Overnight, US stocks took a pounding, down nearly 2%, led by the NASDAQ down 3%+. Data was thin but pretty good with unemployment claims down sharply. Bonds were heavily bid too, driving long interest rates down to new lows. In forex, there’s no apparent “risk off”. Despite China’s lousy data yesterday, it’s satellite currencies retained gains as the US dollar fell.

This looks like a bursting mini-bubble combined with rising risks around Ukraine.

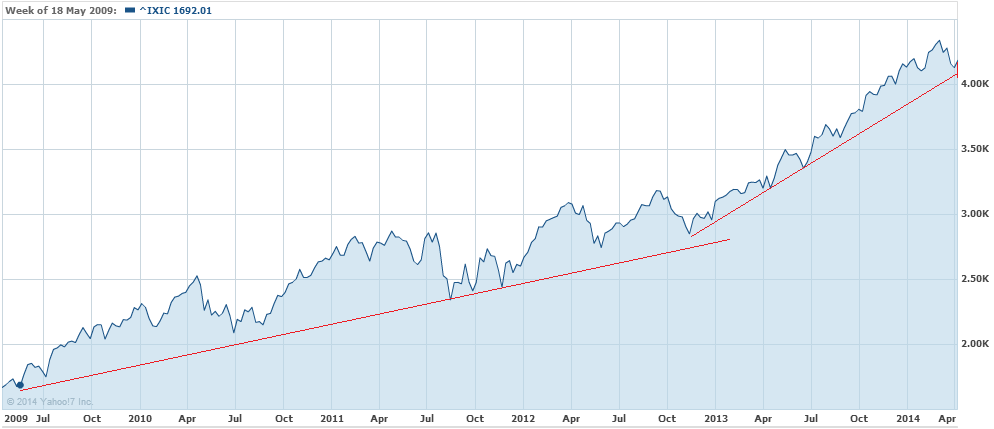

From the top then, here is the NASDAQ 5 year chart:

We are close to or through the major uptrend line. Numerous other supports are broken and momentum indicators are deep red, there’s a nice little head and shoulders top in place. Volatility is rising and the large daily price swings are feeling very much a like bearish dynamics. There’s no serious support level until around 3000 points.

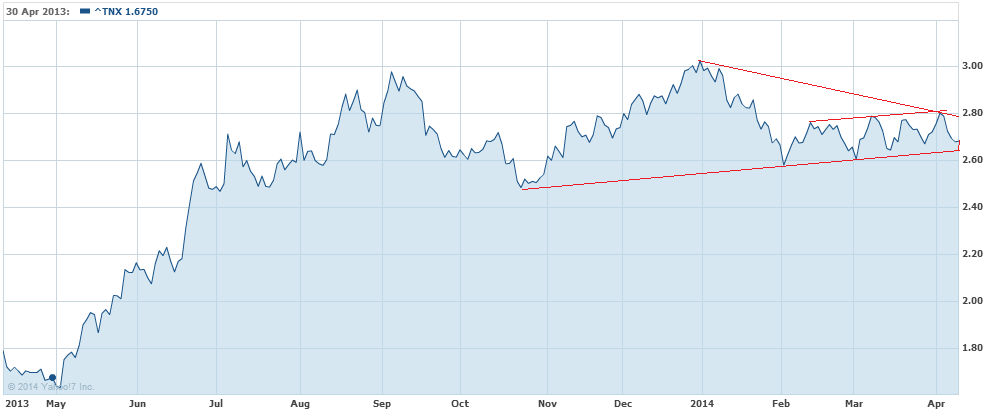

In bonds, the long end is firming fast. 10 year yields fell 2% and are sitting right on the bottom of a rising channel at 2.63%:

BofAML warned last that of this support breaks then 2.4% beckons.

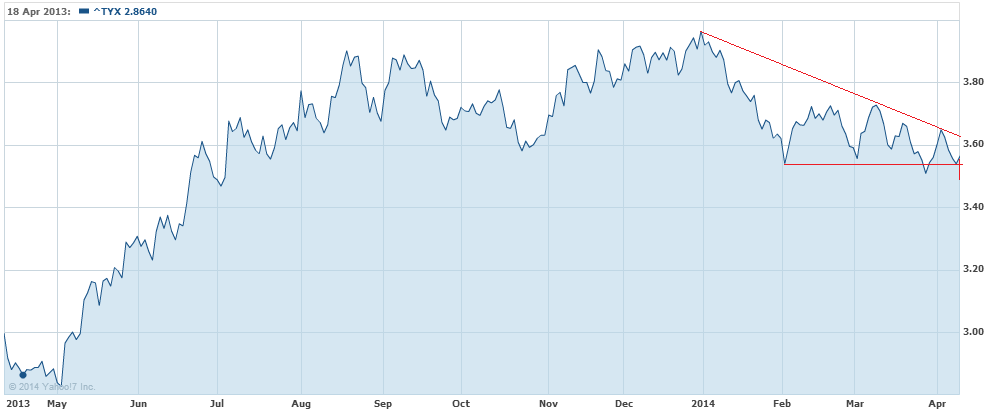

The 30 year is already bulled-up with its yields launching off the empire state building:

The descending triangle break is confirmed and hit a new low overnight, also down some 2% to 2.53%.

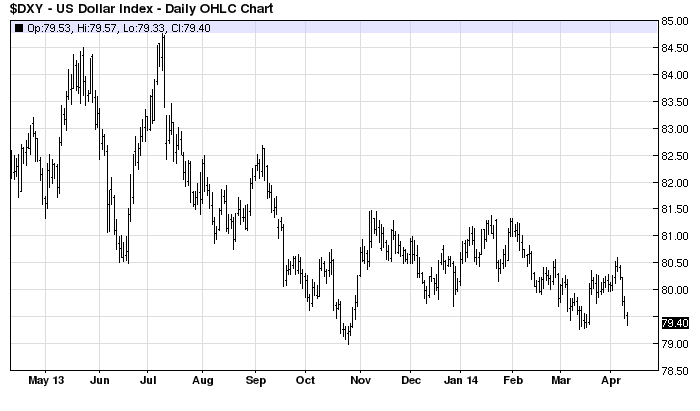

Yet, in forex, it’s all good. There’s no run to the US dollar, indeed, it’s the opposite:

And that’s keeping the emerging market reflation trade that has dominated much of this year buoyant:

Not even a hint of “risk off” on the US dollar crosses. The Australian dollar remained firmly above 94 cents.

It looks to me like the NASDAQ mini-bubble is bursting. That’s feeding what looks to be a decent US stock market correction in the making. I don’t see this a cycle-ending event or anything so dramatic. Falling interest rates and dollar via the long bond are supportive for the US recovery. But the prospect of ongoing taper and rate rises next year with the growing risks of more serious conflict in Ukraine is taking the froth off the high-beta, high valuation end of equity.

My feeling is this will run.