This is from late Friday but is worth repeating. From Bloomie:

Chinese developers raised 49 percent less through trusts in the first quarter as the collapse of Zhejiang Xingrun Real Estate Co. highlighted default risks.

Issuance of property-related trusts, which target wealthy investors, slid to 50.7 billionyuan ($8.16 billion) from 99.7 billion yuan in the fourth quarter, data compiled by Use Trust show. The yield on AA rated five-year bonds has climbed 175 basis points in the past year to 7.23 percent, according to Chinabond. That compares with 2.74 percent on corporate securities globally, Bank of America Merrill Lynch indexes show.

“The banking system and the shadow banking system are becoming concerned about exposure,” David Cui, China strategist at Bank of America said in an interview yesterday. “Once people refuse to provide credit to developers, their balance sheets will be under pressure, forcing them to cut prices. Once enough of them cut prices, fewer people would buy because most people buy property only when they think the price is going up. If this persists, it will turn into a vicious loop.”

…“While the government is trying to curb shadow banking and investors are worried about credit risks of property companies, shadow-banking credit to the property sector will continue to shrink,” said Li Ning, a bond analyst in Shanghai at Haitong Securities Co., the nation’s second-biggest brokerage. “Property companies’ demand for capital is still strong even as borrowing costs rise.”

Mining and property trusts are among the products with the highest default risks, Li added.

Outstanding property trust products, including collective and single, totaled 1.03 trillion yuan as of the end of last year, accounting for 10 percent of all types of trusts, according to data posted on the website of China Trustee Association.

…Unless the government intervenes, both shadow banks and official lenders will provide less financial support to property companies, according to Bank of America’s Cui. At the moment, there is no strong sign that the central government will come out to support the real estate industry, he said.

“Both the economy and the financial system are relying too much on the property sector,” he said. “This is a systematic problem.”

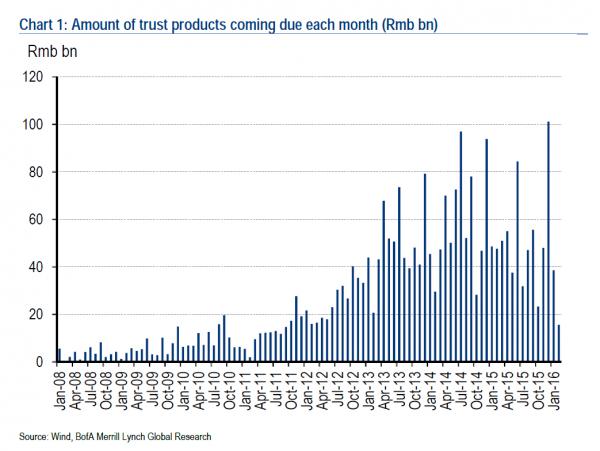

This is my number one global growth risk for this year and next year. Here is Cui’s pipeline of trust maturities: