Goldman Sachs is pulling no punches today and it’s Australia that’s on the end of them:

“Two-year property downcycle imminent; negative implications for banking/commodity/machinery”

…With demand poised to slow given a tepid economic backdrop, weaker household affordability, rising mortgage rates and developer cash flow weakness, we believe current construction capacity of the domestic property industry may be excessive. We estimate an inventory adjustment cycle of two years for developers, driving 10%-15% price cuts in most cities with 15% volume contraction from 2013 levels in 2014E-15E. We also expect M&A activities to take place actively, favoring developers with strong balance sheet and cash flow discipline.

….Mortgage key to avoid prolonged downturn: We believe lower mortgage downpayment/rates, RRR cuts, and developers’ price cuts should help improve affordability and allow transaction volumes to hold at a level sufficient for the industry to restore supply-demand balance by end-2015E.

…Policy delay poses significant downside risks: We believe China has the flexibility (in terms of potential policies, e.g. RRR cut, mortgage easing, removal of L/D ratio, etc.) to prevent a severe property downturn. However, we are concerned about the timing of their implementation, if any, as possible delays could lead to further slowdown in the property sector and a fall in FAI.

“Time to adopt a defensive stance”…Near-term, we prefer defensive stocks in the property/banking/commodity/machinery sectors, and would closely watch for downside/upside risks especially pertaining to policy changes.

And here is a Q&A:

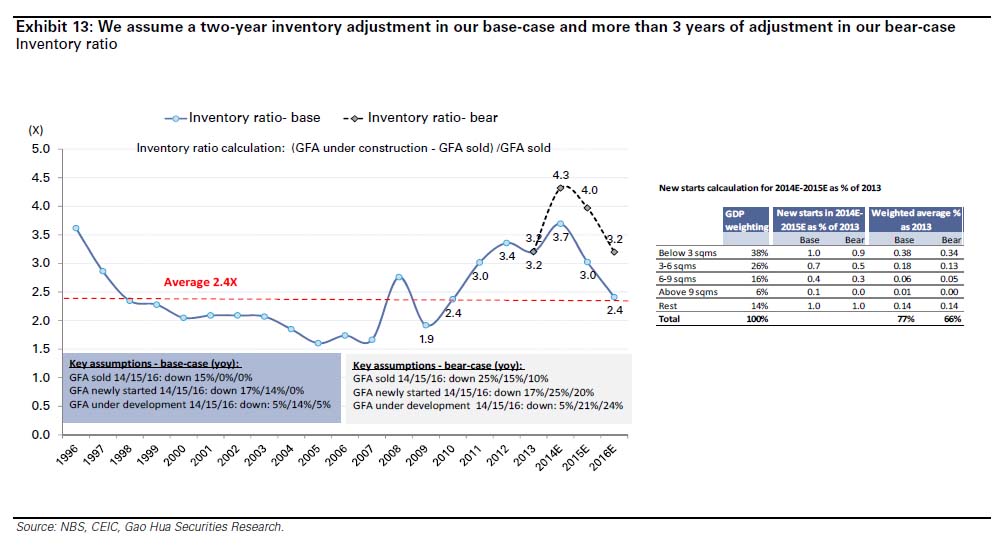

Q. How long will the housing market downturn be for this time?

A: We expect a two-year downturn to restore supply-demand balance. Given developers’ weak balance sheet as discussed in Q3 of this report and “Deteriorating balance sheet to impact property prices in 2Q14E” dated May 5, 2014, we believe developers would need to cut their new starts and construction capex more aggressively in order to lower their leverage and reduce their interest expenses. In the first four months of this year, new starts have already fallen 22% yoy and we expect this trend to continue. By assuming different level of cuts of new starts in cities with different level of oversupply issues for the 200+ cities we analyzed earlier, we conclude that property new starts would need to be about 20%+ lower than 2013 levels during 2014E-15E. We therefore translate it into 17%/14% yoy decline in new starts for 2014E/15E. This would in turn translate into about 5% and 14% yoy decline in GFA under construction for these two years. With our expectation that GFA sold would decline by 15% yoy in 2014 and stay yoy flat in 2015, we estimate the inventory ratio would be restored to end-2010 level of 3X by end-2015E, which we believe should reduce price decline risks. We also expect a further decline in inventory ratio to 2.4X (average level since 1996) by end-2016E assuming GFA sold/new starts are similar to 2015E levels but a further 5% drop in GFA under development in 2016E.

Q: What is the current housing demand/supply situation in China versus its history?

