Cross posted from Investing in Chinese Stocks.

Flat growth in the trust industry is contractionary from the late 2013 peak. If credit elsewhere picks up it can offset the decline, but it also needs to flow to the borrowers served by the trust market. Evidence from prior months points to a more generalized slowdown in credit growth, to say nothing of the real estate sector that is in full blown contraction. The case in the news today is of a Shandong firm auctioning assets, having begun the asset sale process more than a year ago and under suspicion of embezzling funds overseas.

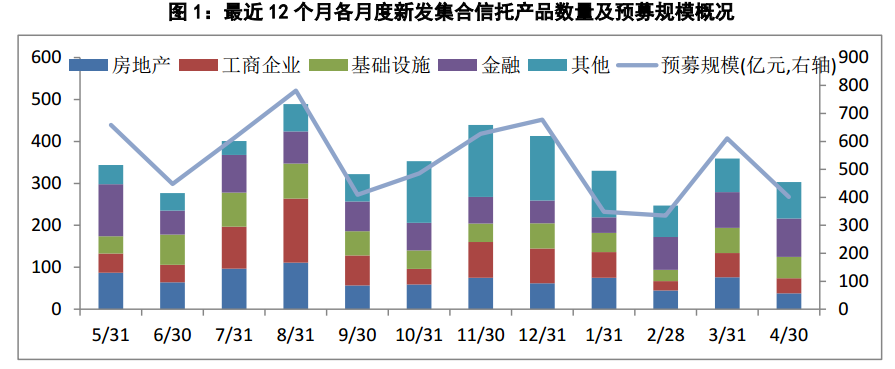

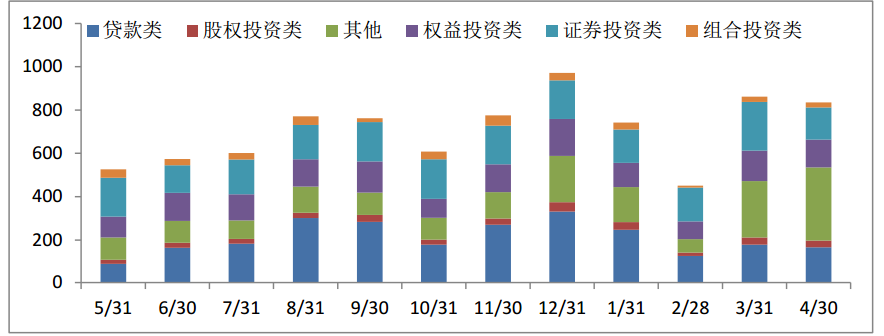

Data and charts from 金牛理财. Bars showed fund raising and lines the number of products.

Newly issued trusts in April raised only about 47% as much capital as in March, with the total number of trusts issued also down. For those worried about ponzi financing, note the drop in real estate trusts (the bottom darker blue section on the bars) and remember that May is a huge month for real estate trusts coming due. There is nowhere near enough capital coming into the market to replace the maturing trusts, with ¥120 billion coming due in May alone (20% of the total), but real estate trusts raised only about one-tenth of that in April. If the borrowers need to roll their debts, credit will have to come from different channels. Without credit, the selling pressure on the real estate market will intensify.

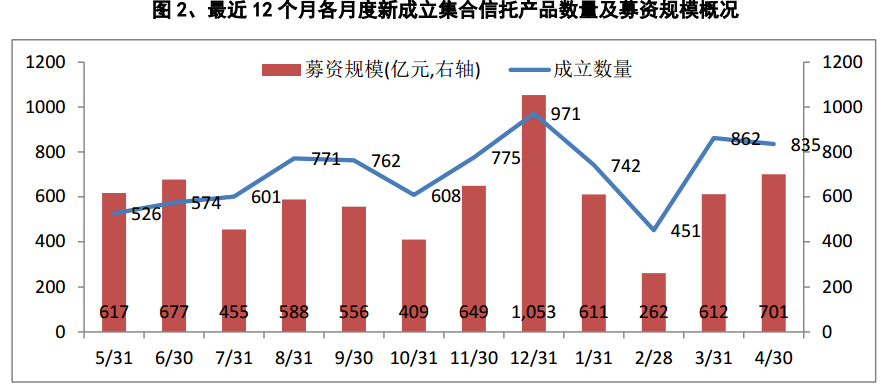

Fundraising was a bit better for newly established trusts:

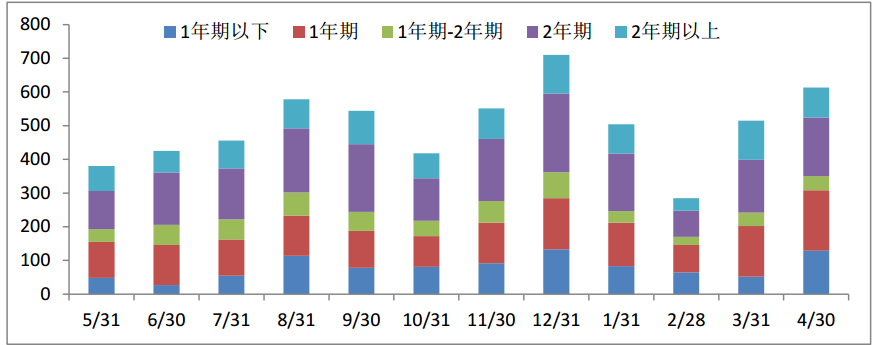

The strength in fundraising was entirely due to growth in products with maturities of 1-year or less than 1-year.

