Recently I posted that MB’s five drivers model for the Australian dollar was pointing lower. The dollar broke lower last night and appears biased for more. The five drivers are:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth);

- investor sentiment and technicals; and

- the US dollar

For the first, there is now no chance of local interest rate hikes this year with falling terms of trade, the capex cliff and consumer confidence in the dunny. Indeed, the chance of another rate cut is rising as weakening local indicators mount up. Interest rate market conviction that that we’ll see rate rises in the year ahead has softened and they are pricing 8bps, down from 21bps not long ago. Australian bullhawk economists have backed away from rate hikes this year.

Moreover, with the recent weak inflation print, the RBA is free to resume jawboning the dollar and that began yesterday with dovish minutes and a Debelle speech both aimed at dollar weakness.

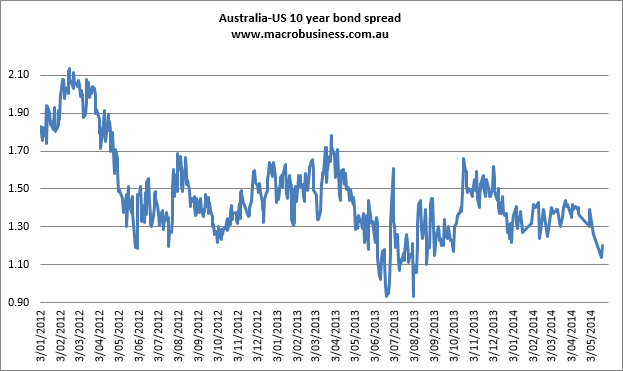

On the other hand, the rise in US bond yields that many expected this year has so far been cut short by a run of terrible economic data. Weather has largely been blamed and is responsible in some (possibly large) measure. That meant that the carry spread between Australia and US ten year bond rose earlier this year but this week it has broken in favour of Aussie weakness:

The progress of taper at this point is anybody’s guess but assuming the weather is mostly to blame US bond yields will not fall too much further. The last time the spread was at this level the Aussie was at 89 cents.

