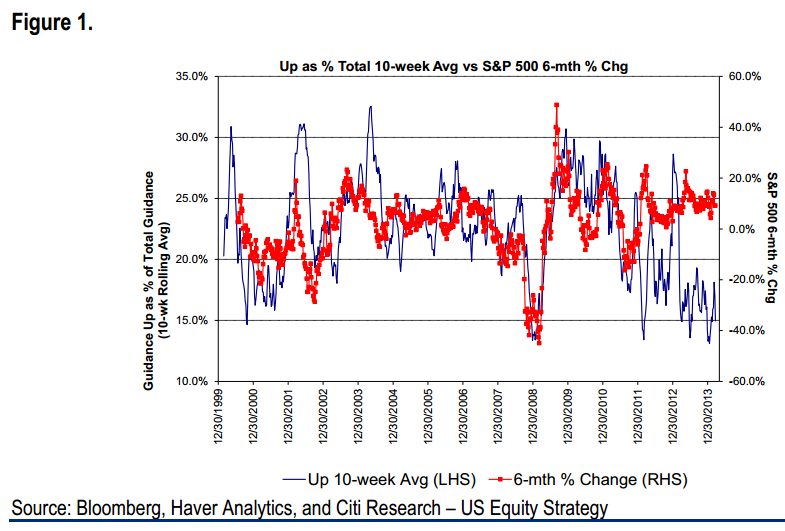

Earnings guidance traditionally has been a critical factor in stock price trend, but that has not been the case for at least nine months. Excess liquidity, money flows into equity mutual funds and exchange traded funds seem to have had more impact as corporate EPS forecasts have been cut with little effect to shares in an almost aberrational manner. However, as noted in February’s Chart of the Month (February Chart of the Month), some of this differing pattern reflected a catch-up of equity index levels to match the earnings trajectory since 2011.

The more recent inability for stock prices to gain traction may intimate discomfort with the earnings outlook as expectations have come in. Both sellside and buy-side projections have been trimmed since 2014 began, amidst weather disruptions, currency exchange rate shifts and emerging market challenges. Thus, it is likely that some stability of EPS beats might be needed to reinvigorate equities and the earliest opportunity for that to occur may come in the next few weeks as 1Q14 results get reported and management teams provide more insight during quarterly conference calls.

The dip in guidance is quite steep and would suggest that further substantial downside is unlikely barring a recession and/or exogenous shocks. With credit conditions in good stead, capital spending plans rising and hiring intentions climbing, it seems improbable that a new imminent economic downturn is in the making especially since the Fed only may begin to raise short-term rates in 15-18 months. While one can never rule out unexpected circumstances, it seems more plausible that share prices drift until a new direction is perceived.

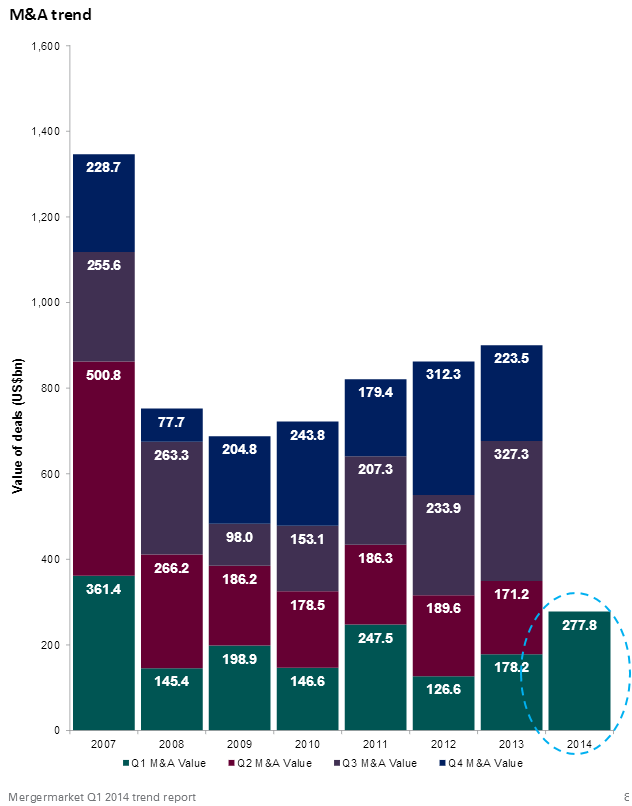

US M&A activity is picking up steam. Deal volume in the first quarter of this year was the highest since 2007 (in dollar terms). The total of $278bn of transactions includes high profile deals such as Time Warner, Forest Laboratories, and WhatsApp.

Moreover, M&A transaction volume growth for both large and middle market firms is poised to accelerate this year. Here are some reasons:

1. US corporations currently hold record amounts of cash (see story) and shareholders want to see action. While dividends and stock buybacks have been popular recently, many firms are looking toward growth strategies.

2. The market has recently rewarded companies that are doing deals by giving them higher valuations (Facebook was an exception), encouraging CEOs to be more aggressive with acquisitions.

3. Financing costs are still quite attractive. US high yield spreads for example hit another post-2007 low last week as fixed income investors (including “shadow” banking participants) look to buy corporate paper. This allows for more leveraged buyouts even at higher valuation multiples.

4. Private equity funds, particularly some of the larger ones are having a fairly impressive start this year with their fund raising efforts (see example). The first quarter has been the strongest since 2008 according to Preqin with some $95bn raised. This capital has to go somewhere.

5. A great deal of near-term fiscal and monetary policy uncertainty has been removed from the market (see post). The macroeconomic environment in the US should support M&A activity.6. The US stock market strength, while making target companies more expensive, is providing more buying power for strategic acquisitions. Companies will be using their (sometimes overvalued) shares as “currency” to do deals.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.