The Bureau of Resource and Energy Economics (BREE) is out with its biannual major resource projects update and the capex cliff approaches ever closer:

BREE’s version of the investment pipeline is a generic model and in practice resources and energy projects go through complex and tailored development processes that suit their proprietor’s planning requirements. The BREE pipeline model is useful for assessing trends in resources and energy sector investment such as the rate at which projects are progressing or if bottlenecks are emerging at any particular point. Despite the strength of the resources boom over the past decade, it has been clear that not every resources and energy project is developed. As such, the projects still in the Publicly Announced and Feasibility Stages can only be viewed as potential investment and additional analysis is required to produce an outlook for future investment in the resources and energy sectors.

BREE’s outlook for resources and energy project investment provides aggregate estimates of investment in two scenarios, a ‘likely’ and a ‘possible’ scenario. The two scenarios model the rate at which projects currently at the Committed Stage are expected to move to the Completed Stage and are subsequently removed from the list, as well as the timing of projects assessed as possible or likely to progress to the Committed Stage. BREE does not attempt to model the timing of projects and forecasts are therefore based on the current project plans. The schedules of planned projects, including both the timing of a FID and start of production, are uncertain and subject to variation (as are BREE’s investment forecasts). It should also be noted that the concept of investment being modelled is the total value of projects that are under construction each year, and not the expenditure of each project in that year.

The ‘likely’ scenario is based on the existing projects at the Committed Stage and adds projects that BREE assesses as having a higher probability of proceeding based on analysis of a range of internal and external factors that historically helped determine a project’s success in being sanctioned. Where data is available, analysis of the proposed project’s position on the relevant commodity cost curve and an assessment of the internal rate of return are undertaken. As the assessments are probability-based there still remains a degree of uncertainty over projects assessed as likely and their progression to the Committed Stage is far from guaranteed.

The ‘possible’ scenario includes projects already at the Committed Stage, projects assessed as likely to proceed and projects assessed as ‘possible’. A possible rating is given to a project that has some positive internal and market factors that suggest it may advance to the Committed Stage, but it also faces greater challenges than a ‘likely’ project that may limit its commercial viability.

Projects assessed as unlikely to proceed are not included in the forward projection of the value of committed investment. Although assessments are made at the project level, as some of the information provided to support the assessment is treated as commercial in confidence, individual project assessments are not provided with the Resources and Energy Major Projects report.

Outlook for resources and energy investment In the past six months government initiatives to streamline the approvals process and award major project facilitation status have been implemented. Nevertheless, the current state of commodity markets is not supportive of further investment in resources and energy projects. World demand for raw materials and energy remains strong and for most commodities is still growing. However, the global rush to capitalise on China’s booming appetite for commodities has now resulted in too much supply entering markets. The quarterly activities reports of many Australian miners and aspiring mine developers show a slowing in activity to progress projects to the Committed Stage. Although Bankable/Definitive Feasibility Studies have been completed that indicate favourable project economics, investor appetite for risk amid a period of declining commodity prices appears limited.

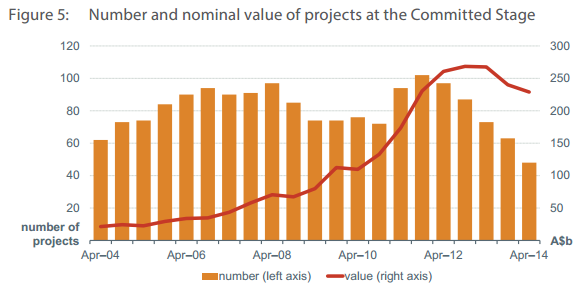

The outlook for resources and energy investment therefore remains subdued in the near term with the investment cycle having peaked. The value of committed resources and energy projects has now decreased from its peak of $268 billion in April 2013 to $229 billion at the end of April 2014. However, it is important to remember that coinciding with the decline in investment are substantial increases in annual production capacity including 215 million tonnes of iron ore, 43 million tonnes of coal and over 1100 petajoules of gas. The investment phase of the mining boom is winding down but the shift to the output phase is now in full swing. Furthermore, while the investment phase lasted for around five years the output phase will last for decades and deliver an ongoing stream of economic benefits such as employment, royalties and ongoing operating expenditure in Australia.

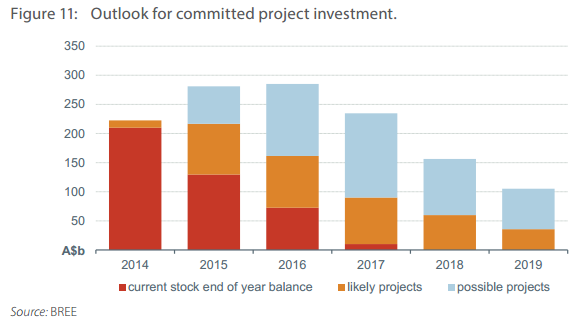

BREE’s outlook for investment therefore remains broadly unchanged and it is projected that there will be a substantial drawdown in the stock of committed projects as high value LNG projects are completed (see Figure 11). While efforts are being made to expedite projects through government approval processes, a reversal of the trend for schedule delays seems unlikely and further delays to project approvals are expected. As BREE’s likely and possible scenarios are based on the current announced schedules for projects, further shifts in the forecast investment profile are also likely in the future.

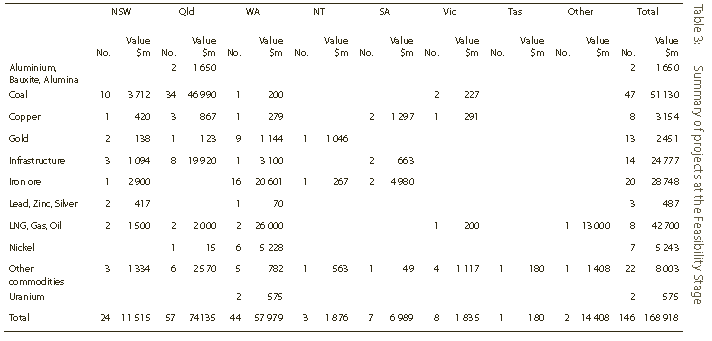

Here is BREE’s list of feasible projects from which the “likely” category is drawn:

Advertisement

BREE is very clearly over-estimating the “likely projects”. Where are we going to see an additional $60-70 billion in projects come from when most are coal, iron ore and LNG? FLNG is bout the only one really likely.

Until 2016/17 or so by far the most likely outcome is the “current stock” bar. Big cliff ahead.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.