Chris Joye is a stand out at the AFR. It’s like a light switches on in the dark when he writes over there, in both style and substance. Today we have another thought-provoking observation:

Australian credit investments are booming. On the back of the lowest borrowing rates in history and generally benign conditions across most asset classes, the cost of issuing Australian corporate bonds and selling home loans via portfolios of residential mortgage-backed securities (RMBS) is plumbing new lows.

In the words of one major bank analyst on Tuesday, “volatility is absolutely crushed for now with the VIX Index looking like a pancake”. Volatility is a measure of the probability of loss in financial markets, with the Chicago-traded VIX index tracking the volatility of US equities.

This favourable sentiment is allowing banks and companies to raise money to fund loans at some of the cheapest levels since the global financial crisis.

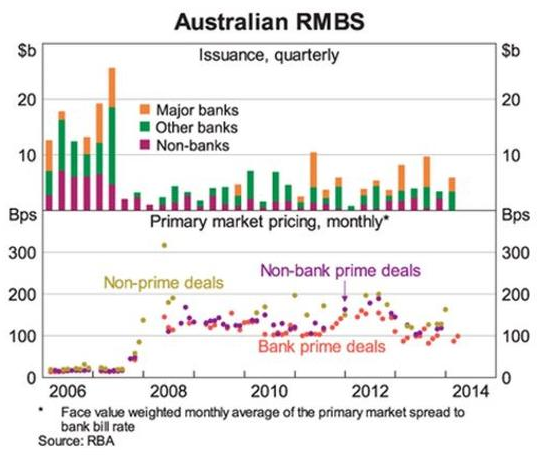

What Chris is saying is true within the context of this cycle. But in the longer term it is important to remember that Australian credit quantities and price remain very different to pre-GFC levels. Look at the RMBS spreads in the above chart, prices have been trending down since 2012 but remain miles above 2006 levels.

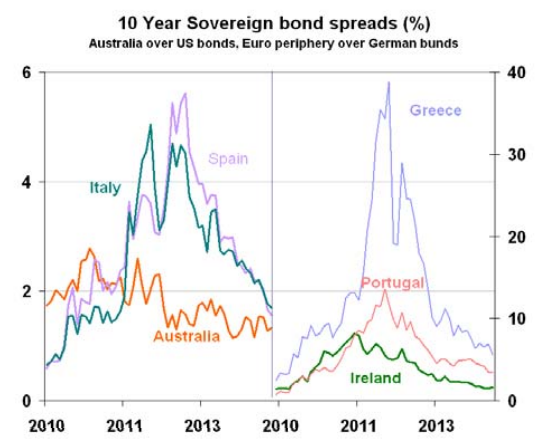

In fact, in my view, Australia has been under-performing the global chase for yield, with many of the spreads between Australian and global debt compressing. The same phenomenon is apparent in the sovereign spreads. As I argued recently:

The Australian current account deficit can only be funded at affordable rates if the Budget remains in good shape for its own borrowing rates and, more importantly, for its guarantee of the major bank’s offshore borrowings, which sustain our huge household sector leverage. It is the key stone in the arch of the Australian economy. Take a look at the 10 year bond spreads between Australia and Europe:

The spreads have been coming in as normalcy returns to European bond markets but not here. While some will argue that this is because growth prospects are higher, it’s also because that growth hangs on access to external debt and as a lonesome South Pacific sardine the only insurance for sovereign and bank bond holders is a clean Federal balance sheet. I do not believe quantitative easing and bond monetisation is viable for Australia, lest the currency collapse completely.

On a more like for like basis, Canadian 10 year yields are currently much lower than Australian.

Advertisement

Yes, Australian bonds are booming, but not so much that we still don’t have to pay a significant premium to fund our highly risky externally funded economic model in a credit averse post-GFC world.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.