The quality of China’s GDP growth is rising with falling property prices. The economy is diverting resources away from wasteful bubble activities to productive ones. While growth is slowing, it reflects shrinking of the bad GDP. Two-thirds of the economy is still expanding steadily. More importantly, China is experiencing a labor shortage due to a shrinking of working-age population and steady economic expansion. The economy is in a strong position to absorb the fallout of a deflating property bubble.

Attempts to bail out the property market are unlikely to succeed. China’s property market is a bubble in both volume and price. Oversupply, especially in small cities, is destroying the expectation of price appreciation. Speculation cannot be revived. Household indebtedness is close to saturation. The high prices in large cities cannot be sustained by debt growth. Bailout attempts, such as eliminating purchase restrictions, will only backfire, as the restrictions do not suppress demand in the first place.

The property market could follow the example of the A-share market. Bailout attempts have less and less impact. The market eventually dies when people no longer pay attention to it.

Allowing prices to adjust is the best policy. The distortions in the economy due to the bubble shrink. The efficiency of the economy improves as a result. The improving efficiency leads to better labor income, which supports the virtuous cycle of rising wages and rising consumption.

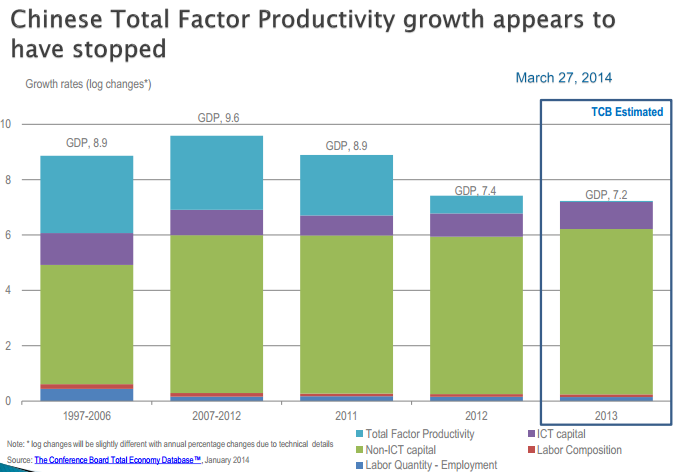

Although he doesn’t actually use the word, what Xie is talking about is productivity. Remarkably enough, that is now China’s challenge, even though it is still poor and unskilled in huge swathes of the population, suggesting tremendous productivity potential.

In fact, China’s productivity stalled completely in 2013. The following chart is from a recent Ross Garnaut presentation at Melbourne University’s Centre for Contemporary Chinese Studies:

It’s not all that hard to figure out where the stall is coming from. The factors at work are very familiar to Australians. A property boom has mis-allocated huge amounts of capital into unproductive investment. That has the double whammy effect of inflating labour input costs and reducing capital efficiency and productivity dives.

China clearly recognises that such a model is unsustainable even if we don’t. It can be propped up for a while by ever-increasing debt but not forever and it’s not in the interests of a single party system to drive it to collapse.

So, it’s not so much a birth as it is rebirth that China faces; a return to the productivity driven growth of yesteryear that boosts household incomes and consumption. That can only be achieved by reducing capital mis-allocation.

On the weekend we had more confirmation of such. First from the head of the People’s Bank of China, Governor Zhou Xiaochuan who said:

China may have a housing bubble only in “some cities”…China is a big country with multiple housing markets, many of which are still drawing new inhabitants from the countryside…”China is still in the process of urbanization, so there may be some kind of volatility in the supply-demand relationship…But if you look at the medium-term of urbanization, I think we still have a very good market for home sectors…The economy has slowed down a bit, but not very much,” Zhou said. “We should keep vigilance on whether it continues to slow down.”

As well, on Friday some Chinese media reported that sub-tier one cities were free to lift property restrictions but it appears that is false, from Investing in Chinese Stocks:

The Ministry of Housing denies that Chinese Cities Can Ease Buying Restrictions. I was a bit skeptical of the story yesterday, and sure enough a denial is out one day later. The Ministry says they do not know the source of the information.

住建部官员否认楼市限购将放松 新领导还在熟悉情况 (Ministry of Housing Denies Buying Restrictions Will Ease New Minister Still Familiarizing Himself)

The purchase of the property market deregulation suspense: Ministry of Housing said it is investigating, understanding 21st Century Business Herald reported Ji Rui Kun Beijing

A ” number of people confirmed that the Ministry of Housing, in addition to the north, on the broad, deep, other cities restriction policy can be self-regulating , “the news caused strong concern.

Take this news yesterday afternoon, some in the second and third tier cities have large land reserves listed property company’s share price soaring, Langfang Development [ 4.84% funding research report ] daily limit yesterday, China Happiness [ 2.40% funding research report ] also rose more than 7%.

May 23 morning, the 21st Century Business Herald also call the Department of Housing and Urban stakeholders to understand, “we are to understand the situation, do not know the relevant sources.”

A source close to the Ministry of Housing is also the phone told 21st Century Business Herald reporter, “I understand that there is now the Ministry of observe, understand, study the current market conditions, how to see the direct statement it? National level of real estate policy The adjustment is needed given the State Council, the city which is the need to finalize the provincial inside, the building housing the Department can only investigate, understand, report, and then perform the role. “

“Besides, the Ministry of Housing to a new party secretary, the new secretary is currently listening to reports, familiar with the stage,” the source further said.

May 23, Wang Jue Lin, former deputy director of the Research Center of the Ministry of Housing policy in an interview with 21st Century Business Herald reporter interviewed have even said it is an accident, “not the interpretation is wrong, that’s wrong, from a rescue perspective, now not to the first-tier cities in addition to, the purchase of their own interpretation of the period. “

“From a market perspective, the first four months, real estate sales area of 277 million square meters, better than in 2011, 2012, but lower than 2013 poor, far from the lowest point in history, “Wang Jue Lin said, is indeed part of the wait period, the future The great unknown, immediate bailout stance may not exist.

Wang Jue Lin according to understand, the Ministry of Housing has repeatedly stressed the bidirectional control, bi-directional control is based on the fundamental market conditions, rather than a simple first-tier cities and other categories of “one size fits all.”

In addition, Wang Jue Lin said, a critical period in the market, such as the purchase of the adjustment policies that place the initiative, the Ministry of Housing is impossible to say how kind who should and who should not be how. Centaline Beijing Dawei, director of market research also think that argument countless accurate, Zhang Dawei said, “The policy was aroused great concern, mainly belonging to the market and also because the policy of wait and see.”

They will nurse this thing down but down it will go.