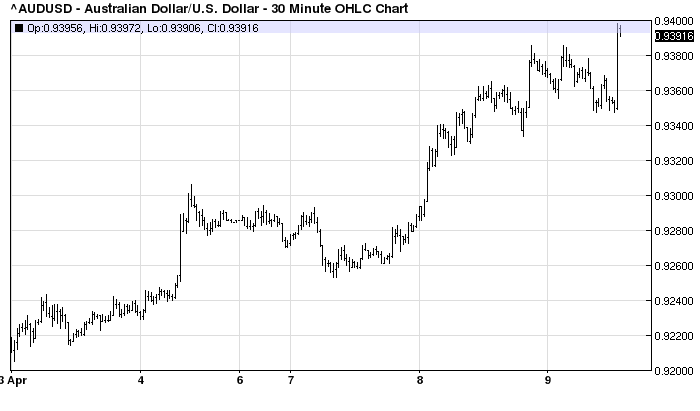

The rampant Australian dollar took out 94 cents (well, 93.97!) last night as the Fed minutes hosed the hawks:

In their discussion of monetary policy going forward, participants focused primarily on possible changes to the Committee’s forward guidance for the federal funds rate. Almost all participants agreed that it was appropriate at this meeting to update the forward guidance, in part because the unemployment rate was seen as likely to fall below its 6-1/2 percent threshold value before long. Most participants preferred replacing the numerical thresholds with a qualitative description of the factors that would influence the Committee’s decision to begin raising the federal funds rate. One participant, however, favored retaining the existing threshold language on the grounds that removing it before the unemployment rate reached 6-1/2 percent could be misinterpreted as a signal that the path of policy going forward would be less accommodative. Another participant favored introducing new quantitative thresholds of 5-1/2 percent for the unemployment rate and 2-1/4 percent for projected inflation. A few participants proposed adding new language in which the Committee would indicate its willingness to keep rates low if projected inflation remained persistently below the Committee’s 2 percent longer-run objective; these participants suggested that the inclusion of this quantitative element in the forward guidance would demonstrate the Committee’s commitment to defend its inflation objective from below as well as from above. Other participants, however, judged that it was already well understood that the Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance.

Most participants therefore did not favor adding new quantitative language, preferring to shift to qualitative language that would describe the Committee’s likely reaction to the state of the economy.Most participants also believed that, as part of the process of clarifying the Committee’s future policy intentions, it would be appropriate at this time for the Committee to provide additional guidance in its postmeeting statement regarding the likely behavior of the federal funds rate after its first increase. For example, the statement could indicate that the Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run. Participants observed that a number of factors were likely to have contributed to a persistent decline in the level of interest rates consistent with attaining and maintaining the Committee’s objectives. In particular, participants cited higher precautionary savings by U.S. households following the financial crisis, higher global levels of savings, demographic changes, slower growth in potential output, and continued restraint on the availability of credit. A few participants suggested that new language along these lines could instead be introduced when the first increase in the federal funds rate had drawn closer or after the Committee had further discussed the reasons for anticipating a relatively low federal funds rate during the period of policy firming. A number of participants noted the overall upward shift since December in participants’ projections of the federal funds rate included in the March SEP, with some expressing concern that this component of the SEP could be misconstrued as indicating a move by the Committee to a less accommodative reaction function. However, several participants noted that the increase in the median projection overstated the shift in the projections. In addition, a number of participants observed that an upward shift was arguably warranted by the improvement in participants’ outlooks for the labor market since December and therefore need not be viewed as signifying a less accommodative reaction function. Most participants favored providing an explicit indication in the statement that the new forward guidance, taken as a whole, did not imply a change in the Committee’s policy intentions, on the grounds that such an indication could help forestall misinterpretation of the new forward guidance.

Looks like our Janet got tongue-tied, indicating precisely the opposite at her post meeting press conference.

Meanwhile, in better news, Goldman is bulling-up on the Spring rebound:

Advertisement

US economic growth is accelerating as the economy bounces back from the inventory and weather-related weakness of the first quarter. Our current activity indicator (CAI) is up a preliminary 3.6% in March, well above the 2% pace of the prior three months and consistent with our forecast for a rebound into the 3%-3.5% range for real GDP growth in the remainder of 2014.

