From UBS, here’s what they reckons happens to major miners if the iron ore price stays where it is:

Summary findings: BHP & RIO earnings -20% and -30% in 2014E at spot

Diversifieds: All else remaining equal, our BHP & RIO earnings estimates for CY 14 would be -20% and -30% (prev. -18% and -28%) respectively under a spot scenario. Nevertheless, RIO would trade on cheaper spot multiples at 11.9x CY 14E PE vs BHP at 14.0x CY 14E. Iron ore: The spot iron ore price is 15% below our CY 14 forecast, and implies a 24% downgrade to FMG’s FY 14E earnings (prev. -23%) and -60% to AGO (prev. -57%).

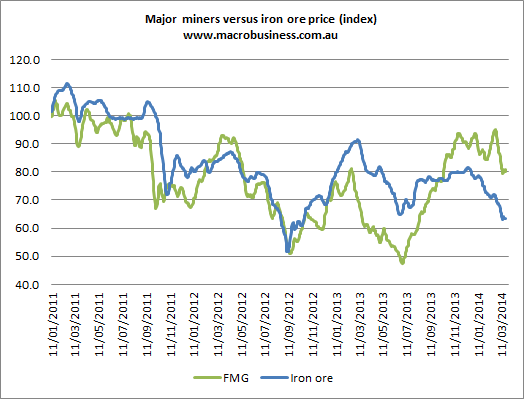

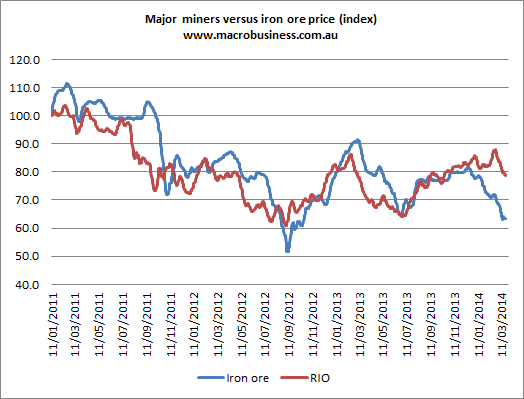

Crushed miners and budget. Yet, the equity market has discounted none of it:

Advertisement

Trading on faith in Chinese communists. Love it.