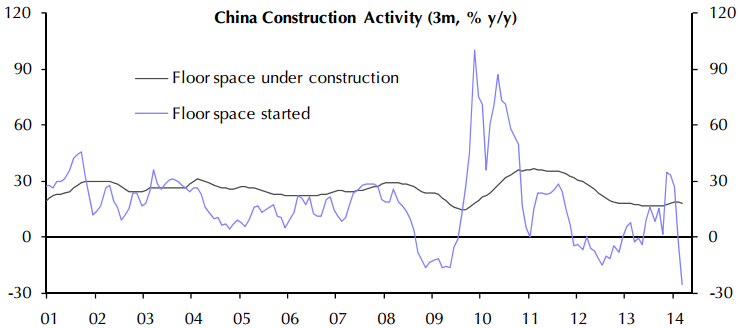

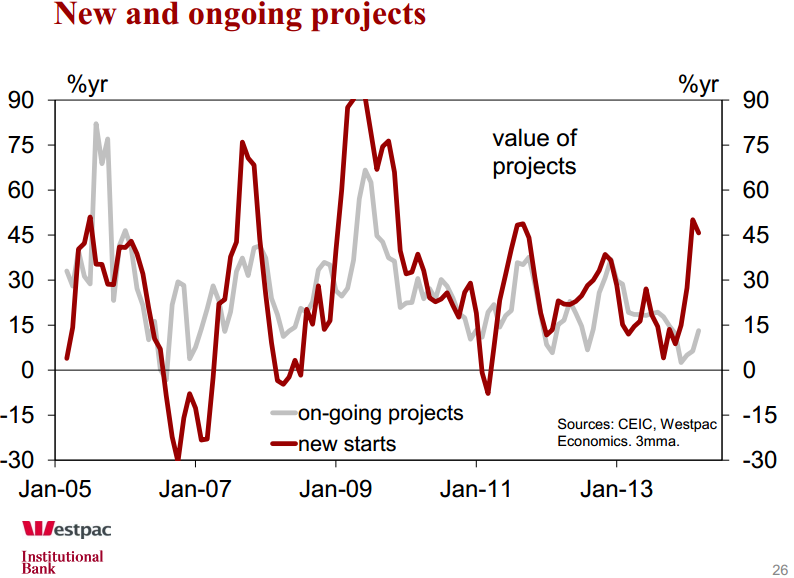

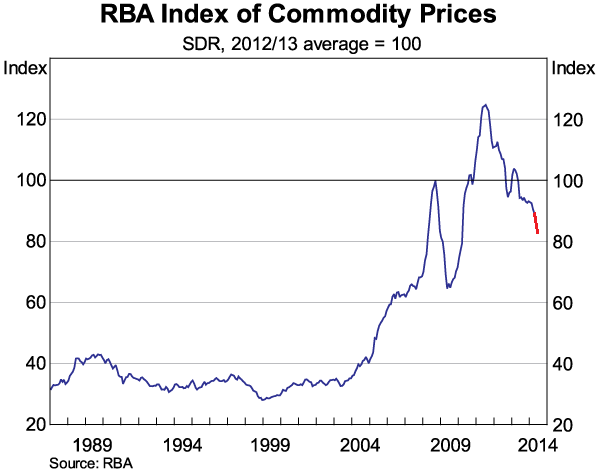

On driver two – global, local and Chinese growth – the jury is in. Global growth may accelerate this year (maybe!) but Chinese growth is going to slow over the next six months to 7% and go lower if the rebalancing process is allowed to run its course. Everything points to an ongoing cycle in which monetary and prudential policy is kept tight and fiscal policy lends targeted support. Property and steel are explicitly in the gun and infrastructure is expanding as an offset:

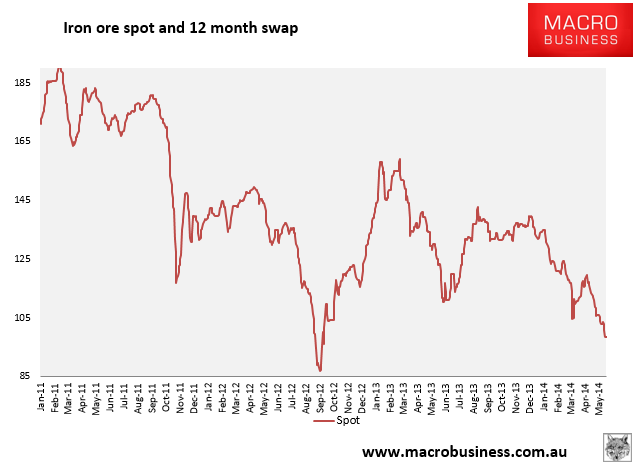

There is also, of course, the plunge in iron ore:

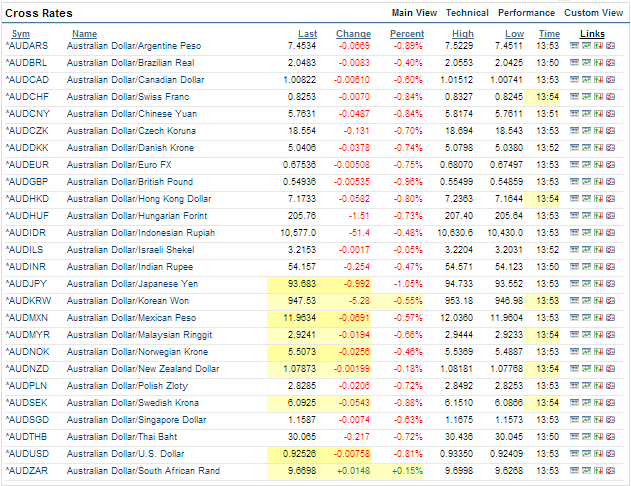

Which, in the past few days, has really singled out the Aussie for weakness on the crosses:

Coal has been smashed too and the falls in the terms of trade could very quickly approach “external shock” proportions from here. My estimate of the falls too date in spot prices are below (that will filter through contracts in the months ahead) :

Australian growth will follow suit. All things being equal, I expect another year of firmly sub-par growth, well under 3%, as the capex cliff, falling terms of trade and national income outweigh the cyclical forces of monetary stimulus.

