From the Kouk:

It would be a wild exaggeration to say that Australia has an inflation problem, but the March quarter CPI highlighted the fact that the strength of the domestic economy is spilling over into a somewhat uncomfortable acceleration in the inflation rate.

While the March quarter inflation rates came in under market expectations (which says more about those expectations than it does about the actual hard data), inflation is moving higher.

Whether it is the annual headline inflation rate – which has risen from a low of 1.2 per cent in the June quarter 2012 to 2.9 per cent now – or the underlying inflation rate – which has risen from a low of 1.9 per cent to 2.7 per cent now – the RBA can no longer sit on a record low cash rate of 2.5 per cent and be confident that a further acceleration in the inflation rate wont happen.

Left unchecked, there is more chance the inflation rate will exceed 3.5 per cent than it will drop below 2.5 per cent in the year ahead. This suggests the RBA is playing a very dangerous game in its refusal to contemplate even a moderate winding back of the current monetary policy stimulus that has been in place for a year.

What could be worrisome about the recent upward momentum in the inflation rate is that it has occurred with wages growth near historical allows. This means we are not seeing cost-push inflation (the old wage/inflation ‘spiral’) but demand-pull inflation, which results from demand running ahead of capacity.

One only needs to look at the strong growth in retail spending, the record high level of new house building and the massive $1 trillion boost to wealth over the last two years from rising house and stock market prices to see why firms are able to get away with price increases to eager consumers.

While it is early days with the turn in labour market conditions, any upshift in wages growth would, according to RBA orthodoxy, only add to inflation pressures.

With the economy showing no sign of losing momentum, it seems obvious that interest rates need to move towards a neutral rate around 3.5 per cent. The RBA should still be taking out the proverbial insurance against an inflation breakout later this year and into 2015 by hiking the cash rate by 25 basis points rates very soon as it starts along the path back to, say, 3.5 per cent for the cash rate.

The fall-away in mining investment is being swamped by stronger growth elsewhere. The transition is occurring and the threat to economic growth from a tight budget seems very low risk given the countervailing boost to government spending on infrastructure, paid parental leave, defence and a raft of other Coalition favourites.

The next RBA Board meeting is 13 days away. The RBA should be hiking interest rates but its body language now makes that unlikely. Inflation is getting uncomfortable, the RBA knows it, but obviously wants to see the inflation pressure build further before acting.

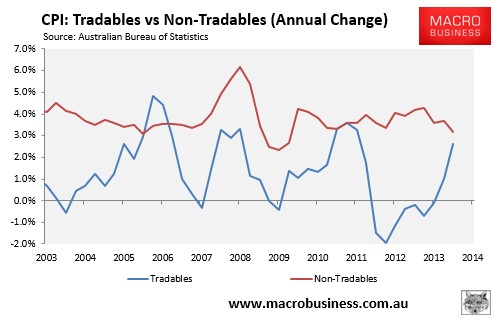

Demand pull inflation? Domestic demand has been in near recession for the better part of a year. The recent rebound is muted and is why non-tradable inflation is weakening. This inflation episode is all about tradable inflation from a falling dollar:

The August CPI report will see a lowly 0.4% reading from last year drop out of the series so there’s some chance that the Kouk’s maniacal hawkishness will get a second wind in the second half. But by then the capex cliff will be shedding feathers like a mauled bullhawk and its so-called “swamping” by stronger growth elsewhere will probably have receded. If the dollar stays where it is then tradable inflation will also stabilise soon enough.

I guess this is the Kouk’s way of saying he’s wrong again on rate hikes.

Meanwhile, Bloxo offers the more sober hawkish assessment:

CPI inflation surprised the market on the downside in Q1, with trimmed mean inflation steady in y-o-y terms at +2.6%. Headline inflation ran at +2.9% (market had +3.2%). Imported goods inflation has picked up over the past year, with annual tradable inflation running at +2.6% y-o-y, largely driven by the fall in the AUD from its early 2013 highs. This lift was, however, offset by some moderation in domestic cost pressures, as a loose labour market and slowing wages growth have kept non-tradable inflation contained. Non-tradable inflation ran at +3.1% y-o-y in Q1.

Today’s figures are likely to have been weaker than the RBA was expecting. In its last set of published forecasts the central bank was projecting underlying inflation to rise in H1 2014, reaching +3.0% y-o-y by Q2. However, despite today’s weaker than expected outturn, underlying inflation remains in the upper half of the central bank’s target band in y-o-y terms.

With growth rebalancing, domestic demand lifting, the labour market improving and inflation passed its trough, we still see the RBA’s easing phase as likely to be done. Given these factors we also expect that the RBA is unlikely to resume its ‘jawboning’ campaign to talk the AUD lower. Overall, today’s result is likely to leave them comfortable with current policy settings for now.

Looking ahead, the RBA have stated in recent commentary that ‘the cash rate could remain at its current level for some time if the economy was to evolve broadly as expected’, predicated on a view that inflation would fall in H2 2014 and in early 2015, as the loosening labour market reduced wages pressures. However, more recent data have challenged these assumptions with the unemployment rate having fallen from its recent peak and forward indicators, such as job advertisements and business surveys, pointing to a further pick up in hiring in coming months. If the labour market continues to improve, as we expect it may, disinflation from this source may turn out to be less pronounced than the RBA expected and rates may need to rise earlier than the market is currently pricing.

Inflation surprised the market to the downside in Q1, as a loose labour market and slow wages growth kept cost pressures contained.

Today’s outturn is likely to be weaker than the RBA were expecting and should see the central bank remain comfortable with current policy settings for now.

However, with the economy continuing to strengthen and the labour market beginning to improve we continue to see the next move in rates as likely to be up and expect that a hike may arrive before the end of the year.

Also likely wrong but at least on the right planet.