After multiple twists and turns in Q1, the US, European and EM equity markets have delivered outcomes only a short distance from flat. In part this is due to the lack of persistence in macro drivers since the year began and their shifting configuration relative to most of last year. In a sense, we are still waiting for the curtain to rise on ‘showtime’ for the US recovery.

‘Showtime’ after a delayed opening

We think that point is now at hand: our forecasts imply an acceleration in global GDP growth, excluding Japan; the US economy is set to bounce back from the drags from weather and destocking; and China’s weak start to the year should give way to something a little better, as modest stimulus falls into place. At the same time, US financial conditions are at their easiest levels post-crisis, and we expect easing measures from both the ECB (quite likely tomorrow) and the BoJ (in April or June).

A more cyclical tilt to markets

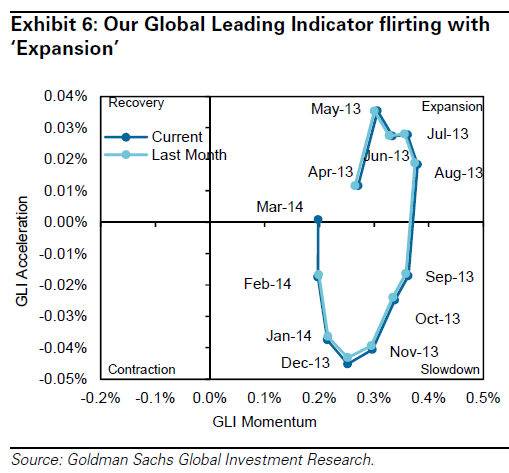

These dynamics have begun to influence market pricing more clearly in the past couple of weeks. And our Global Leading Indicator has shown tentative signs that a phase of Expansion may be starting. But we think the reality of a better cyclical picture has not yet been fully priced. If we are right, the improving cyclical environment should continue to support equities, while pushing yields higher. It should also support a pro-cyclical stance within each of the major asset classes.

The so-called Chinese stimulus is two-fifths of bugger all so I would discount that part of the analysis. But China should stabilise even though ongoing credit shocks will roil markets, not least iron ore.

But I buy the US recovery story in a moderate way as it bounces out of winter. The labour market is slowly improving there. Sober Look has more on that today:

We are seeing signs of significant improvements in US labor markets. The ADP report today was certainly an indication of recovery from the winter slowdown.

ADP: – Mark Zandi, chief economist of Moody’s Analytics, said, “The job market is coming out from its deep winter slumber. Job gains are consistent with the pace prior to the brutal winter. The gains are broad based across industries and business size classes. Even better numbers are likely in coming months as the weather warms.”One area to watch in the ADP report is construction (see post), as construction payrolls have consistently increased each month over the past year. With demand for rental units remaining high, this sector could pick up quickly.

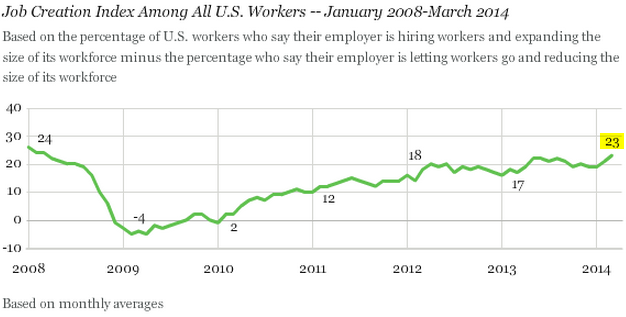

But signs of improvement go beyond the ADP measures. Gallup’s Job Creation Index for example rose to the highest level since 2008.

Gallup: – U.S. workers in the private sector are reporting a more positive jobs situation where they work than at any point in the past six years. Combine this with state workers’ record-high job creation reports and the year-over-year improvement from federal workers, and March’s promising Job Creation Index reading would appear to be a positive sign in the long recovery from the 2007-2009 economic recession.

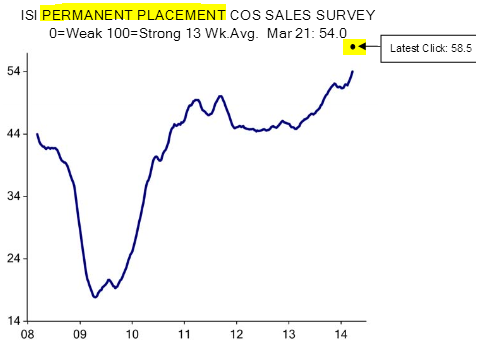

Furthermore, the ISI’s survey of permanent placement (recruiting) firms shows a surprisingly robust improvement in activity recently.

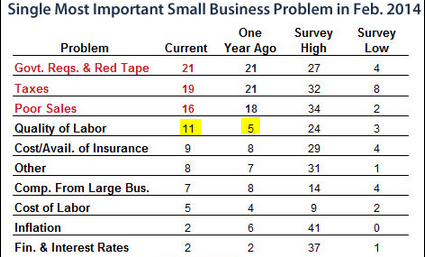

Companies are paying more to find employees, which is consistent with the recent report showing that small businesses are complaining about labor quality – something they weren’t doing much a year ago.

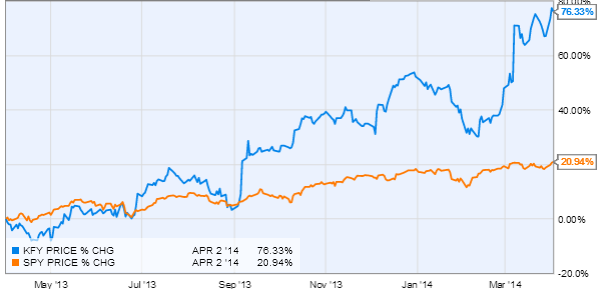

The markets are starting to recognize this change in labor markets, with the 10-year treasury yield rising nearly 12bp from a week ago. Another market example of this improvement is the recent spectacular rally in the shares of a large recruiting firm, Korn Ferry (KFY).

Clearly we will see some volatility in the official payrolls numbers going forward, but the signs of US labor markets firming are unmistakable.

Advertisement

Ironically, the recent flattening of the yield curve has been encouraging too, in so far as it appears there’s no imminent danger of a bursting bond bubble derailing the economy.

And with the great dovish wings of our Janet embracing it all, I can’t see why the S&P won’t power on into space, for now.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.