…the labor force participation rate has risen by 0.39 percentage points since December, the biggest increase over a three-month period since 2007. The main reason for the increase has been a significant pickup in the gross flow of individuals from inactivity to employment (and to a lesser degree unemployment). We view this as a potentially promising sign that labor demand is picking up sufficiently to pull discouraged workers back into the labor force.

The increase in labor force participation is especially encouraging because the expiration of emergency unemployment benefits at the end of December should have acted to reduce participation. We have received questions whether the impact might have gone the other way. Some argue that the loss of benefits might have forced some workers to seek employment, and that this could have increased participation. But this assumes that prior to year-end there were a significant number of individuals who told the unemployment benefit office that they were actively seeking work but said the opposite in the household survey. We find this hard to believe; most people would probably be reluctant to tell “the government” that they are not actually seeking work when doing so is a prerequisite for drawing benefits.

Tapering to roll on but not fast enough for Australia.

Advertisement

The budget forecast 91 cents and will now come under greater strain as nominal growth begins to slide.

Non-mining tradable businesses will be reassured that their offshoring strategies are right and local capex will fall harder than it is already in manufacturing, retail and wholesale. Mining capex will as well because the internal wage deflation that has begun will be wiped out – and some – for LNG, coal and iron ore.

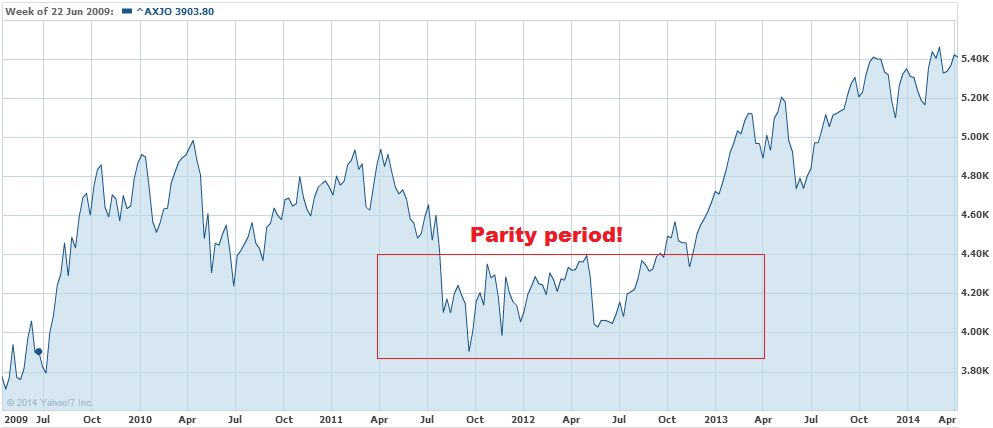

As thoughts of a return to parity begin to filter through the collective forex consciousness, the stock market rally will struggle too (yes, I’m aware that it will hit a post-GFC high today):

Advertisement

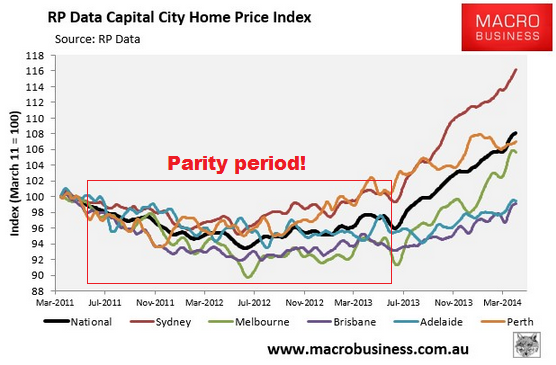

It’s a reasonable proposition to suggest that foreign investment into housing slow too. Prices didn’t take off until the dollar fell well below parity (in fact, more like 95 cents). That’s when the Chinese investor phenomenon hit the press:

Advertisement

Before you all get too excited, I’m not suggesting that these are scientific correlations. They’re educated guesses, having observed every data release, every day for the past four years, as well as tracking all media. It makes fundamental sense. As the dollar rises further above fair value so too do the risks of currency-related capital losses for foreign holders of Australian assets.

And this slowing is going to transpire as we head off the mining capex cliff in the second half, the terms of trade fall to new lows, and China slows anew. The RBA’s so-called rebalancing is in jeopardy.

The good news is that this is a fantastic last call for Australians to pile into assets with non-mining international exposure!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.