Stocks soared last night on decent data and Janet Yellen doving up everyone’s glasses. In data, the Chicago PMI missed but was firm at 55.9 and the Dallas Fed Index launched out of winter to 17.1. But it was Janet Yellen’s take on the labour market that sent stocks into renewed ecstasy. From Bloomie:

Yellen said today the Fed hasn’t done enough to combat unemployment even after holding interest rates near zero for more than five years and pumping up its balance sheet to $4.23 trillion with bond purchases.

“This extraordinary commitment is still needed and will be for some time, and I believe that view is widely shared by my fellow policy makers,” Yellen said at a community development conference in Chicago. “The scars from the Great Recession remain, and reaching our goals will take time.”

Yellen spotlighted as evidence “real people behind the statistics,” describing how one person, Vicki Lira, lost two jobs, endured homelessness and now serves food samples part-time at a grocery store.

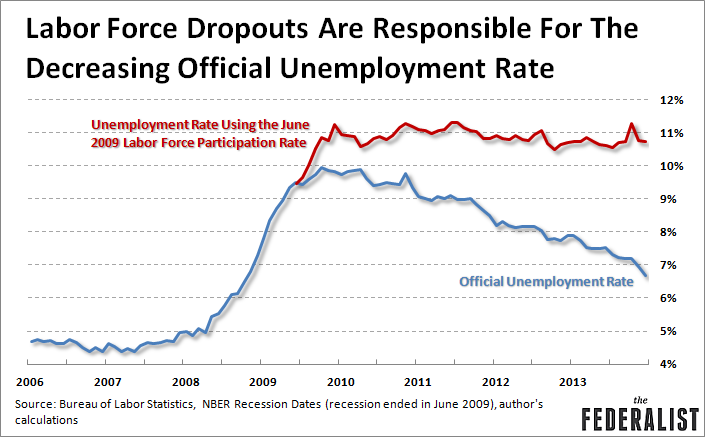

Indeed, Ms Yellen sees the inactive unemployed as a part of her brief and that means using underemployment and the labour force dropouts as a guide to Fed thinking as much as it does headline unemployment:

Indeed, she sees slack everywhere:

One form of evidence for slack is found in other labor market data, beyond the unemployment rate or payrolls, some of which I have touched on already. For example, the seven million people who are working part time but would like a full-time job. This number is much larger than we would expect at 6.7 percent unemployment, based on past experience, and the existence of such a large pool of “partly unemployed” workers is a sign that labor conditions are worse than indicated by the unemployment rate. Statistics on job turnover also point to considerable slack in the labor market. Although firms are now laying off fewer workers, they have been reluctant to increase the pace of hiring. Likewise, the number of people who voluntarily quit their jobs is noticeably below levels before the recession; that is an indicator that people are reluctant to risk leaving their jobs because they worry that it will be hard to find another. It is also a sign that firms may not be recruiting very aggressively to hire workers away from their competitors.

A second form of evidence for slack is that the decline in unemployment has not helped raise wages for workers as in past recoveries. Workers in a slack market have little leverage to demand raises. Labor compensation has increased an average of only a little more than 2 percent per year since the recession, which is very low by historical standards.5 Wage growth for most workers was modest for a couple of decades before the recession due to globalization and other factors beyond the level of economic activity, and those forces are undoubtedly still relevant. But labor market slack has also surely been a factor in holding down compensation. The low rate of wage growth is, to me, another sign that the Fed’s job is not yet done.

A third form of evidence related to slack concerns the characteristics of the extraordinarily large share of the unemployed who have been out of work for six months or more. These workers find it exceptionally hard to find steady, regular work, and they appear to be at a severe competitive disadvantage when trying to find a job. The concern is that the long-term unemployed may remain on the sidelines, ultimately dropping out of the workforce. But the data suggest that the long-term unemployed look basically the same as other unemployed people in terms of their occupations, educational attainment, and other characteristics. And, although they find jobs with lower frequency than the short-term jobless do, the rate at which job seekers are finding jobs has only marginally improved for both groups. That is, we have not yet seen clear indications that the short-term unemployed are finding it increasingly easier to find work relative to the long-term unemployed. This fact gives me hope that a significant share of the long-term unemployed will ultimately benefit from a stronger labor market.

A final piece of evidence of slack in the labor market has been the behavior of the participation rate–the proportion of working-age adults that hold or are seeking jobs. Participation falls in a slack job market when people who want a job give up trying to find one. When the recession began, 66 percent of the working-age population was part of the labor force. Participation dropped, as it normally does in a recession, but then kept dropping in the recovery. It now stands at 63 percent, the same level as in 1978, when a much smaller share of women were in the workforce. Lower participation could mean that the 6.7 percent unemployment rate is overstating the progress in the labor market.

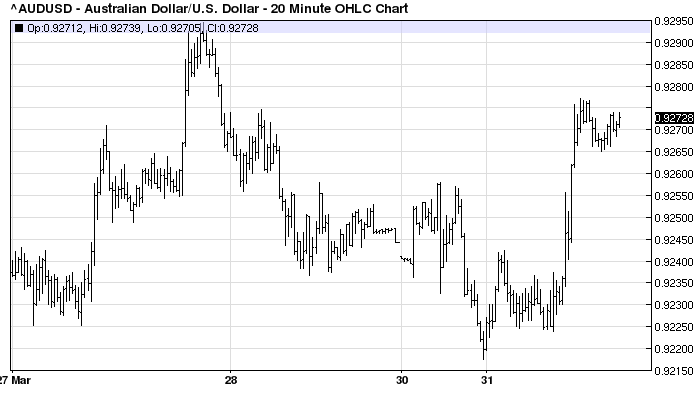

S&P to the moon! Australian dollar still simmering: