The basic assumption in Australian monetary policy right now is that the US recovery will push up interest rates in the medium term and that will, in turn, close the yield spread between Australian assets and those in the US, dragging down the Australian dollar.

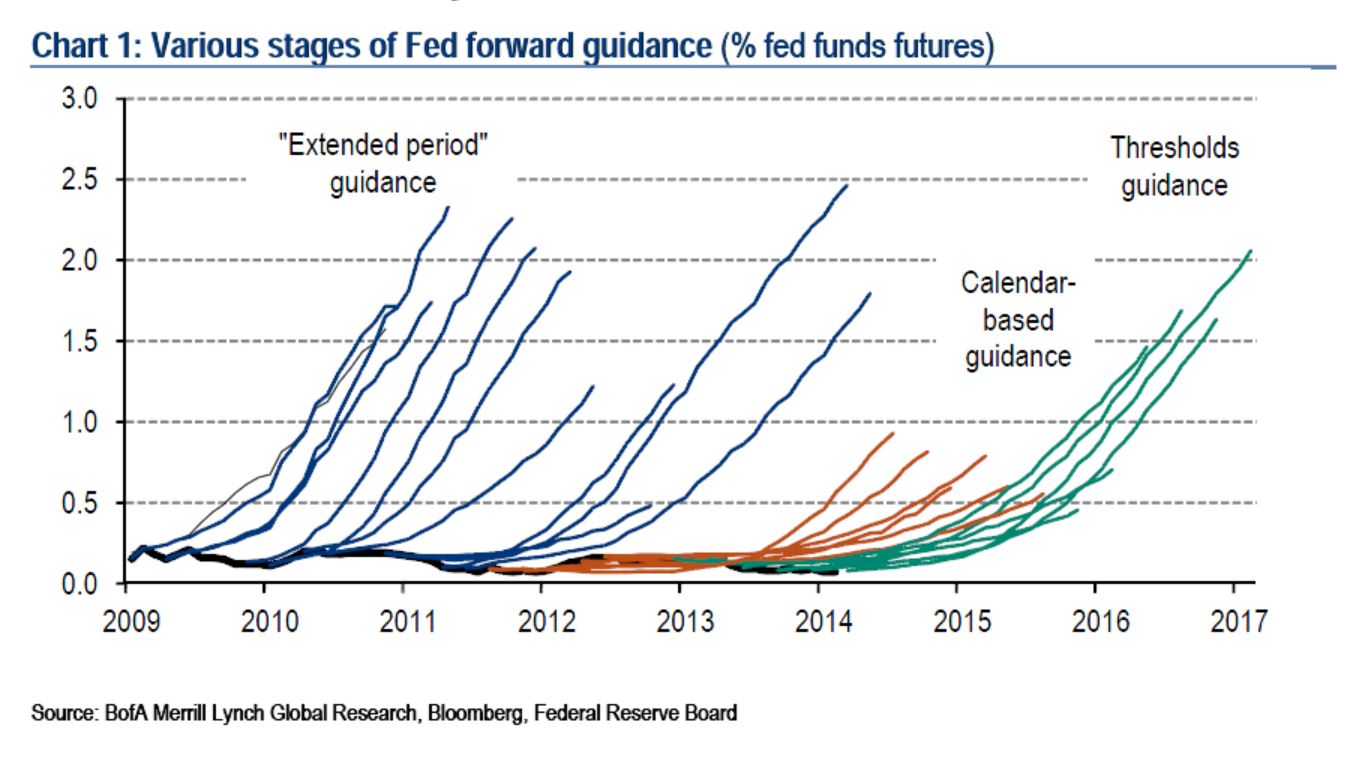

This forecast relies largely upon the expectations of the US Federal Reserve. But a chart by BofAML shows that may be a more perilous leap of faith than one might expect:

…in each of the last three business cycles, the market consistently mispriced the Fed, expecting rate hikes much too early. Let’s take a look at the forward curve after each FOMC meeting in the most recent period. Until the Fed announced “calendar guidance” in 2011, the markets always saw Fed rate hikes just around the corner. More recently, Fed attempts to guide the markets have flattened that curve.

Basically, since 2009, the Fed has itself been far too hawkish about the forward curve of its own interest rates (or has comprehensively failed to communicate the opposite to markets).

Advertisement

On this evidence alone it would probably be sensible to rely upon our own efforts to bring down the dollar than those of a perennially wrong Fed.

But there is more to be worried about. The two central pillars of expectations for a better US recovery are reduced fiscal drag (which is in the bag) and an ongoing housing recovery. The second of these is not looking very healthy today.

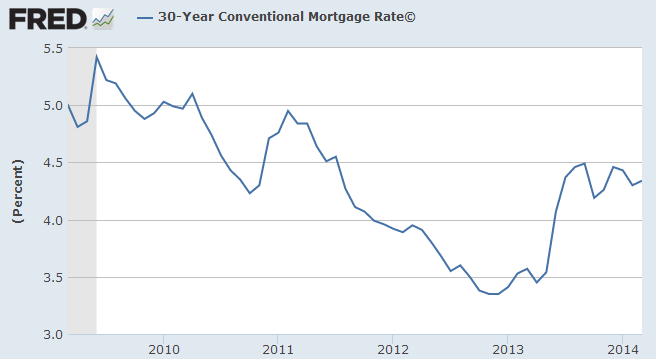

Last year I was concerned that US housing might be derailed by a continued rises in long bonds yields and their impacts the mortgage market. Well, yields didn’t rise. They’ve been falling. And mortgage rates have been trending down since September 2013 too:

Advertisement

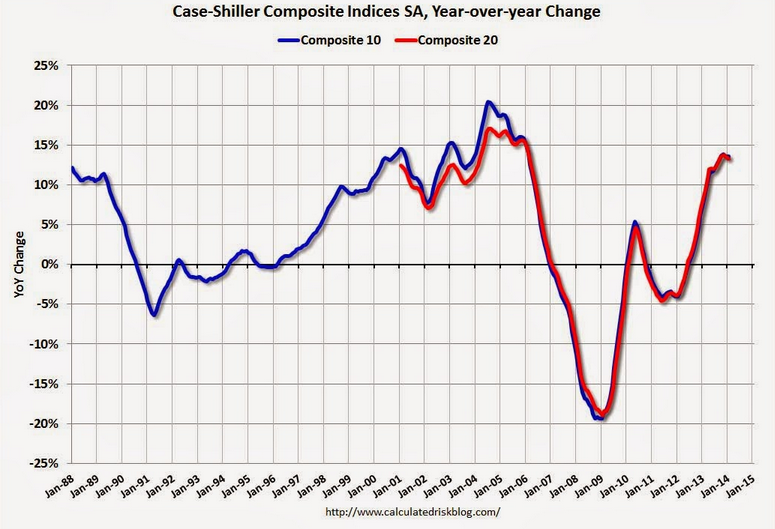

But US housing has still slowed, a lot, and does not appear to be firing up for anything more exciting than consolidation.

Year on year house prices are still up handsomely but they’ve hardly moved since September last year when interest rates hit their peaks and they will begin falling away sharply in annual terms soon (all charts from Calculated Risk):

