From the AFR:

Earnings forecasts for cyclical stocks are defying historical downgrades, suggesting economic growth is re-balancing in the wake of the mining investment boom.

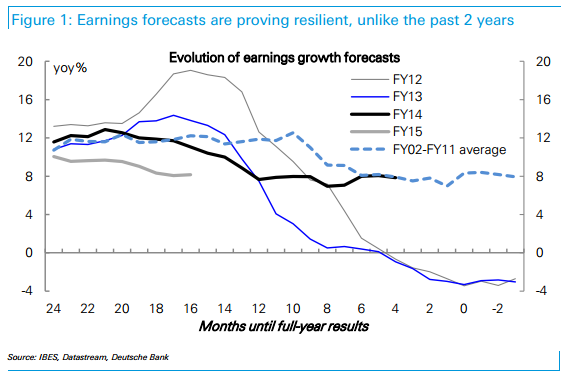

The consensus of analysts expect earnings to grow around 8 per cent in the financial year to June 30, 2014, a forecast which has held steady for the past eight months, according to Deutsche Bank equities strategist Tim Baker.

Well, I read the report, and was not terribly impressed. Here is it’s summary:

1. EPS forecasts holding up nicely, and valuations look reasonable for cyclicals

The consensus of analysts expects earnings to grow ~8% in FY14, a forecast which has held steady for the past 8 months. This stability is a marked change from the past few years of heavy downgrades, and provides evidence that the earnings cycle is turning, led by cyclicals. Valuations also favour cyclicals in our view. Resource stocks are cheap vs the rest of the market, trading on a PE of 13¼x (a little below the 10yr avg). Cyclical industrials don’t look cheap on a PE basis, but offer upside as earnings normalize from cyclical lows. These stocks comprise 18% of the market capitalization, vs the 10yr avg of 20%.2. Businesses are reporting the best conditions in 2½ years

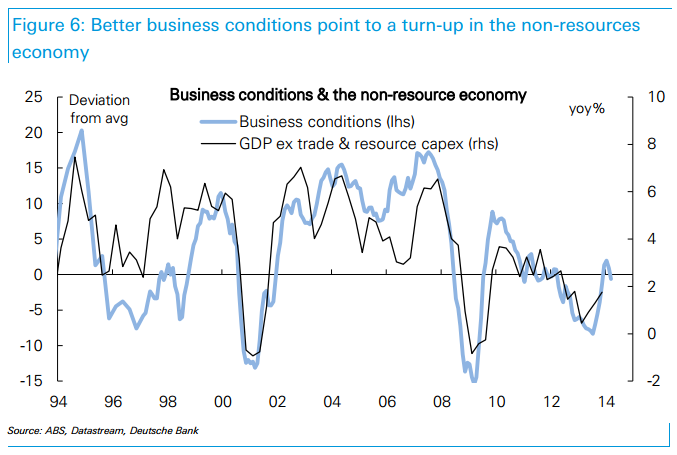

The past 4 months have seen businesses report the best conditions since mid- 2011. Sentiment at current levels points to the non-resource economy getting back to trend growth, which would support earnings for domestic cyclicals.3. The turn in the labour market should boost household income & spending

After an 18-month downtrend, employment growth looks to be turning up. This has been foreshadowed by improving growth in hours worked, and also by partial indicators like the NAB survey & job ads. These indicators point to further strengthening in hiring, which will add to household spending power.4. Chinese growth should get a boost from exports

China has reported heavy falls in export in the past 2 months, but this data looks distorted. In underlying terms export growth remains positive, though with some slowing recently. We expect net exports to add moderately to growth this year, for the first time since 2010. With the pick-up underway in US & European growth, history would suggest this is quite achievable.

OK, here’s the riposte:

1. It’s too early to say whether cyclical stock downgrades are holding up better that previous years, which is clear in the chart:

2. Business conditions bounced post-election and have since been waning. With the capex cliff, the economy could very easily return to last year’s lousy demand conditions in the second half:

3. The turn in the labour market may help spending but it will do nothing for incomes, which will keep falling owing to the terms of trade slide. The labour market will also only turn up only very slowly. That means consumption will be funded either out of more debt or less savings; a questionable proposition given post-GFC household conservatism and not very sustainable either way.

4. What are Chinese exports even doing in this report? If the Chinese economy is going to support Australian cyclicals then it will be through boosting fixed asset investment not exports. Rising exports might actually be bad for Australian demand if they prevent Chinese stimulus aimed at more building.

Deutsche recommends Toll, Asciano, Boral, Bluescope, Stockland, Lend Lease, Harvey Norman, Nine, Crown, Rio & BHP.

The first two are bad choices given the mining capex cliff and its impact on haulage, as we saw last week in McAleese. The last two are bad choices because falling iron ore prices are not fully priced in equities despite cost cutting. Building materials are in for some fun but given the housing bubble there is a risk of a swift reversal. Same for retail. Of all of them, only Crown looks good, on the dollar play.

As I wrote late last year, the sell side was always going to get excited by cyclicals this year, and that carries its own market implications, but it is far from clear cut that cyclicals in general will actually deliver.