It’s a mad cacophony of hooves and beaks and screeched revenge today! Head bullhawk, The Kouk, is thundering overhead:

It was always going to happen – the pace of economic growth was certainly strong enough to be generating jobs – it was just the lag between a stronger economy and more jobs that was in question.

So news of a nice jump of 47,300 in employment in February and a flat unemployment rate is certainly good news and it is starting to bring the labour force data into line with the rapid economic expansion now underway in the broader economy.

With house building at record highs, consumer spending returning to above trend growth and export growth running at a strong double digit pace, many more jobs will be created in the year ahead. Indeed, it would be reasonable to expect around 200,000 jobs to be created in the next 12 months, even if the monthly profile to get there is extremely volatile.

When the lift in non-mining investment is also taken into account, there appear to be very few downside risks to Australian growth in the year ahead, even allowing for a possible tight budget in May.

Another quarter or two where GDP growth runs at a 3 per cent plus growth pace, which is likely given the hard data of recent times, would signal not only stronger demand for labour, but would suggest that some of the building inflation pressures over the past half year would also be magnified.

This is where the RBA is playing a dangerous game in refusing to move monetary policy towards neutral – ie, starting the process of hiking the cash rate to ensure its inflation target is not blown out of the water. A 25 basis point rate hike now, followed by another in a few months, for example, would hardly derail the growth momentum in the economy.

But a rate hike would certainly signal the RBA’s seriousness in meeting its inflation target and would give it a bit of wriggle room in either a scenario of very strong growth (thankfully we acted early) or an economic decline (let’s take back those hikes and no damage done).

Add to that rampaging house prices – prices are up 1.5 per cent in the first two weeks of March and are now 2.7 per cent up for 2014, year to date – and the impediments to the RBA hiking interest rates are scarce.

On the contrary, a clear turn in the labour market, as evident in today’s data, suggest the RBA will get smart and will start a rate hiking cycle in the next few months.

Fellow feathered bovine, Paul Bloxham rattled his bell, though with considerably greater sobriety:

Australia’s labour market improved in February, after a run of weak labour market outturns in recent months. Overall, the labour market remains loose – with the unemployment rate still at the highest level since 2003 – but it does appear to be improving. With the economy still some distance from full employment, pressures on wage costs are likely to remain subdued in the near term and not yet present a concern for the RBA.

However, we expect the labour market to continue to improve in coming months. The domestic economy looks to have turned a corner from Q3 last year. The economy posted solid growth in Q4 and a broad range of domestic indicators point to a further rise in activity over the beginning of 2014. In our view, the labour market lags the broader cycle in demand and given usual lags we would expect the improvement in hiring to further gather pace in coming months.

This improvement is beginning to be seen in the forward indicators of labour demand. Business surveys suggest the pace of hiring should continue to rise in the near-term, while job advertisement surveys point to a decline in the unemployment rate.

The labour market is likely to be a key factor determining the timing of future rate increases from the RBA. Typically, the RBA has only raised interest rates while the unemployment rate is falling. Their current view is that the unemployment rate will continue to rise through 2014. Given the usual lags between domestic activity and the labour market, we expect the unemployment rate could begin to decline in a meaningful way by the middle of this year – a factor potentially paving the way for rate hikes before the end of 2014.

From Crikey comes galloping support for the Pascometer:

Joe the Confidence Killer, they could call him. Hockey the Hatchet man of Hope, the Slayer of Sentiment.

The Westpac-Melbourne Institute Consumer Sentiment Index fell again between February and March, the Institute revealed, and is now down to 99.5 after reaching a high of 110 in November. “The proportion of pessimists now exceeds that of optimists for the first time since May last year,” the Institute darkly reported. Fairfax columnist Michael Pascoe correctly pinged Treasurer Hockey’s gloom, doom, we’ll-all-be-rooned rhetoric for the slump. Hockey’s garment-rending about the state of the economy continued well past his ascension to the treasurership. It continued through his first visit to Washington DC (which yielded dramatic predictions of bad times coming, and a $9 billion handout to the Reserve Bank to help fight them), December’s MYEFO statement, in which he used low-ball nominal GDP numbers to complain about the huge debt Labor had left him, and into the New Year, when he promised a slash-and-burn budget.

But in particular, as Pascoe spotted, consumer sentiment was also affected by partisanship: Labor voters see nothing but economic bleakness compared to Coalition voters — the gap this month is 84.5 for the former to 115.4 for the latter, a dramatic reversal from this time last year when Labor voters led Coalition voters on confidence by 25 points.

As I noted yesterday, and Crikey underlines itself, this happens every election so the Pascometer’s analysis (and Crikey’s) is still weak.

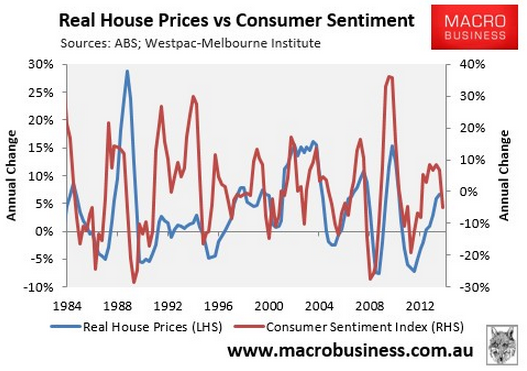

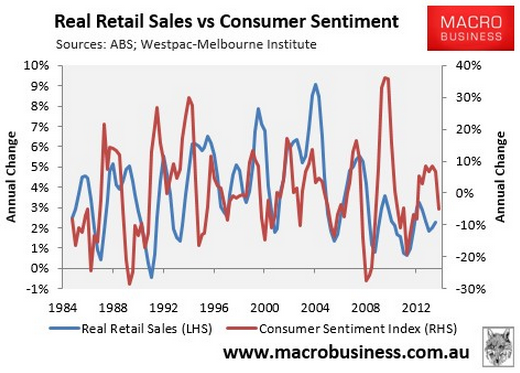

They go on to argue that there is no relationship between confidence and spending anyway so the recent falls in sentiment are irrelevant. Judge for yourselves the wisdom of that in the data:

My view remains unaltered. Yes, the first half will show some improvement in the labour market, but no, it won’t accelerate as the year rolls on and the capex cliff, as well as falling terms of trade, holds us back. The one thing that might change that is renewed Chinese stimulus but even then the likelihood is no rate hikes this year, and probably not next year, either.

On the other hand, macroprudential controls are inevitable!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.