Cross-posted from Investing in Chinese Stocks:

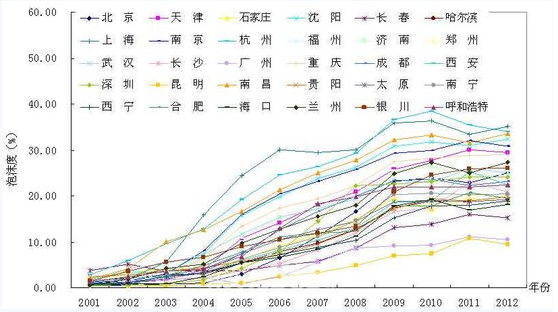

A hot topic in the news today: researchers in China devised a method for quantifying overvaluation in real estate. Among the factors are disposable income, population density, construction costs, mortgage rates and real estate developer investment. (中国30城房价泡沫排行榜 近七成城市超警戒线)

I found a link to a 2012 version of the research: 产业经济学系讨论稿系列No.120:中国30个大中城市房地产泡沫:基于预期均衡价格模型分析【高波 王辉龙 李伟军】pdf, although that may be the latest research because all of these stories are referencing 2012 in the stories. That would likely mean these bubbles have increased by more than 10% in many cities, pushing them to 30% to 40%.

The number one bubble city was Shanghai, at 35.1% above “fair value.” Shanghai is likely to always trade at a premium though, so it’s hard to know what the market will decide is fair value. Other cities on the list may not be as lucky.

2012 Home Price Bubble Top 10

Shanghai…..35.10%….April 2014 New Home Price :33402元/平米

Hangzhou…..34.10%….April 2014 New Home Price:18151元/平米

Nanchang…..33.52%….April 2014 New Home Price:9654元/平米

Shenyang…..32.34%….April 2014 New Home Price:7953元/平米

Nanjing……30.91%….April 2014 New Home Price:14118元/平米

Tianjin……29.46%….April 2014 New Home Price:11181元/平米

Chongqing….29.03%….April 2014 New Home Price:7926元/平米

Lanzhou……27.26%….April 2014 Existing Home Listed Price:5714元/平米

Yinchuan…..26.07%….April 2014 Home Price:5427元/平米

Jinan……..25.69%….April 2014 New Home Price:8754元/平米

This is also a top story in the Chinese news today.

How Vulnerable are Chinese Banks to a Real Estate Downturn?

What is clear, however, is that real estate price corrections have large consequences beyond simply an increase in real estate developer defaults and mortgage foreclosures. Real estate demand supports a wide variety of industries and real estate as an asset plays a critically important role as collateral for lending and as an investment for households. Large drops in real estate prices lead to contractions in investment and consumption which will damage the economy and ultimately feedback upon the financial system in the form of more defaults. China isn’t in danger of a US-style wave of foreclosures, but the financial sector is certainly not insulated from a real estate-induced economic slowdown.