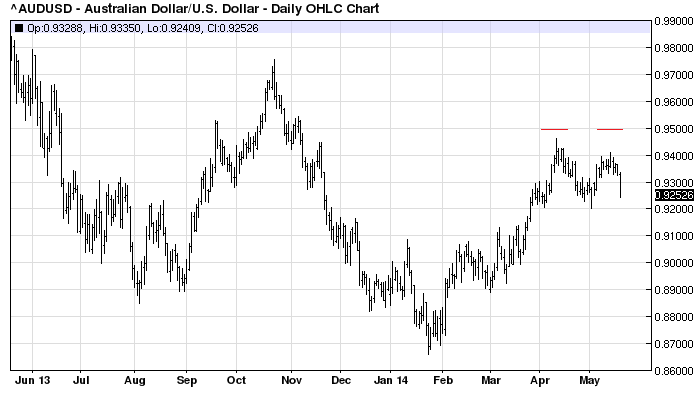

Drivers three and four, sentiment and technicals, look vulnerable. In technical terms, a potential double top is forming on the recent rebound:

If 92 cents breaks, substantial downside opens up.

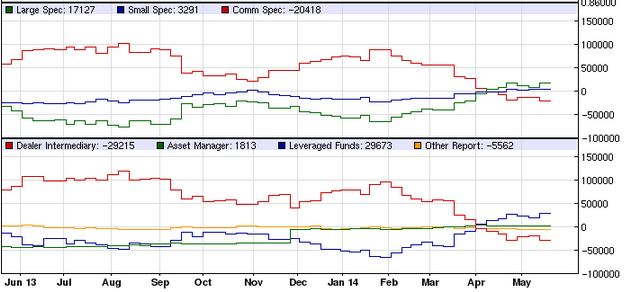

Turning to sentiment, the Commitment of Traders report is showing that the large and small speculators that control the market have recently charged into longs. The shorts have been completely washed out and a reversal looks quite possible.

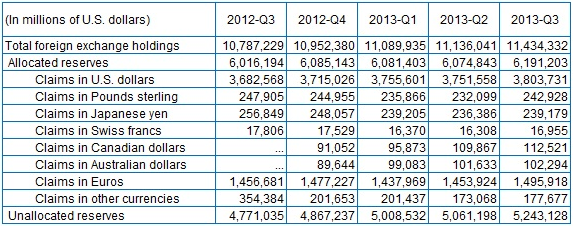

There is one possible positive for sentiment. We know that central banks have been adding Aussie to there reserve portfolios for a few years. That has been a significant real support to higher valuations and general market sentiment around the currency. The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) report shows the accumulation was still aggressive in early 2013:

However, it is interesting to note that as the Aussie has regained its cyclical mojo and gotten cheaper, official buying has slowed to a trickle. That does not strike me as especially committed to the cause. Buying in the twin currency in Canada has remain much stronger. That’s not to say we’ll see a reversal in the holdings. But we aren’t seeing much in the way of bargain hunting either. This has not been updated since December.

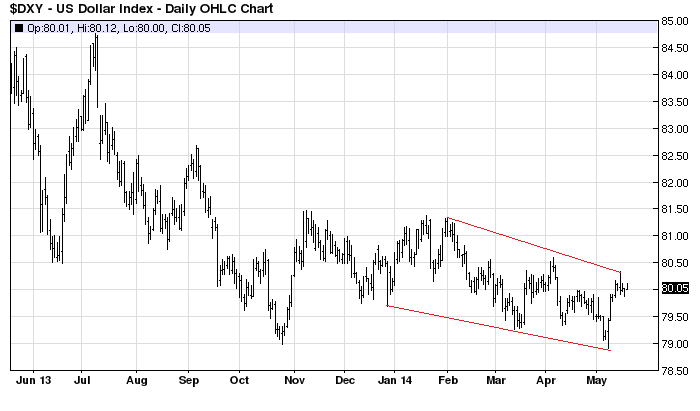

The final driver, the valuation of the US dollar, still looks weak and is the one major factor weighing on further Aussie weakness. The US dollar is in a downward channel:

That could be a bullish falling wedge pattern but given current bond market strength it’s not easy to see US dollar strength. As growth improves, albeit still disappointing, it should not at least go much lower!

The upshot is that the conditions for Australian dollar weakness are in play. The weakening in the divers is most apparent in the fundamentals of Chinese rebalancing and local cyclical slowing which will bring the RBA back out of hibernation. The broader financial bullishness for the Aussie emanating from weak US and EU interest rates over time is still there but that has not benefited the Chilean peso because of its exposure to China via copper. The same should happen to the Aussie as iron ore slides.

My long term view remains unchanged – downside first to 80 cents and then much lower – given I see no real recovery in Australia until its below 80 cents permanently.