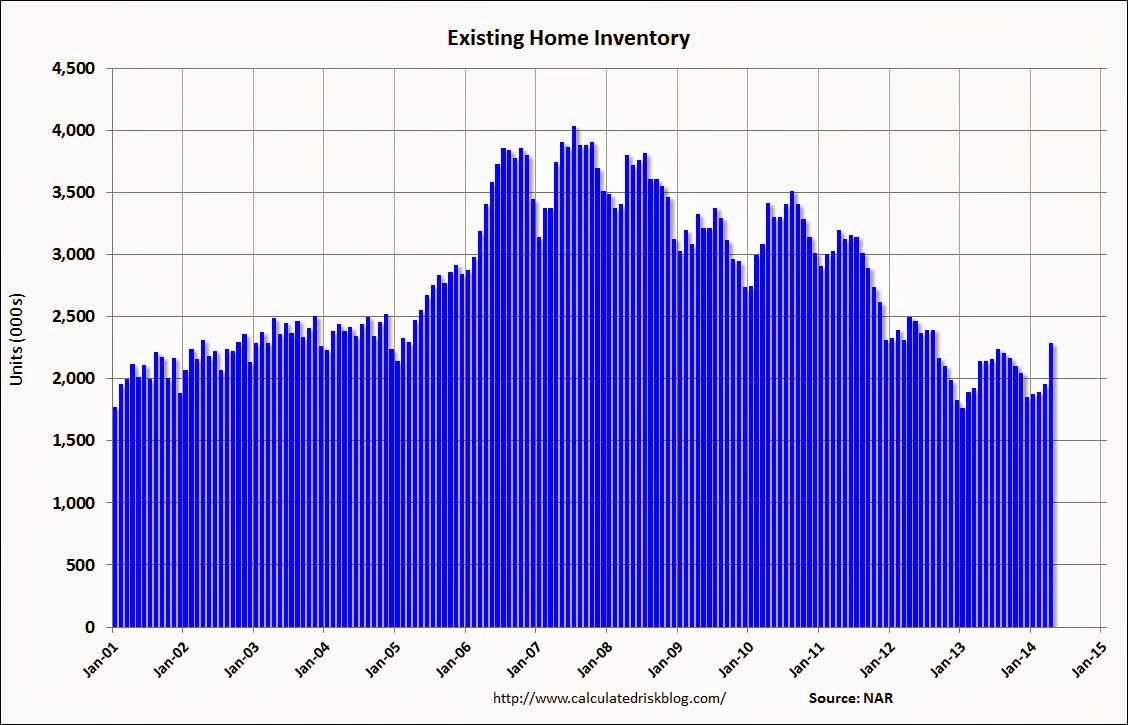

Here are the charts from Calculated Risk:

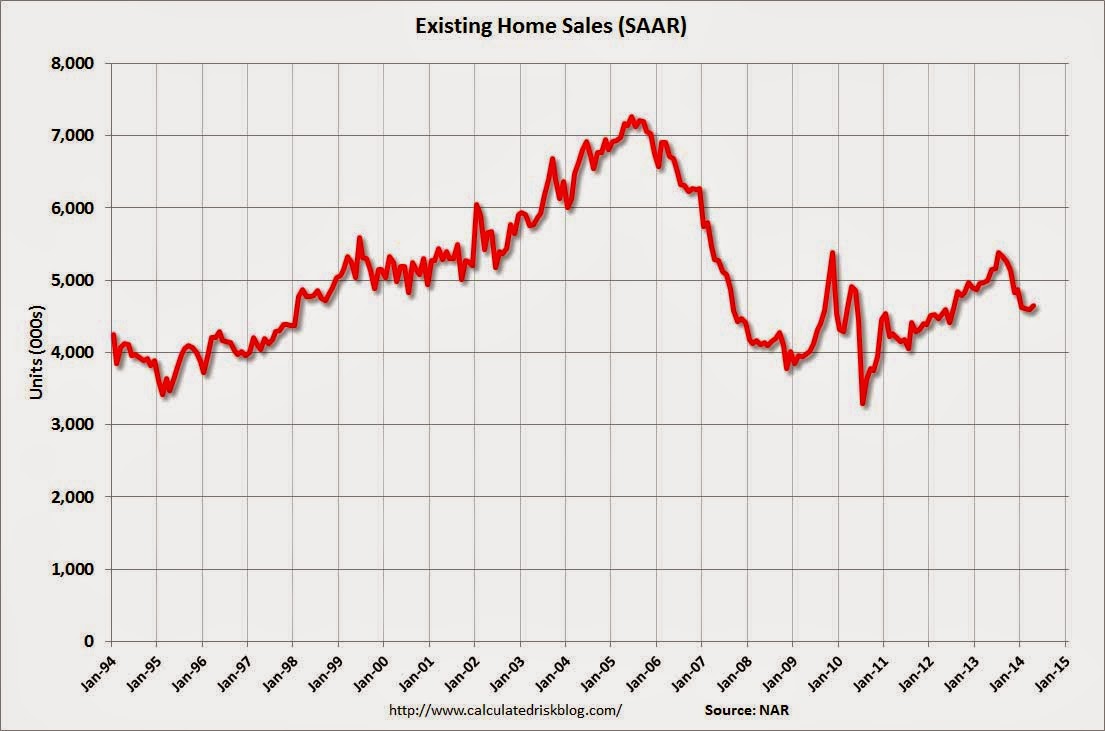

This added to Thursday’s data on existing home sales which was also luke warm:

In both we see modest levels of activity, a rising trend in inventories and weakening price momentum. I expect a very slow grind up from here.

It’s not disastrous and the US industrial economy is clattering along but housing is clearly now a diminishing tailwind and not the stuff of record stock market highs. Unless it means lower rates for longer, which bonds confirmed again, the 30 year yield bid down 1% to 3.4% and 10 year much the same to 2.54%.

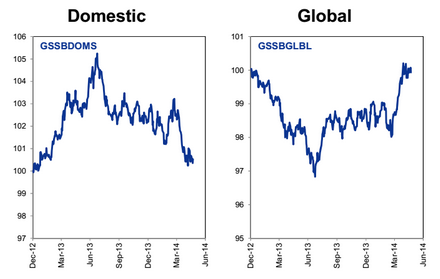

Here is a chart from Goldman Sachs which captures the move:

US domestic focused stocks are on the nose while internationally focused are powering up. That’s a pure lower US rates for longer trade.

The Yellen put powers on.