The April NAB Business Survey is out and shows a mixed result with confidence down sharply but some stabilisation in conditions:

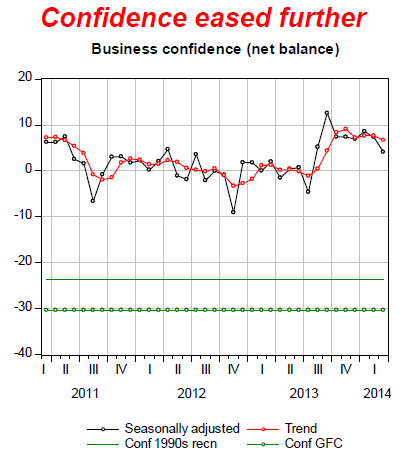

Business confidence was pared back in the month to its lowest post-election level, which is also below its long-run average. It appears as though firms are responding to the ongoing sluggishness in business activity, which has not quite reflected the exuberance of firms in past months. The stubbornly high AUD, uncertainty over the global economy and the potential for significant ‘belt tightening’ in the upcoming budget, could all have contributed as well. Mining continues to be the least confident industry.

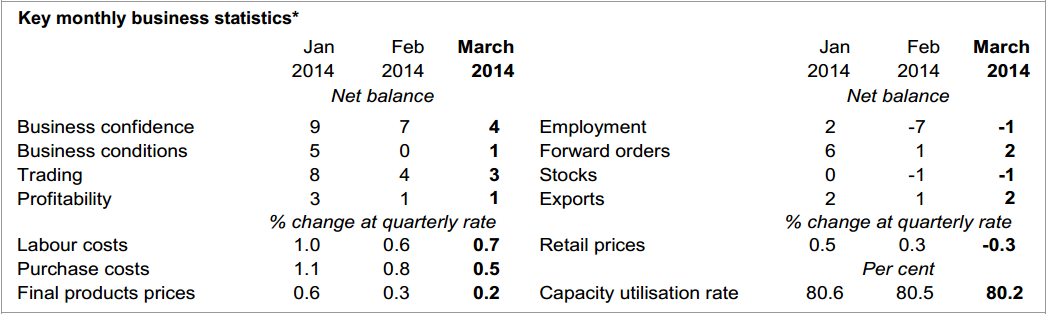

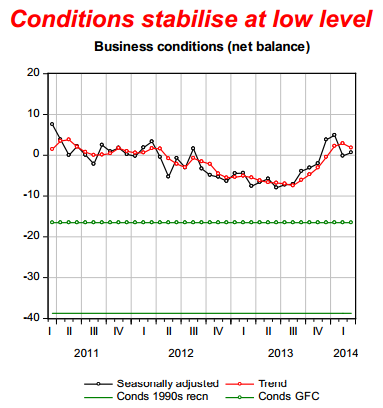

Business conditions rose only slightly in the month and are still pointing to a sluggish recovery in business activity. Nevertheless, most industries recorded an improvement in business conditions in the month, with the exception of transport & utilities and wholesale. Conditions facing wholesalers deteriorated heavily in March and are by far the weakest of all the industries covered in the survey – a concern given its characteristics as a bellwether industry. Recreation & personal services continue to enjoy the highest level of business conditions. Sales eased in the month, while forward orders and employment both remain soft

Our wholesale leading indicator suggests much weaker underlying conditions, pointing to further below trend economic growth in the first quarter of 2014 of around 2½% and continuing weakness into Q2.

Inflation pressures softened again in the month due to lower input cost pressures. In particular, purchase cost inflation eased in the month, resulting in a sharp fall in retail prices. Soft labour costs growth is consistent with increasing slack in the labour market.

This survey is a nice representation of where we’re I think the economy is headed. Both confidence and conditions have recovered but remain subdued. That’s how it will stay in my view with a sideways grind ahead as the mining bust drags and cyclical forces lift:

Advertisement

Bottom line: we’ve already had the recovery. From here it’ll be a tough slog that looks good on paper owing to high net exports but will feel much harder on the ground outside of a few narrow sectors.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.