If you ask the AFR how far the US bull market has to run, you’ll get a simple answer:

‘‘The question, of course, is, ‘How much longer can this go on?’‘ Fidelity global strategies fund portfolio manager Jurrien Timmer said.

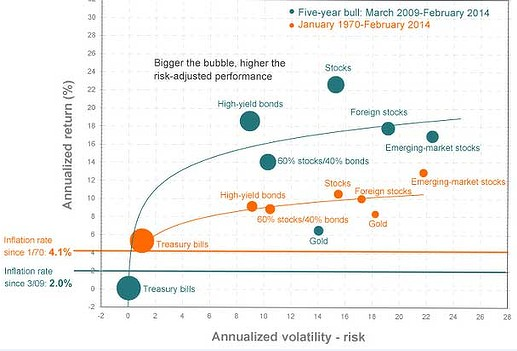

‘‘The good news is that the odds that the US economy will go into recession in any given year have gone from one in two before the Great Depression to one in four during the 1960s, 1970s, and 1980s, to one in seven since then. This suggests that even after a five-year recovery, we are, statistically, at least, not yet due for a recession or bear market.’’

Holy cow, that’s weak. Anything better?

‘‘If the US stock market has indeed entered a secular bull market, the outsized 23 per cent annual return since the 2009 low could actually be par for the course for years to come,’’ Mr Timmer said.

‘‘Secular bull markets have on average lasted 21 years. That suggests that the last five years could be only the beginning.’’

That quote is going straight to the pool room. Still, there’s a little disquiet:

Advertisement

‘‘I still wonder whether there will be unintended consequences from QE. I find it hard to imagine that the Fed can add $4 trillion to its balance sheet without there being some sort of price to pay for it.’’

I’ve been bullish the S&P for 18 months and remain so but it has absolutely nothing to with fundamentals. Rather, it has everything to do with this. From the adorable crazies at Zero Hedge:

Advertisement

The worse things get the better the returns!

Meanwhile there’s Australian equities strategy from the Tim Baker at the SMHblog:

The premium ascribed to cyclical stocks is justified by their “superior growth outlook,” reckons Deutsche’s equity strategist, Tim Baker, while “the recent weakness in resources looks like a buying opportunity”.

Baker says he likes miners over banks, because “Australia is having a construction cycle without a leverage cycle (different to history), which leaves banks with only moderate earnings growth. And valuations look very full on those earnings.”

In terms of cyclical industrials:

Prefer domestic to offshore exposure as the non-resources economy improves.

Consumer spending seems to be picking up.

They’re “less worried about the labour market – while resource employment will slow, there should be jobs growth coming from housing and eventually business capex recovery”.

Financial markets plays “look attractive, with good valuations and solid inflows on the back of households’ rising risk appetite”.

Deutsche Bank has added Harvey Norman, Nine Entertainment, Ansell, Aurizon, AMP and NAB to their model portfolio, and removed Myer, Downer, Aristocrat Leisure, Perpetual, Primary and CBA.

It’s fair analysis but I disagree for the simple reason that the mining bet is really a punt on iron ore and that is an all or nothing gamble of an opaque clique of Chinese communists. The local cyclicals are fair enough but I can’t see the economy accelerating without a lower dollar so my view is unchanged: international industrials are the growth pick for the cycle.

Advertisement

As for when the cycle ends, in my view we are currently somewhere in early to mid 2007.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.