Here’s the Kouk yesterday:

The favourable news on the economy is unrelenting.

After the flood of extremely positive news last week, there has been further reinforcement of the clear upswing in a couple of series released in the last day and a bit.

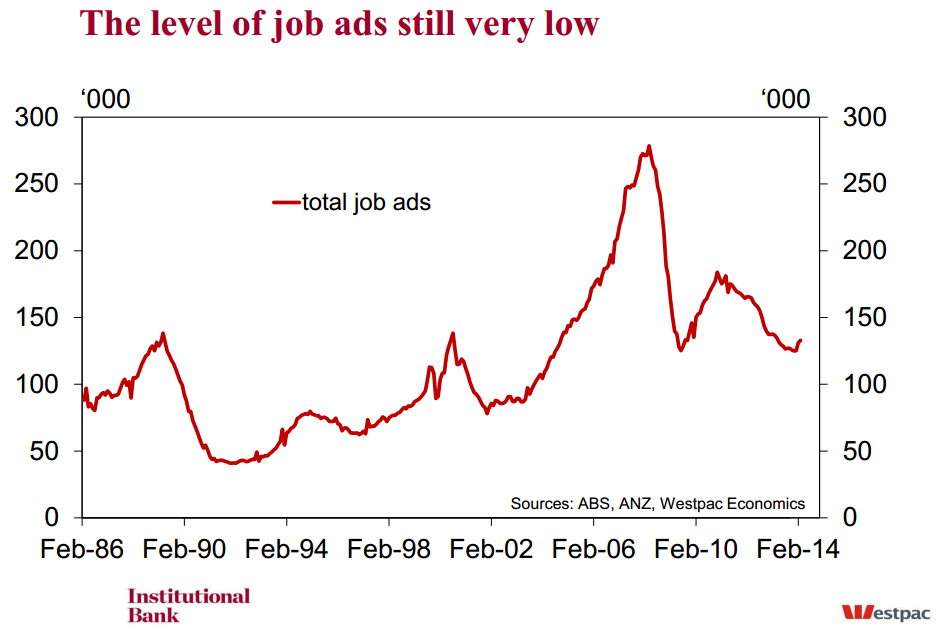

Yesterday saw the number of job advertisements, as measured by the ANZ, lock in five straight months of increase in trend terms. There is now no doubt that employment growth will also lift in the months ahead and the unemployment rate will start to fall very soon.

Adding to the news of decent growth is today’s report of NAB’s measure of business conditions – up only 1 point but up nonetheless, while business confidence slipped 3 points from recent gains to still be at +4 points. The business sector is clearly enjoying the fruits of the surge in housing construction, strong retail sales and rampant export growth which is offsetting the softness in manufacturing and mining investment.

It is now very difficult to find a part of the Australian economy that is weak, with the obvious exception of mining investment. But even that decline is, so far, moderate and is being overwhelmed by the favourable news in the other 90 per cent of the economy.

There are some other snippets of news worth considering. Eight days into April and the RPData 5 capital cities house price series continues to move higher, up 0.1 per cent after a record 2.3 per cent jump in March. The annual increase in the series is 10.8 per cent. The house price boom must be increasingly uncomfortable for the RBA and the urgency for an interest rate hike is becoming evident to even those who used to be gloomy about growth.

And even commodity prices are higher today than at the start of the month when the RBA Board last met. According to the Reuters/Jeffries CRB index, commodity prices are 0.8 per cent higher in the past week and are close to their highest level in more than a year.

All up, it seems full steam ahead for the Australian economy to 3.5 per cent GDP growth and inflation skirting the upper bound of the RBA target range at 3 per cent. Who knows, the unemployment rate this time next year might be nearer 5 per cent than 6 per cent.

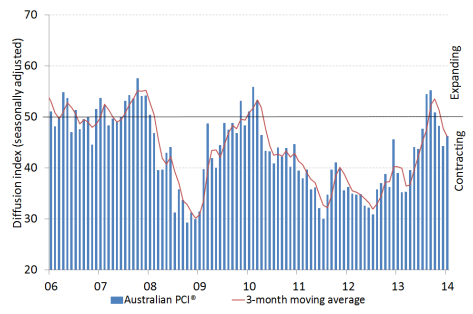

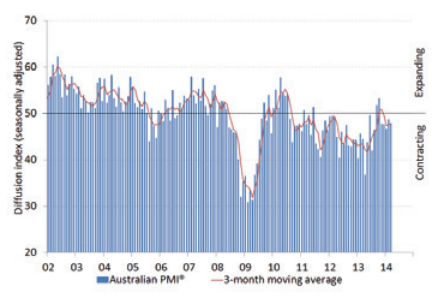

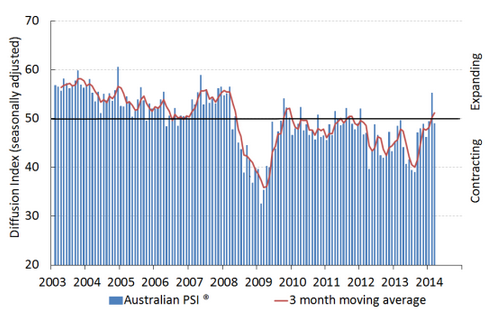

OK, it’s a slow news day so I’ll rise to that challenge. Here are three areas of weakness to start with. All three AIG PMIs – services, manufacturing and construction – all in recession:

That’s Kouk’s 90% of the economy right there. These survey’s aren’t top tier data admittedly but neither should they be completely ignored. As well, here is the ANZ jobs ads chart:

We’re off the bottom, which is great, but with the employment dimension of the capex cliff yet to kick in it’s hardly a large or secure surge.

The NAB survey was also mediocre with both conditions and confidence below long term averages. Consumer sentiment has fallen heavily from last year and is below long term averages. Retail sales last week were weak, albeit after a strong run.

The CRB index does not include bulk commodities, which is where all of our exports are, including coal and iron ore, which make up some 50% of the terms of trade. These are still down some 10% from the beginning of the year despite the recent snap back.

That is not to say that there aren’t green shoots. There are. House prices in the east are out of control and stocks are holding up well too. I expect some better news in the labour market as a result. But there is plenty of evidence to suggest only a tentative and struggling economic recovery beyond that, before we even get into a more serious discussion about structural challenges.