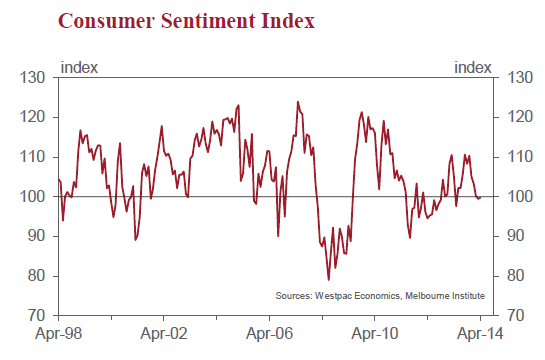

• The Westpac Melbourne Institute Index of Consumer Sentiment increased by 0.3% in April from 99.5 in March to 99.7 in April…

This flat result is a mild surprise. Given that the Index has fallen by a total of 9.6% since November and that March’s reading appeared to have been impacted by announced job cuts at Qantas and across the vehicle industry we had expected that some rebound was likely. That expectation was also supported by the recent positive news around the sharp rise in new jobs for February and ongoing positive news on the housing market.

While the Reserve Bank did not lower rates further at its April meeting there was minimal speculation around a move and therefore Reserve Bank policy is likely to have been a neutral for this month. In fact the confidence of those folks with a mortgage fell by just 0.7%.

There has also been notably less speculation in the media around the upcoming Budget.

While the overall Index hardly moved, the components were quite volatile. Assessments of family finances showed marked improvement with the sub-indexes tracking views on finances vs a year ago up 6.7%, and expectations over the next 12 months up 2.2%. On the other hand respondents were quite ambivalent around the economic outlook. The sub-index tracking expectations for ‘economic conditions over the next 12 months’ surged by 10.5% but the sub-index tracking the longer term outlook (over the next 5 years) was down by 4.2%. Surprisingly, given the recent improved trend in consumer spending, the subindex tracking views on ‘whether now is a good time to buy a major household item’ slumped by 8.7% to its lowest level since May 2012.

The Westpac Melbourne Institute Index of Unemployment Expectations fell by 3.2% from 164.4 to 159.1. Respondents were marginally less negative on the labour market. Note that a fall in this index means fewer consumers expect unemployment to rise in the year ahead. Despite the April decline, the Index is still 2.1% above its print for February, before respondents were unnerved by the announcements of large job losses in high profile companies Qantas and Toyota. This is still the second highest read since June 2009. This Index is still pointing to further deterioration in the labour market.

Prospects for the housing market also deteriorated. The index tracking views on ‘time to buy a dwelling’ fell by a further 3.9% to now be down by 20% from the recent peak in September last year. This fall has been particularly acute in Victoria where the peak to trough slump has been 39% including a particularly sharp 19% fall in April.

The Reserve Bank Board next meets on May 6, one week before the Federal Budget is announced. The Governor has indicated in recent statements that a period of rate stability is likely. Today’s Consumer Sentiment report supports that policy approach. It indicates that neither the labour market nor the housing market require rates to rise. On the other hand, stability in the Index at around the level where optimists and pessimists are in equal

numbers points to a ‘neutral’ consumer mood that supports a steady approach to monetary policy. Indeed Westpac does not expect that it will be necessary to raise rates before the second half of 2015.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.