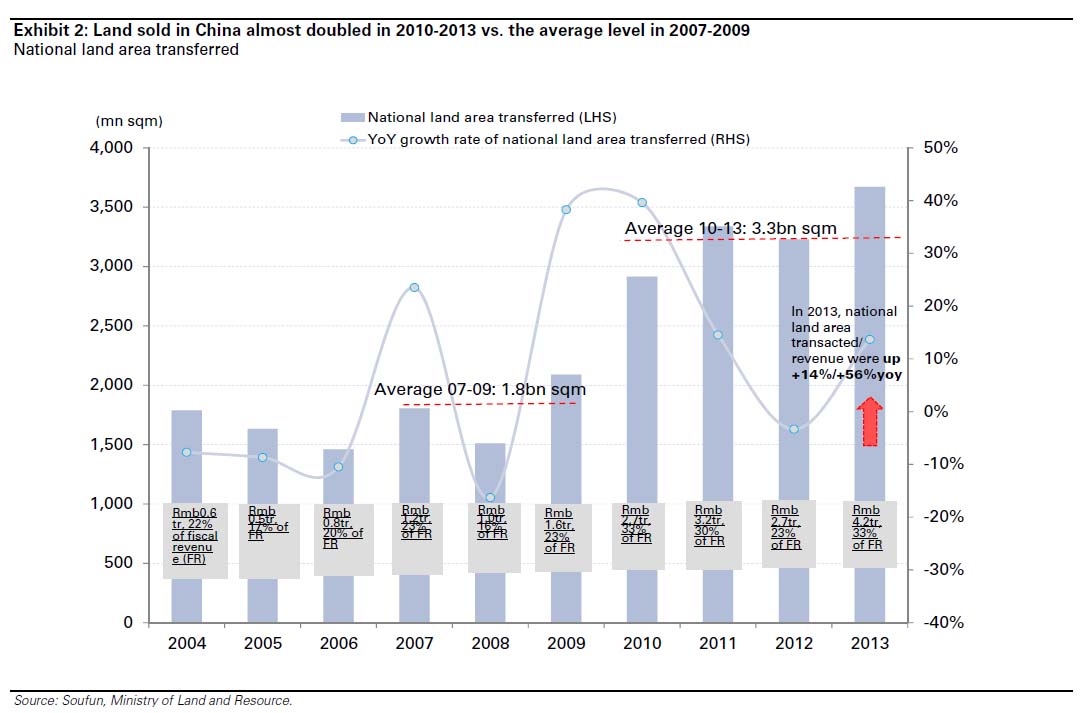

A: We have noticed a significant increase in land sales during 2010-2013, almost doubling the average level during 2007-2009. As an important fiscal revenue source to support local governments’ fixed asset investment (FAI) post the 2008 global financial crisis, land sales in China have significantly increased since 2010, with average land area sold in 2010-2013 almost doubling the average level in 2007-2009 (see Exhibit 2).

