Capital Economics has produced a little note on China with which I entirely agree. It examines the slowing growth base case, as well as very plausible Chinese hard landing scenarios if reform has a little accident on the way.

China’s changing growth model

Before getting into what a hard-landing would look like, it is important to stress that this is not how we see things playing out. We expect growth in China to ease over the coming quarters, as policymakers try to strike the right balance between structural reform and supporting short-term growth. Slower growth that is less reliant on investment and rapid credit growth is exactly what China needs if it is to avoid a hard landing. As such, the recent slowdown could be seen as a positive.

A rebalancing of the economy away from investment and towards private consumption could create opportunities for some Asian economies.

Exporters of consumer goods should be big beneficiaries. Meanwhile, rising Chinese wages will force some manufacturers to look for alternative low-cost production bases elsewhere in the region, such as Vietnam and the Philippines.

However, while we think a hard landing will be avoided, there are warning signs in China that cannot be ignored. With investment the equivalent to 49% of GDP, China has one of the most unbalanced economies in the world. The pace of credit growth, which over the last decade has been nothing short of spectacular, is another cause for concern. In most countries, such strong credit growth has historically been followed by a financial crisis and recession.

The Chinese government recognises the scale of the challenges, and has unveiled an ambitious programme of reforms aimed at tackling some of the problems. However, there are no guarantees the reforms will succeed. In the rest of this Focus we examine what would happen if China’s rebalancing proves to be too little too late and the problem ends up being beyond the control of China’s authorities.

What constitutes a Chinese hard landing?

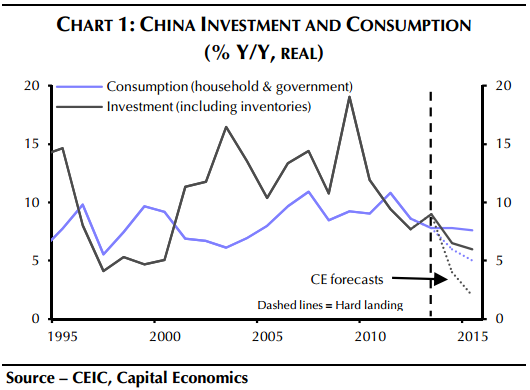

Our central scenario for China involves a gradual slowdown in (commodity-intensive) investment from the double-digit rates of the last decade to just 6% in 2015. (See Chart 1.) Accordingly, we see China’s headline growth slowing to 7.3% in 2014 and 7.0% in 2015.

In contrast, a hard landing would involve a much sharper downturn in investment. We think that a plausible hard landing scenario would see China’s real investment growth drop to 2% y/y. Consumer spending growth would also slow, as confidence faded and wage growth fell, but not as abruptly. These assumptions would deliver GDP growth of around 4% y/y.

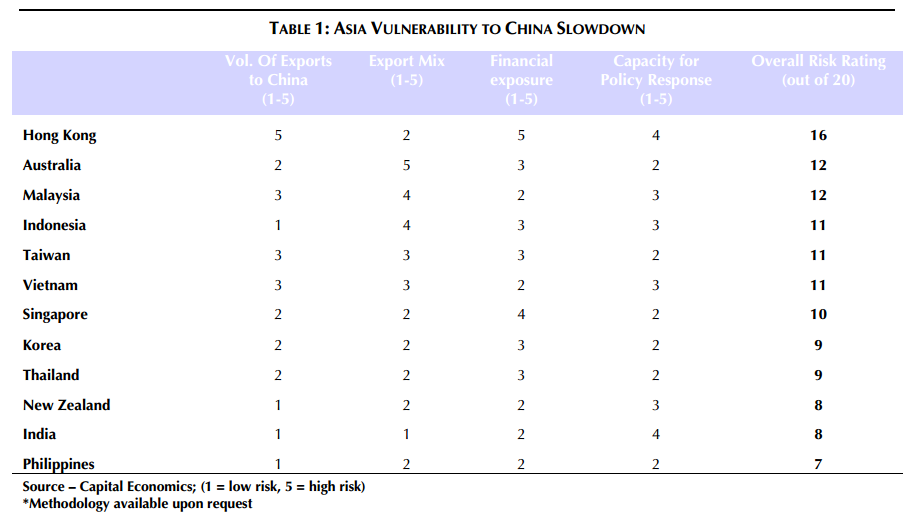

And here is Capital Economics’ table of relative vulnerability to a Chinese slowdown:

Advertisement

In short, outside of China, we’re the worst off. There is nothing “bearish” or “doomster” in this analysis. It is the simple sum of current Chinese policy.

A few points in conclusion then:

at a moderate or fast pace, the dollar is going to fall a long way

history is frowning upon the economist’s at the RBA and Treasury and their presumption of endless Chinese growth

this is a simple macroeconomic analysis and markets will make the outcome worse because they trade momentum and overshoot.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.