Advertisement

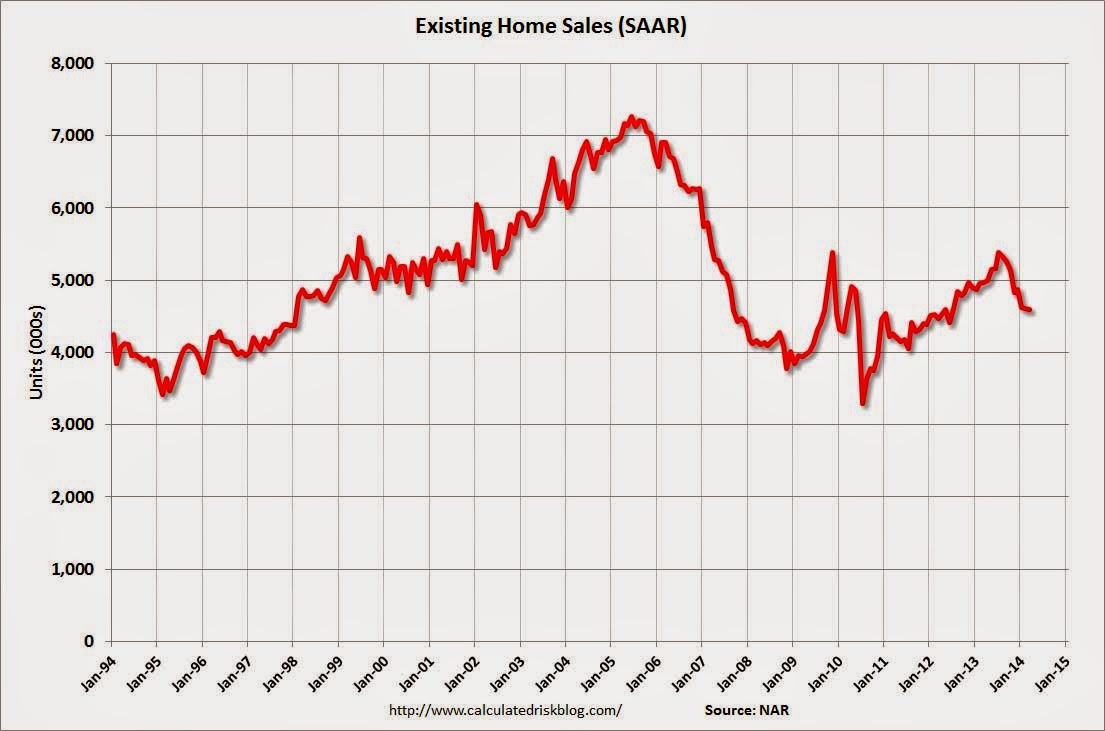

Existing home sales volumes have slipped:

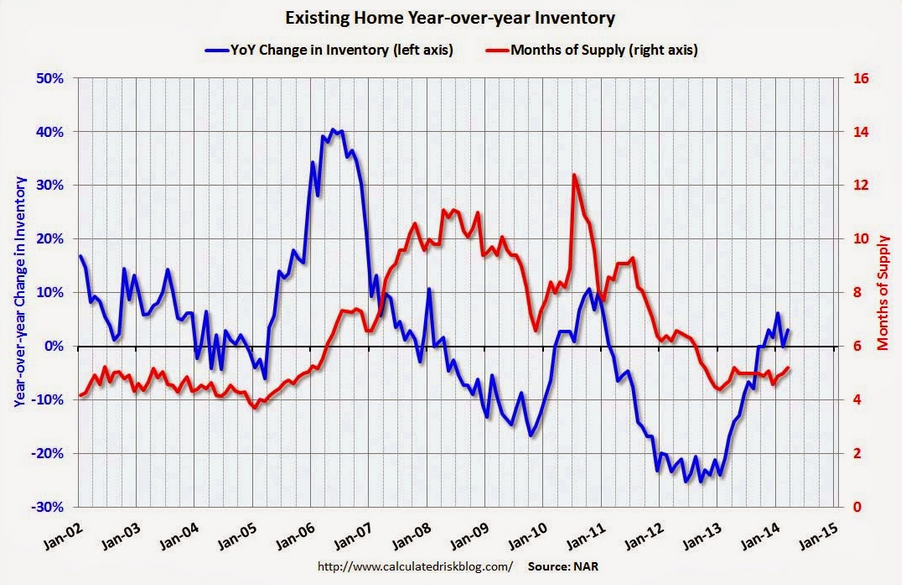

Inventories have bottomed and are climbing (though are still low):

