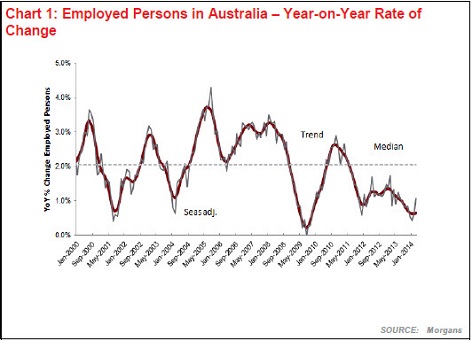

Australia is at the very beginning of a recovery from an extended growth recession. A growth recession occurs when growth in employment is slower than growth in the labour force. The average growth rate of employment in Australia since the beginning of this century is 2.05% per annum. As you can see in the chart below, employment in the past two years has only been a fraction of this:

Two employment measures published by the Australian Bureau of Statistics are the seasonally adjusted measure and the trend measure. The seasonally adjusted measure seems to be favoured by the media, but it’s the trend measure that proves to be more reliable.

The trend measure of year-on-year employment growth was well below average back in July 2012. For the year to July 2012 employment by this measure grew by only 1.2%. A year later in July 2013, it was even lower at 1.03%. The low in this series of year-on-year growth rate in employment was not reached until February 2014, where employment grew only 0.64% for the year to date. Inevitably this led to unemployment sneaking up.

In February unemployment was 5.9% on the trend measure and 6.1% on the seasonally adjusted measure. In March, unemployment fell on a seasonally adjusted basis from 6.1% to 5.8%. This was reported as the beginning of a rapid recovery – it is not. The improvement in the more reliable trend measure was minuscule. Trend employment growth rose from 0.64% for year to February to 0.66% for the year to March.

Looking up from here

We do think this is the bottom for employment, but the recovery will take a long time to happen. We suspect the seasonally adjusted number for unemployment, having fallen too far in March, will rise again in April. In fact, employment growth has to be growing at faster than the long term average of 2.05% for unemployment to fall. We believe it will be the end of 2014 before employment again rises to the long term average level.

What this means for interest rates

Many commentators have suggested that the improvement in the employment picture we have just seen suggests that interest rates will soon be going up. We think that is entirely premature. It is difficult to believe that the RBA will put up interest rates in the circumstances of rising unemployment.

Our view remains that there will be no increase in Australian interest rates before the final quarter of 2015.

I recently gave Mr Knox a caning for a poor report on iron ore but this is a better read on the Australian economy. As a base case I’d take this seriously and would only add that the prospects for recovery so slow enough that we are just as likely to see another external shock before we get there meaning interest rates could very easily go lower before they go higher.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.