The wholesome MB effect on the mainstream echo chamber continues today at Business Spectator as Rob Burgess picks up the manufacturing banner:

Commodity producers are price-takers, and Australia’s shortish terms-of-trade boom (which is now ending) has given us the false impression that we have a sustainable competitive advantage in the things that have made us rich: predominantly iron ore and coal.

…Sorry to dampen that romantic nationalism, but we can’t. A trade surplus is one thing, but to pay for our imported food, wine and clothes (and everything else) sustainably we need a current account surplus, which measures all income flowing in and out of the country, not just the value of what we bought/sold.

We are selling a lot of minerals. But given that most of the capital to build the mines has come from abroad, a large part of profits must flow home as well. So we have a trade surplus and a continuing current account deficit.

…Only by addressing the current account deficit in the long term — by boosting value added industries — can Australia maintain anything like its current prosperity.

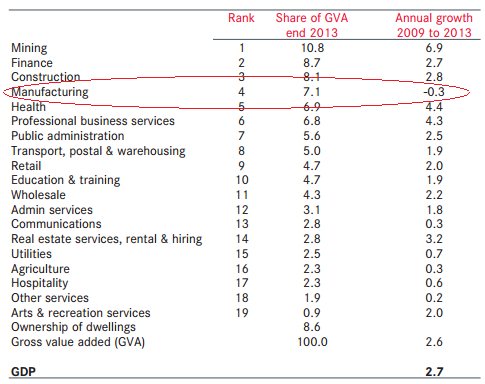

Here is a recent table from Westpac showing how that adding of value is going:

As I’ve said before, these levels of manufacturing’s contribution to growth are the lowest in the OECD and roughly half those of the supposedly de-industrialised US and UK economies. On balance that will mean lower productivity growth, less export opportunities and higher imports. And don’t forget that the ABS capex report is forecasting much more shrinkage to come.

This is something of a boiling frog problem for the country. The decline in our terms of trade is slow enough and rising gas exports will be large enough that we’re only feeling the heat slowly and the manufacturing crisis can be ignored.

But our standards of living will still slowly boil away. There are only three ways to grow your economy. Either the external sector must be running a surplus or the public and/or private sectors running increasing deficits and accumulating more debt. We’re running into political blockages on the former and peak warnings on the latter. From AFR today:

The return of cheap and easy access to financing for lenders has sparked fears Australia’s heavily geared household sector may take on too much debt.

After the global financial crisis interrupted a multi-decade surge in household indebtedness, Australians are gradually starting to gear up again.

According to the Reserve Bank, the ratio of debt to disposable income has edged up from 145.1 per cent in mid-2012 to a three-year high of 148.8 per cent last December.

…Nomura analyst Victor German said households would be unable to expand their borrowing like they had throughout the 1990s and 2000s, when borrowing easily outstripped income growth.

‘‘It does not feel like there is a lot more scope for households to continue to leverage up,” Mr German said.

What we need to be doing is repairing competitiveness and productivity so that manufacturing and other tradables can begin to invest again, we can make our own stuff rather than import it and export it to others. As Burgess says, only that way can we leap from the slowly boiling saucepan in the long run.