If you want to know why New Zealand is the new star economy and Australia is yesterday’s news then the IMF does a good job of explaining it to you in its new World Economic Outlook with a study on China’s changing commodity demand.

Following three decades of rapid growth in China of about 10 percent a year on average, the recent slowdown has raised many concerns. Among them are the implications for global commodity markets: China’s demand rebalancing may lead to lower commodity consumption and prices and thus create adverse spillovers to commodity exporters (Figure 1.2.1). This box delves into China’s commodity consumption and its relationship to demand rebalancing. The analysis finds that China’s commodity consumption is unlikely to have peaked at current levels of income per capita. Moreover, the pattern of its commodity consumption closely follows the earlier paths of other rapidly growing Asian economies.1 However, recent shifts in the composition of China’s commodity consumption are consistent with nascent signs of demand rebalancing—private durable consumption has started to pick up, while infrastructure investment has slowed.

Global (and Chinese) commodity consumption has been rising and is predicted to continue to do so, but at a slower pace for low-grade commodities and an accelerating one for higher-grade commodities—implying positive spillovers for exporters of commodities, particularly of higher-value commodities.

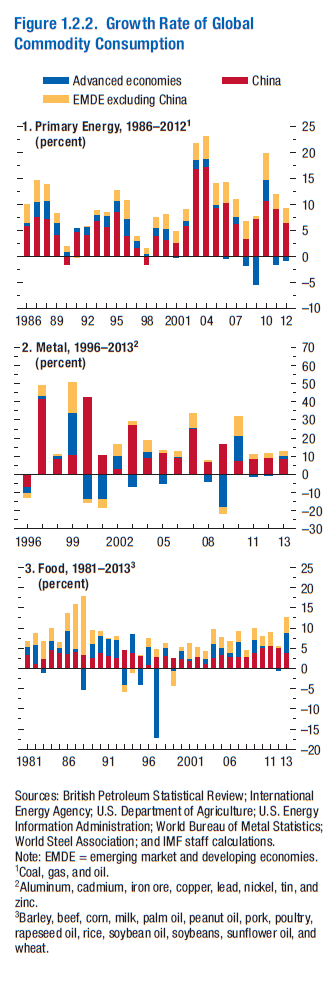

Growth in global commodity demand has moderated somewhat, but China’s commodity consumption is still rising. Since the global financial crisis, the growth rate of global commodity consumption appears to be slowing, relative to the boom in the middle of the 2000s, except in the case of food (Figure 1.2.2). This slowdown has been accompanied by a compositional shift in global commodity consumption. Specifically, within primary energy, the growth rate of natural gas consumption has risen faster than that of other fuels, very basic food staples such as rice are giving way to proteins (the sum of data for edible oils, meat, and soybeans; excludes seafood and dairy, for which data are incomplete), and base metal consumption has generally shifted away from low-grade metals (copper and iron ore) toward higher-grade ones (aluminum and zinc). In China, the growth rate of commodity consumption has also moderated, but is still robust. Within commodity categories, patterns in energy, metal, and food consumption per capita appear to be broadly in line with a few decades earlier. Some idiosyncrasies are evident; most notable are China’s considerably higher per capita consumption of coal and high-protein foods. However, recent shifts in composition commodity categories at the global level are also evident in China. In particular, rice has given way to higher-quality foods (edible oils and soybeans, and to a lesser extent, meat); copper and iron ore have recently been giving way to aluminum, tin, and zinc; and coal has started to give way to cleaner primary energy fuels. Chinese (and other emerging market) demand for thermal coal softened in 2013 and early 2014, consistent with the baseline forecast of the International Energy Agency (2013).

The relationship between commodity consumption and income can help gauge prospects for future commodity consumption

in China. The predicted relationship between commodity consumption per capita and income per capita and other determinants is based on cross-country panel regressions estimated over the period 1980–2013 with country fixed effects for 41 economies (26 advanced: Australia, Austria, Belgium, Canada, Czech Republic, Denmark, Estonia, Finland, France, Germany, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Netherlands, New Zealand, Norway, Slovak Republic, Slovenia, Spain, Sweden, United Kingdom, United States; and 15 emerging or developing: Chile, China, Croatia, Hungary, India, Iraq, Mexico, Malaysia, Pakistan, Poland, Russia, South Africa, Taiwan Province of China, United Arab Emirates, Vietnam).

For primary energy, the nonlinear relationship with per capita income predicted earlier (April 2011 World Economic Outlook) still holds. The estimated regression is eit = ai + P(yit) + uit, (1.2.1) in which i denotes the country, t denotes years, e is primary energy per capita, y is real per capita GDP, P(y) is a third-order polynomial, and fixed effects are captured by ai. Specifically, income elasticity of energy consumption is close to one at current levels of income per capita in China (as it was earlier in other fast-growing Asian economies). In contrast, advanced economies can sustain GDP growth with little if any increase in energy consumption (Figure 1.2.3, panel 1).

This relationship is flat for higher incomes—except in the United States, where consumption has been increasing with income per capita. What is new is the analysis for base metals. The estimated regressions for average metals and their components are the same as that for energy but with added arguments: the share of investment in GDP, the share of durables in private consumption, and the growth rates for both. In particular, the nonlinear relationship with per capita income is a good predictor of metal consumption at the early stages of income convergence, with an income elasticity greater than one in China (and its Asian comparators). The predicted metal consumption curve reaches an inflection point at a much earlier income threshold relative to energy, first slowing at the threshold of $8,000 per capita, then reaching a plateau at about $18,000 per capita, and thereafter falling gradually (Figure 1.2.3, panel 2). Moreover, predicted consumption is rising in the growth rate of the investment-to-GDP ratio (unlike for primary energy).