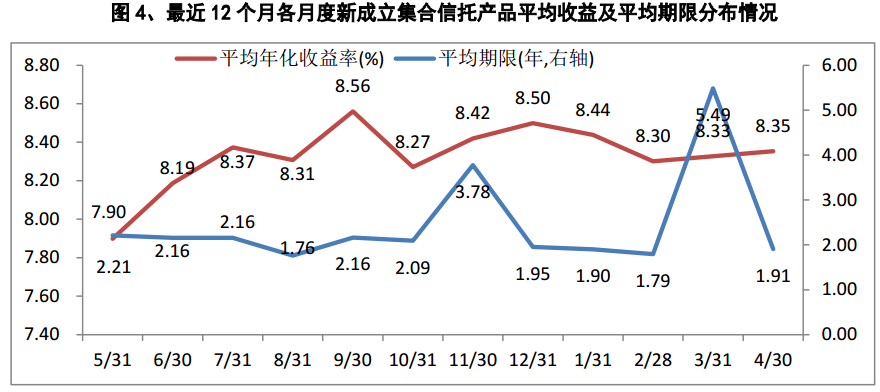

Here’s the average yield and average maturity for the trust market:

Here are the different trusts by use of funds. The big growth in the “other” category is concerning.

The trust industry looks relatively healthy from the view of total assets gathered, but the numbers are not positive for the overall credit market and not good at all for the real estate market.

Defaults and forced assets sales are already underway. The case below from Shandong has misappropriation of funds as part of the story, with CITIC already having auctioned off a number of assets last year in order to extricate itself from the situation.

Shandong Real Estate Firm Auctions Off Assets (千亿地产信托兑付洪峰5月来袭 一山东房企上拍卖席)

Qingdao Real Estate Trust Crisis Feeling (青岛地产信托5月危情 中航信托或已脱身)

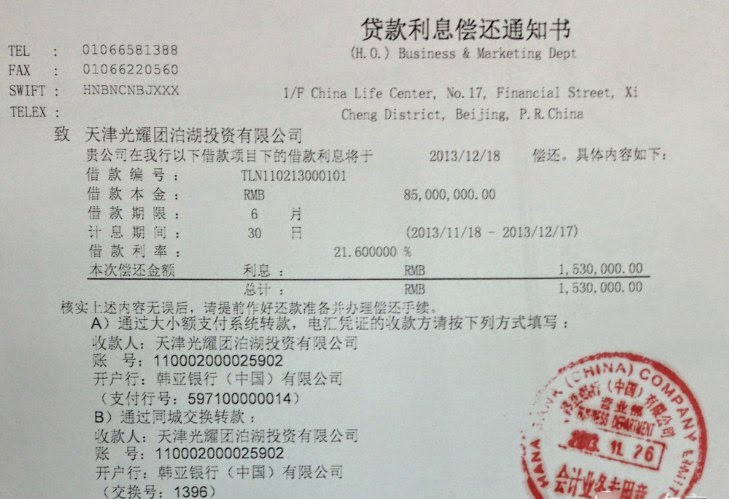

As well, top 100 developer Guang Group is rumored to be facing bankruptcy after failing to deliver buildings on time. The third article below says the firm has been blacklisted by the banks and was already considered a “bad debtor” as early as 2012. The firm is rumored to have been borrowing privately at 4% monthly interest rates; the company neither confirmed nor denied. Another article claims the company borrowed at 21.6% interest last year from Hana Bank. (曝光耀资金内幕 去年向韩亚银行贷款年利率高达21.6%)

Just below is the company’s response: capital is indeed tight, but that doesn’t equal bankruptcy.

Whether accurate or not (in terms of the bankruptcy rumor), this story is among the top headlines on some business sites or in their finance sections, including People’s Daily.

光耀地产回应面临破产传闻:资金链确紧张但不至于倒闭 (Guang Group responds: Capital Chain Tight But That Doesn’t Equal Bankruptcy)

Chinese media reported today hundred glorious estate real estate companies can not pay because of a number of real estate building, the company is facing collapse. In addition, the company has been included in the national list of dishonest debtor.

In this regard, the real estate aspects Guangyao said in response to the China Securities Network, indeed there are several real estate companies postponed handover situation, capital chain does have some difficulties, but are seeking alternative sources of finance banking, trust, etc., “and will not collapse.”

It is understood that due glorious estate capital chain tension, resulting in its listed companies * sum of 60 million yuan loan guarantees for new capital ST violations carried out while exposing the * ST new capital letter Phi violation, and therefore the property is listed Guangyao into a national dishonest debtor lists.

In this regard, glorious estate has been included in the national response to recognize dishonest debtor list, “but the reasons are complex, in the middle there are some disputes.”

More here: 中国百强房企光耀地产被传倒闭 资金周转成硬伤