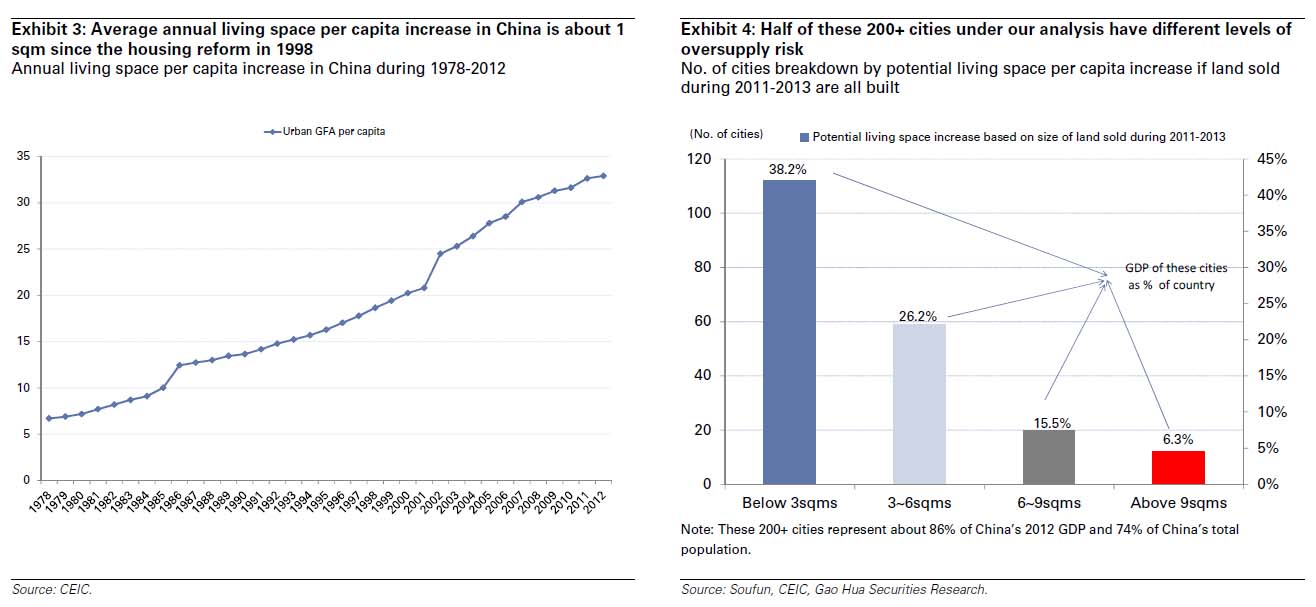

By adding up the total residential land sold during 2011-2013 in each of the 200+ cities, and dividing this by the total population in each city, we estimate the potential living space per capita increase for each of these cities. Our analysis suggests about half of these 200+ cities could see potential oversupply of properties and construction activities would need to be cut (with different magnitudes) in the coming years.

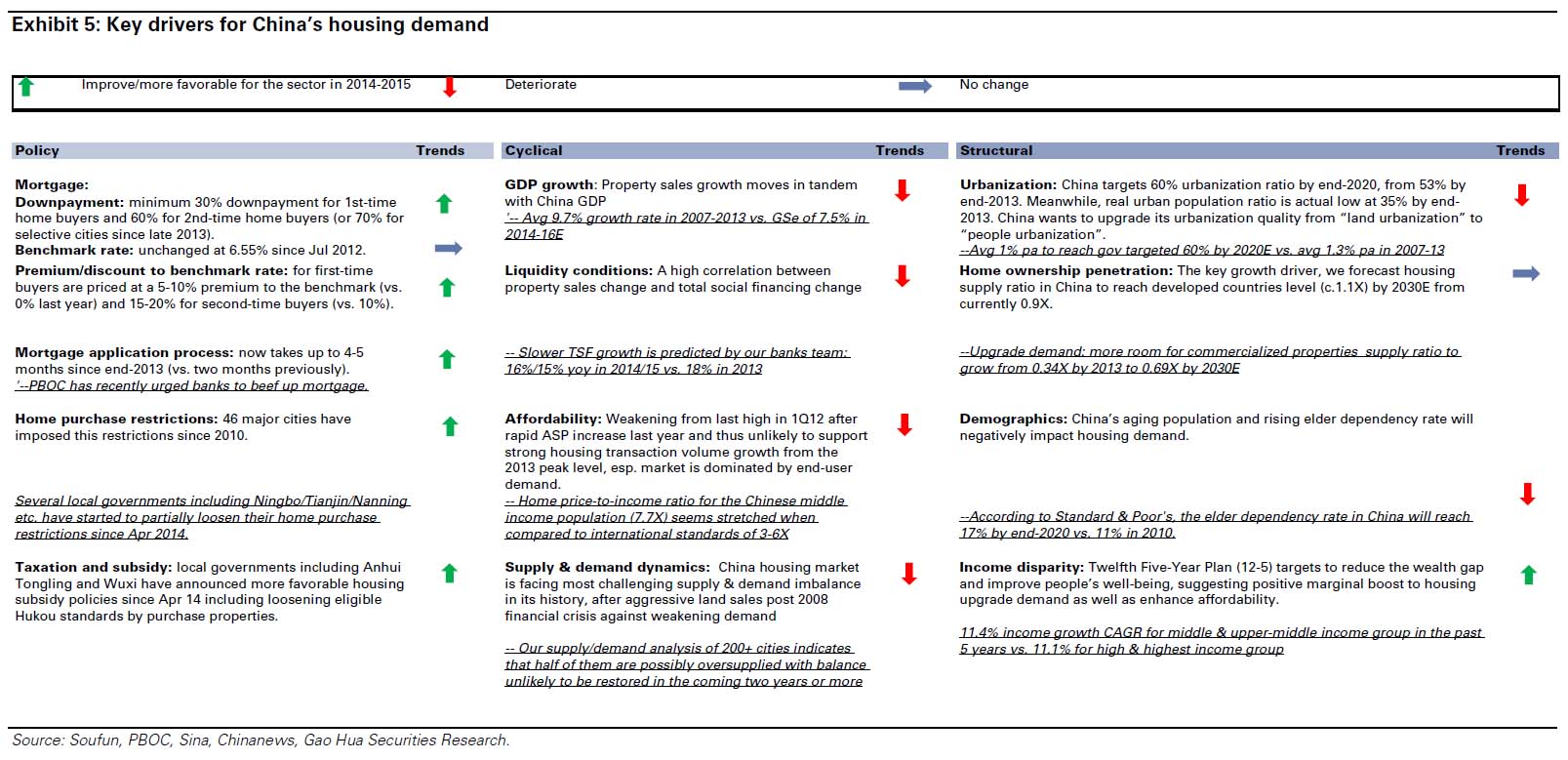

In Exhibit 5 below, we summarize the key drivers for China’s housing demand and our estimated trend in the coming years vs. past years (since 2010). We expect policy drivers to mostly move in a favorable direction, but cyclical and half of the structural drivers would either be in a negative or weakening trend over the next decade.

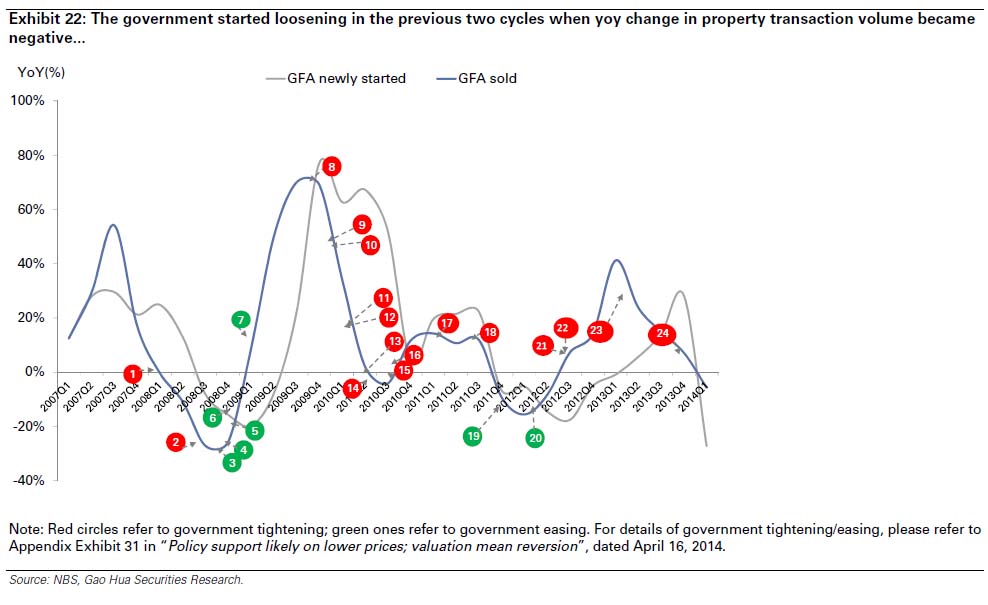

Q: When did the government start to provide support to the housing market in previous downturns?

A: With further deterioration of the housing market in the coming months, we expect the government to provide policy support to prevent prolonged housing downturn that could trigger a vicious cycle on the economy.

The exact timing of such support is difficult to predict, but we summarize below the indicators that have triggered government support for the industry during previous cycles:

Decline in quarterly property sales volume yoy (10%-20% yoy decline);

Decrease in property prices mom in most cities (about 50 out of 70); and

Land transaction premium over government base land price approaching zero.

We believe poor sales volume/sell-through ratio would lead directly to slow land acquisition and possible price cuts.

Residential construction represented roughly one quarter of China’s 20% fixed asset investment growth in 2013. Goldman’s 5% and 14% falls in construction floor space in 2014 and 2015 would thus take around 5-6% off fixed asset investment growth across those two years. It is already at 17.6% so we’re talking about a fall to 11-12% year on year growth (on the back of an envelope). That’s far ahead of any local forecast but is consistent with a swift rebalancing of Chinese growth and probable fall to about 6% GDP if spillovers are contained (which is questionable).

Advertisement

Moreover, this is the most steel intensive component of Chinese growth absorbing up to half of all steel output.

Goldman also raised its iron ore surplus forecast yesterday for 2015 to 175 from 145 million tonnes on diminishing Chinese growth prospects. It is still forecasting an$80 iron ore price but if it proves to be right about Chinese property then I’ll add that steel output growth will cease next year and a sub-$80 iron ore price for long periods is probable, as well as cut backs in iron ore production hitting volume growth.

That raises the clear and present risk of an echo housing bust and recession in Australia.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.