Since the growth rate of investment appears to be slowing and consumption is beginning to rise in China, a further disaggregation of base metal consumption could be warranted to assess which metals are more sensitive to these recent developments in investment and consumption. For a few high-grade metals, such as aluminum and zinc, the relationship is found also to be rising significantly in both the share of durable consumption in private consumption and its growth rate, with the consumption elasticity significantly larger than one (and larger than that for the average metal). Hence, the predicted consumption per capita of high-grade metals grows briskly at levels of income per capita below about $20,000 (relative to the growth rate and the plateau predicted for average metals). However, it falls more rapidly thereafter (relative to average metals) (Figure 1.2.3, panel 3). This result implies that investment, durables, and GDP growth more broadly will come with higher consumption (with an increasing growth rate) of these metals in the future—this is likely also to hold true for some precious metals used in high-end durable manufacturing, such as palladium—at least until China’s income per capita is double the current level. This is not the case for low-grade metals, for which investment and GDP growth will soon be sustained with lower consumption growth rates for these metals, implying a slowing in future demand growth. Estimation results confirm that copper and iron ore consumption will continue to rise, but at a slowing rate as income rises, similar to the experiences of China’s Asian benchmarks earlier. At incomes of $15,000 per capita and higher, consumption of copper and iron ore is predicted to fall more rapidly than consumption of aluminum. Among base metals, only copper futures are in backwardation. What are the broader implications of this analysis, however, for global commodity demand, and what are the links to China’s demand rebalancing?

The predicted paths for metal consumption per capita are consistent with slowing investment in infrastructure and accelerating consumption of durables in China. Relative to that in other emerging market economies, China’s commodity consumption per capita is indeed high and rising, as established. However, this is not unusual for its early stage of income convergence given its growth model, which broadly follows that of Korea and Taiwan Province of China in the 1970s and 1980s and of Japan some decades earlier. These benchmark economies relied on a growth model led by exports, factor accumulation, low private consumption, and high investment (Figure 1.2.4, panels 1 and 2). Differences between China and these benchmark economies—studied in IMF (2011, 2013a); Hubbard, Hurley, and Sharma (2012); and Dollar (2013)—are largely related to somewhat higher investment-to-GDP and lower household-consumptionto- GDP ratios, linked to China-specific social and institutional factors. Private consumption in benchmark economies also initially declined and later grew as income began to converge, and their infrastructure investment slowed concomitantly. China’s high investment (Ahuja and Nabar, 2012; Roache, 2012) appears to be leveling off. This is particularly notable in the growth rate of infrastructure, as some provinces near a threshold of industrialization and infrastructure building (McKinsey Global Institute, 2013).

Thus, the observed slowing in metals used heavily in infrastructure seems natural. Meanwhile, private durables consumption is catching up following a long delay (Figure 1.2.4, panel 3), perhaps linked to the acceleration observed in the growth rate of consumption of aluminum and other high-grade metals (Deutsche Bank, 2013; Goldman Sachs, 2013a).Demand rebalancing should follow. Regression results suggest that the growth rate of GDP and the investment-to-GDP ratio drive private consumption at the early stages of income convergence (before the $10,000 per capita threshold), when low-grade commodities are intensively consumed. Thereafter, invoking Eichengreen, Park, and Shin (2013), (higher) levels of income and other domestic social and institutional factors largely drive the share of durable consumption (and services) when demand shifts toward high-grade commodities. Such predictions of the determinants of domestic demand components appear to be consistent with the shifting commodity composition and spending pattern observed in China: toward high-grade commodities and durables since 2012 and softening demand for low-grade commodities and slower infrastructure investment during 2013, thus suggestive of nascent demand rebalancing. Implementation of the envisaged reforms outlined in the Third Plenum of the 18th Central Committee, particularly the removal of factor subsidies and administered credit, should lift private labor income and foster further rebalancing.

Positive spillovers to both low- and high-grade commodity exporters should occur as commodity consumption follows predicted relationships. Rebalancing does not indicate that the level of China’s consumption of commodities will peak—at least not until the country’s per capita income doubles from current levels. Rather, commodity consumption (globally and for China) is predicted to increase and to continue to shift gradually toward high-grade foods and metals as well as cleaner primary energy fuels.

However, exporters of basic and low-grade commodities (such as rice, copper, iron ore, and later, coal) should expect Chinese demand to grow more slowly as it shifts toward other commodities, with increasing, positive spillovers to the exporters of these

commodities.

This an excellent text book description of the shift underway in China. I will only add that in the real world it doesn’t work quite so smoothly. Markets exaggerate underlying trends and cause overshoots and imbalances followed by even more dramatic corrections.

The case of China is unlikely to be any different which means that although the underlying story of the IMF is right, its timing could be off and, moreover, the rebalancing that it is describing might transpire in large steps over short periods via crisis.

The timing is impossible to predict but the probability of it happening is high so any long term investment should be acting upon the IMF’s Chinese narrative.

Full report here.