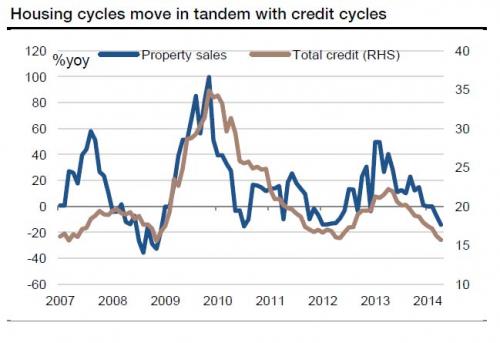

Late yesterday China released its April economic data and the tale it tells of the property sector is of concern. New starts contracted 15% year on year (vs. -21.9% in March), property sales fell 14.3% year on year (vs. -7.5% in March); and land sales fell 20.5% year on year (vs. -16.9% in March). This chart is from Society Generale:

George Magnus sticks his head up at the FT to make sense of it all:

The greater risk to China lies in the pervasive consequences of any property bust. Property investment has grown to account for about 13 per cent of gross domestic product, roughly double the US share at the height of the bubble in 2007. Add related sectors, such as steel, cement and other construction materials, and the figure is closer to 16 per cent. The broadly defined property sector accounts for about a third of fixed-asset investment, which Beijing is supposed to be subordinating to the target of economic rebalancing in favour of household consumption.

…The reason things look different today is the realisation of chronic oversupply. As the property slowdown has kicked in, housing starts, completions and sales have turned markedly lower, especially outside the principal cities. Inventories of unsold homes in Beijing are reported to have risen from seven to 12 months’ supply in the year to April. But when it comes to homes under construction and total sales, the bulk is in “tier two” cities, where the overhang of unsold homes has risen to about 15 months; and in tier three and four cities, where it is about 24 months.

…If activity levels and prices weaken further, Beijing’s resolve not to respond with traditional stimulus programmes is unlikely to hold. We should expect a potpourri that might include: extra spending on infrastructure and environment programmes; faster urbanisation in inland and western provinces; some relaxation on restraints on homebuying, such as mortgage deposits; and, ultimately, new monetary easing.

Advertisement

That sounds right to me. We can also expect slower growth despite the offsets. Capital Economics explains why:

The problem in the property sector is not that there is a price bubble, as many have argued over recent years. It is that property construction has been growing at an unsustainable rate. On average, property starts have increased at a real rate of 16% each year since the turn of the century, with a massive surge in new projects in 2009, when credit controls were loosened and local governments gave the go ahead for a vast number of projects to support employment.

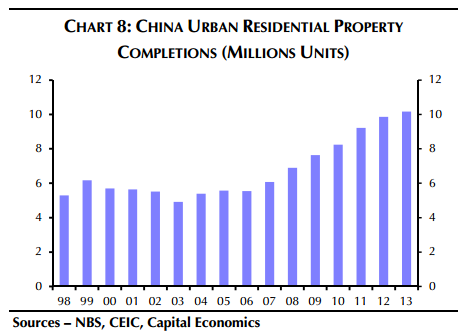

As a result, the number of new properties being released onto the market each year has been rising fast. Residential property completions have risen to about 10 million units last year, from five or six million a few years ago.

To put this in perspective, China since the turn of the century has built residential property equivalent to the entire housing stocks of the UK, Germany and France combined. And the number of new properties continues to grow each year. Residential investment simply cannot continue at this pace. The usual argument is that urbanisation will drive continued increases in new residential demand. But that’s not what the most authoritative projections show.

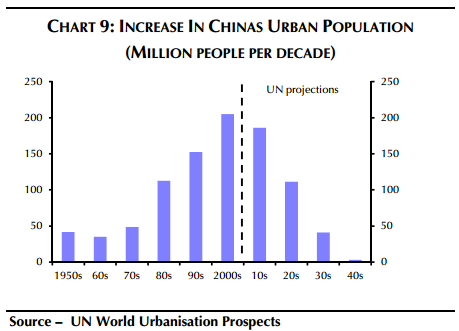

For example, the UN’s most recent estimates of increases in China’s urban population show that the pace of urbanisation has already peaked. China’s government recently published a policy document on urbanisation. Its projections show exactly the same: slower growth in the urban population over coming years than in the recent past.

Of course, there are other factors driving urban residential demand, such new household formation by existing urban residents, and the need to replace old housing stock.

But the big picture is unchanged. The upshot is that there is a mismatch in the real estate sector, with the number of new properties being built increasing each year, but no such increase in the underlying drivers of demand.

Attention Pascometer! China can keep building at an astonishing rate but if it’s not as much as the year before then growth slows. It’s the most misunderstood notion in economics, it’s the rate of change that matters, not the absolute level.

Advertisement

Capital Economics sees 7% growth this year and next then 6% in 2016 as authorities react in the way Magnus describes. I’m a little more bearish than that and not so sanguine about the downside risks. As Magnus concludes:

China is different from the west in many ways but the real economic effects of a burst property bubble are the same the world over.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.