Advertisement

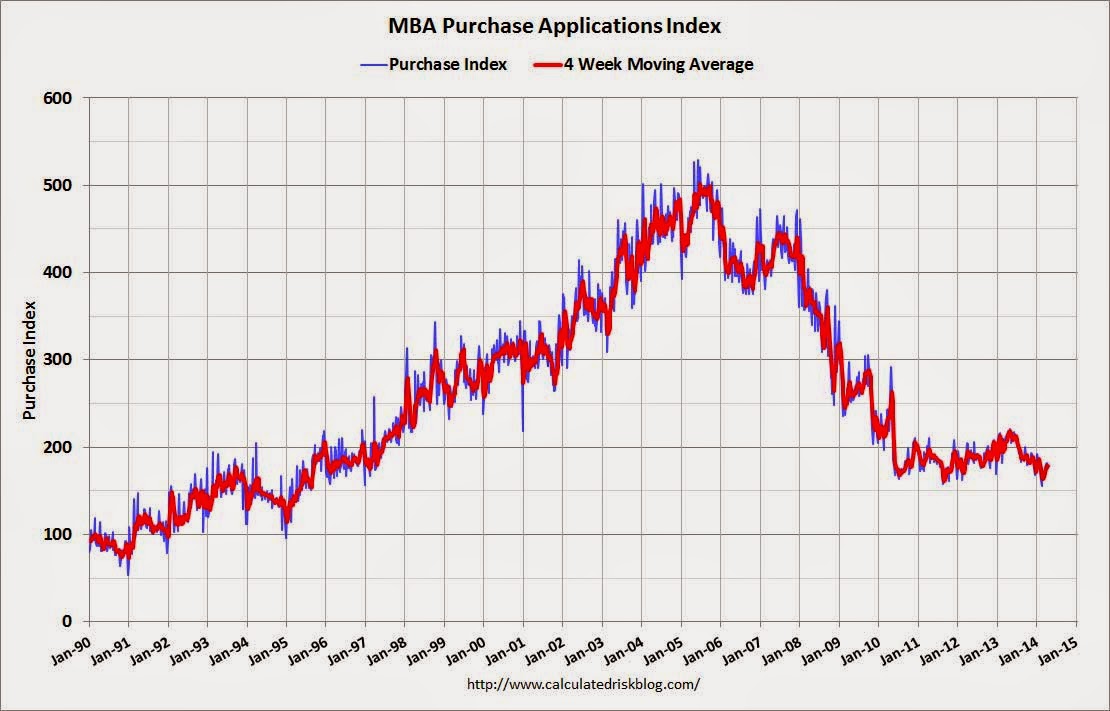

Mortgage originations are also very slow, hovering at post GFC lows. Any number of Wall St banks have indicated as much this earnings season and it’s obvious in weekly data from the major banks (which does not capture non banks so does understate the reality). For new purchases:

Advertisement

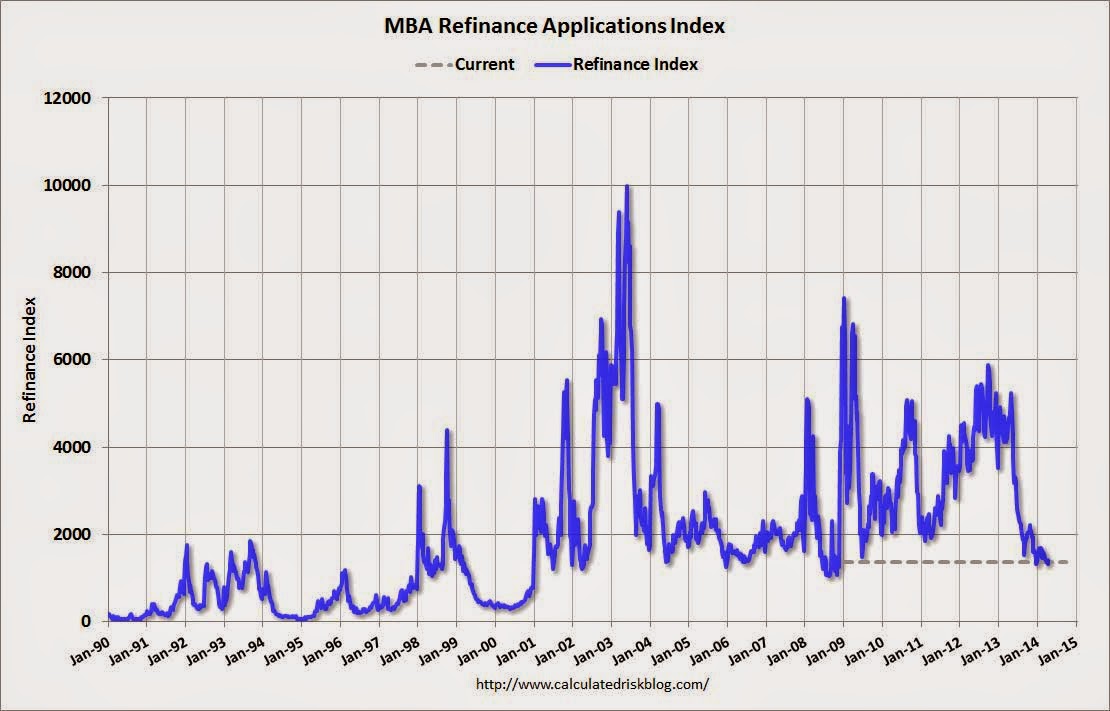

And refinancing:

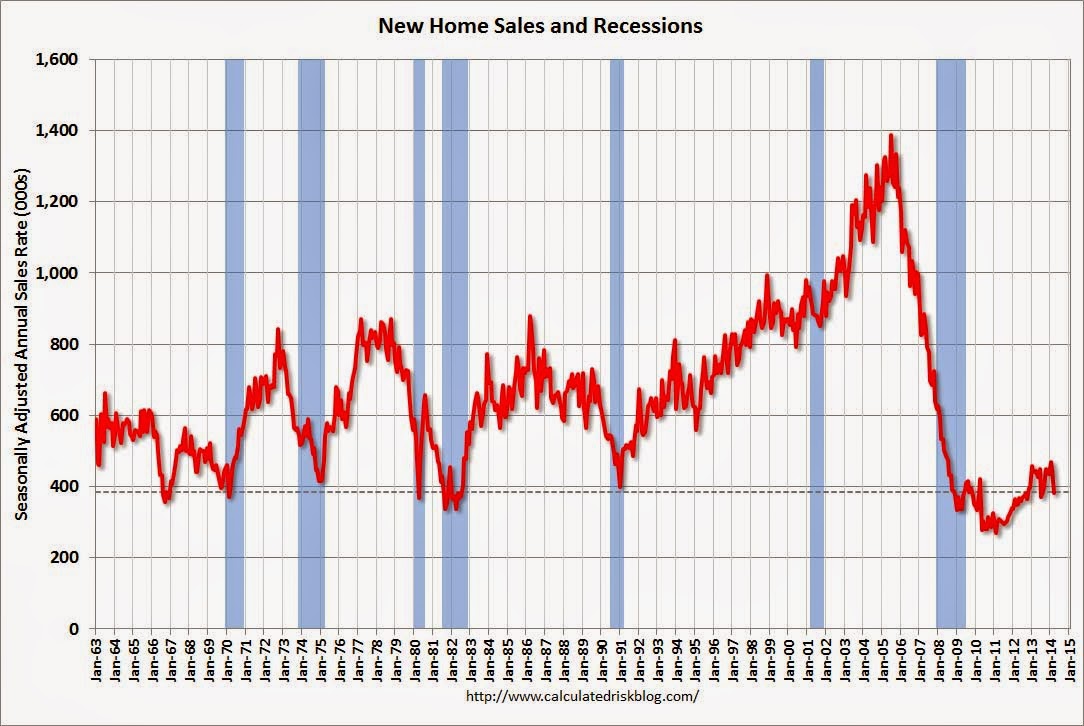

Most worrying for growth, is that the same slowdown is becoming apparent in new homes. Sales data for March out last night was terrible, showing no post-winter snap back:

Advertisement

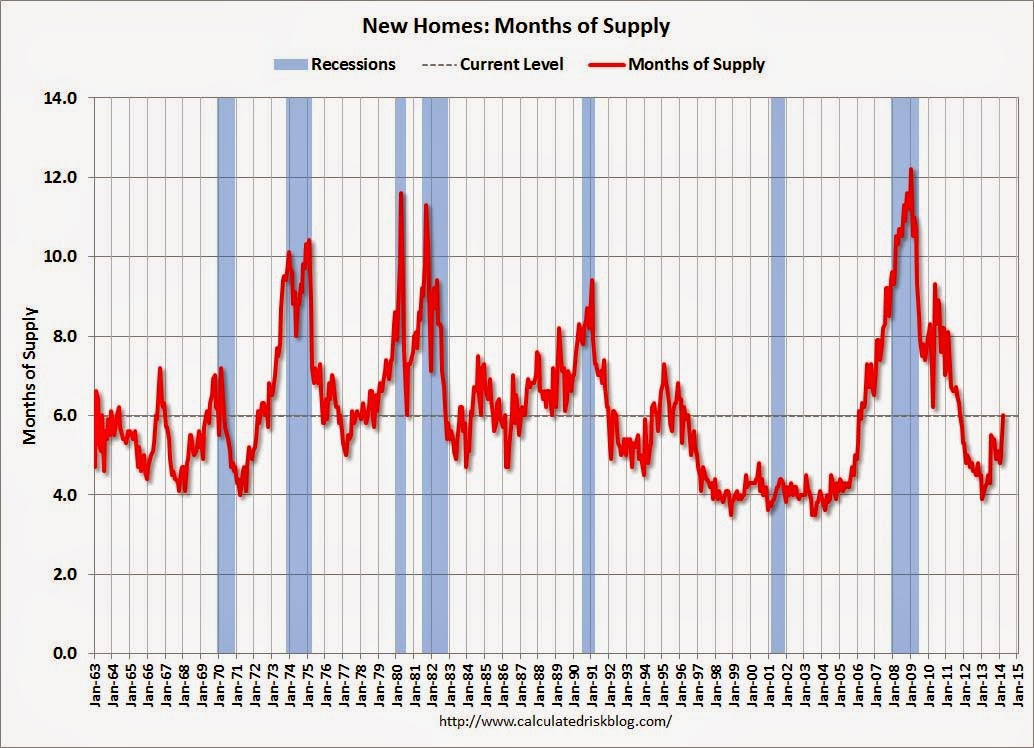

And months of supply is suddenly back in the normal range after a period of shortage:

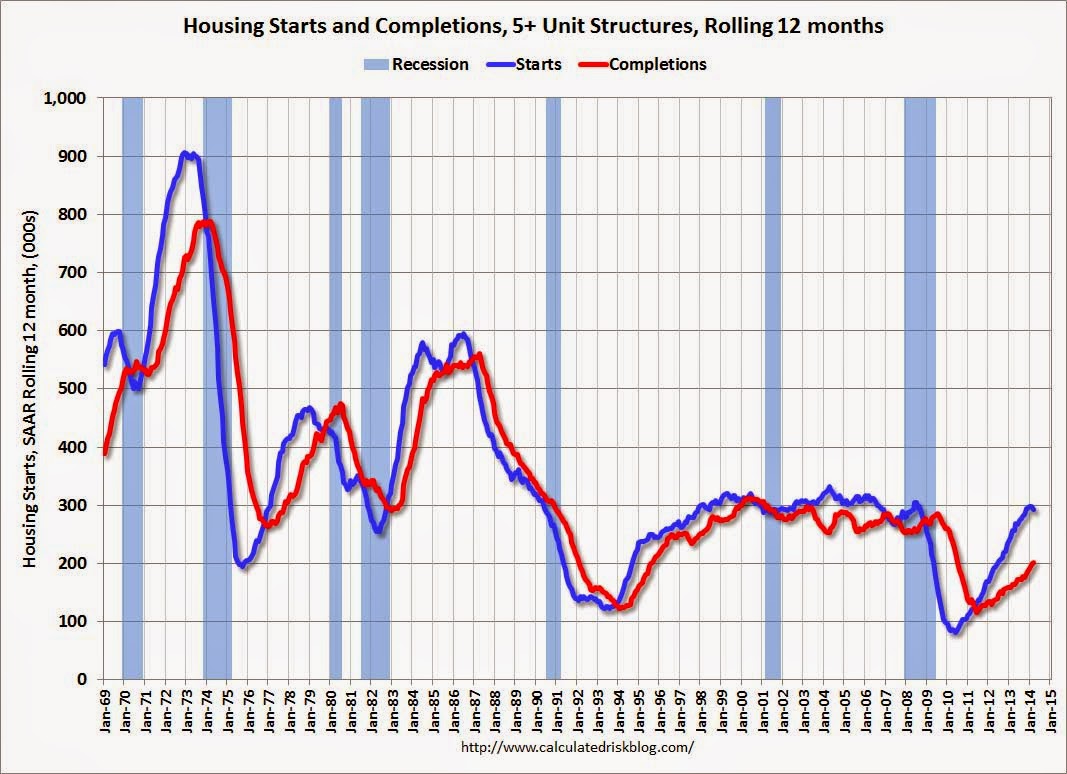

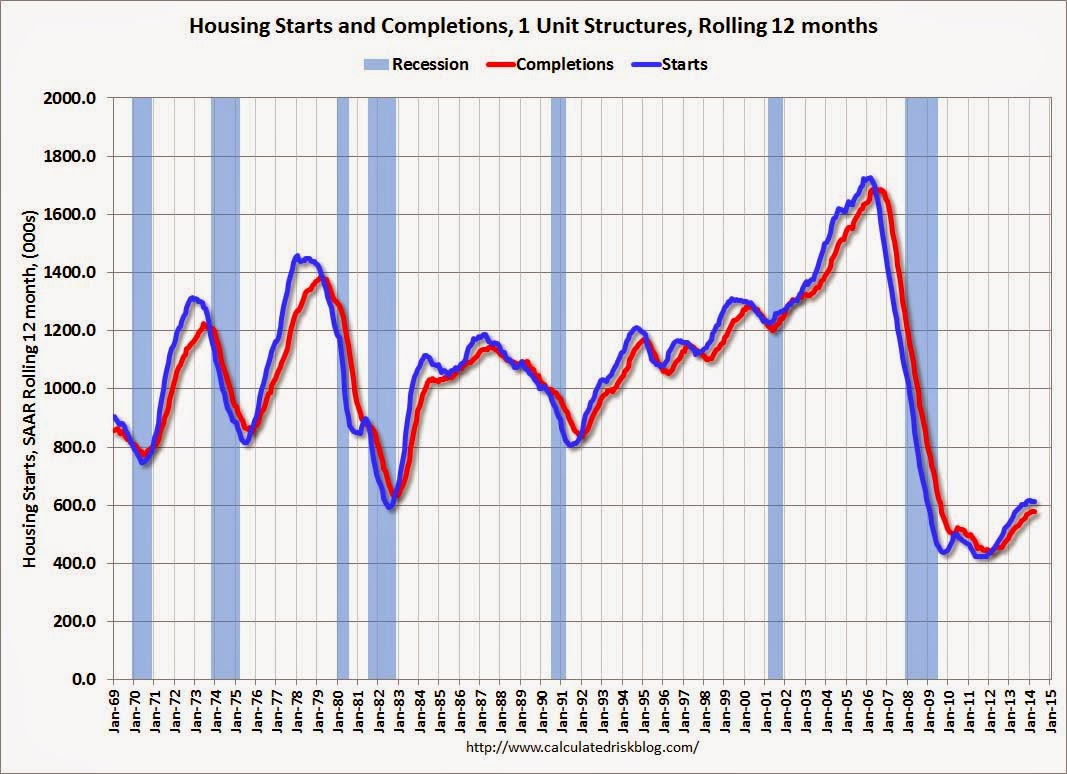

Housing starts are looking toppy too. Units recovered well from the crisis:

Advertisement

But houses did not and now look shaky:

Some of these are definitely weather effected but the emergence from winter is not looking all that sprightly. If new home sales follow prices (as they do just about everywhere) then just how robust can we expect 2014 housing construction to be?

Advertisement

There are other worrying signs too. One powerful updraft in the housing market has been the shift by Wall St into becoming a landlord in distressed property areas, buying 7.5% of all residential properties last year. Like Australia this has had an over-sized impact on prices owing to their better liquidity but that trend has also reversed dramatically since interest rate have threatened to normalise. Renovations are also down sharply.

This is not an argument that the US is about to swing into recession. Nothing like it. But if its housing market does stall, including construction activity as well as prices, then the likelihood of US Fed tightening is rather obviously diminished and that will mean more upwards pressure on the Australian dollar for longer.

We really should be taking out insurance by taking our fate into our own hands.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.