The ribald rally in the Australian dollar yesterday has come to abrupt end as markets woke up to crumbling Chinese data, a Crimean referendum and lousy US data.

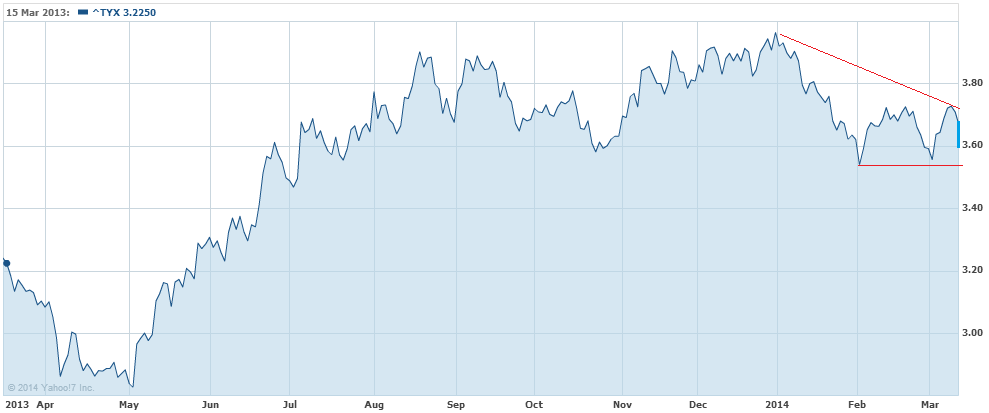

It’s not entirely clear what triggered what but the outcome was plain as day with stocks taking a 1.5% flogging and long bonds attracting a strong bid with yields down nearly 2%. The thirty year is now just 5 points above the 2014 3.55% low and is forming a bearish descending triangle pattern;

Advertisement

If it breaks, then the taper is likely too as well.

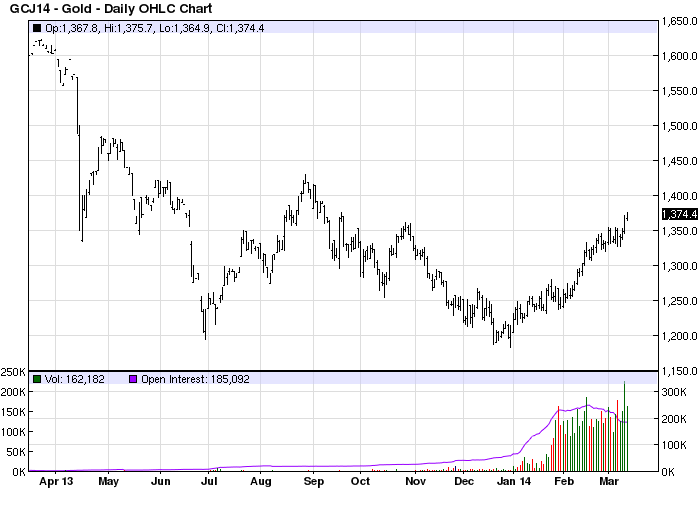

Supporting that contention, gold added a little to yesterday’s impressive gains:

Advertisement

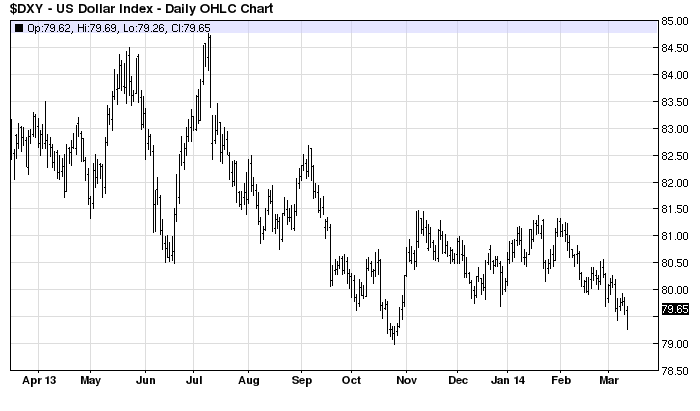

Again supportive, the US dollar also slumped (and recovered) but is clearly in a weakening trend:

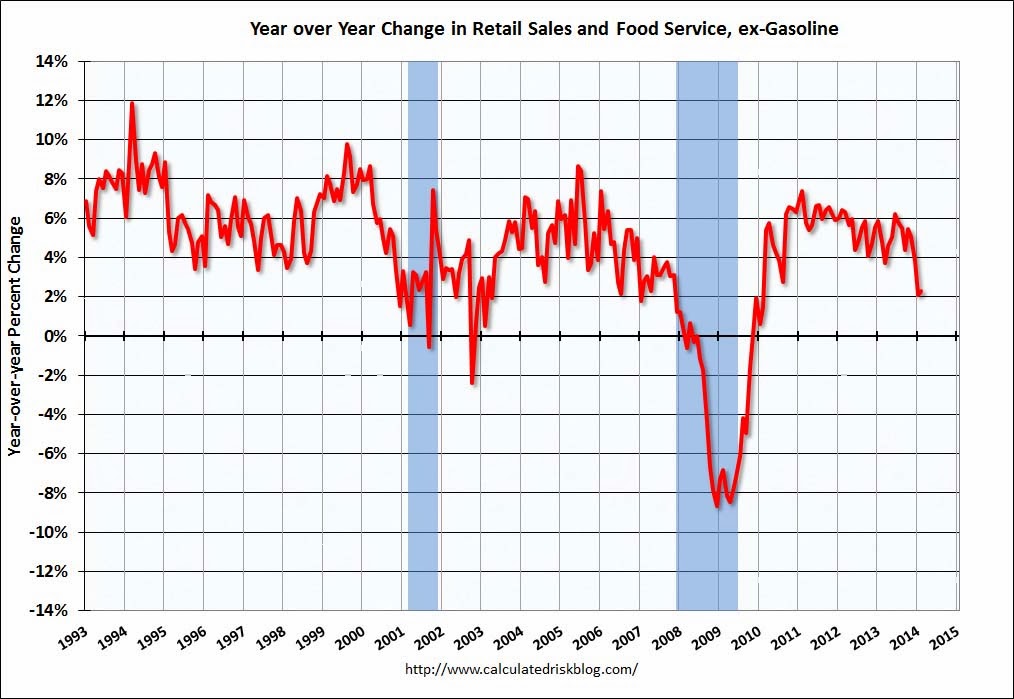

The US data flow was awful, reinforcing taper tapering. From Calculated Risk:

Advertisement

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for February, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $427.2 billion, an increase of 0.3 percent from the previous month, and 1.5 percent above February 2013. … The December 2013 to January 2014 percent change was revised from -0.4 percent to -0.6 percent.

That’s one chilly winter! Goldman can’t slash its first quarter growth forecasts quickly enough:

BOTTOM LINE: Although February retail sales rose a bit more than expected, negative back revisions more than offset the front-month surprise. Separately, initial and continuing jobless claims both fell more than expected. Import prices rose more than expected in February, but declined on a year-on-year basis. We reduced our Q1 GDP tracking estimate by two-tenths to 1.5%.

February retail sales rose 0.3% (vs. consensus +0.2%). Core retail sales?used by the Commerce Department to estimate the personal consumption expenditures (PCE) component of the GDP report?also rose 0.3% (vs. consensus +0.2%). By category, the strongest gains occurred in sporting goods (+2.5%) and non-store retailers (+1.2%), both bouncing back from weakness in January. (Non-store retailers mainly represent online shopping.) However, back-revisions to core retail sales in January (-0.3pp to -0.6%) and December (-0.2pp to +0.1%) were significant and widespread across categories, suggesting a trajectory of consumer spending in Q1 that was weaker than we anticipated.

We reduced our Q1 GDP tracking estimate by two-tenths to 1.5%.

Advertisement

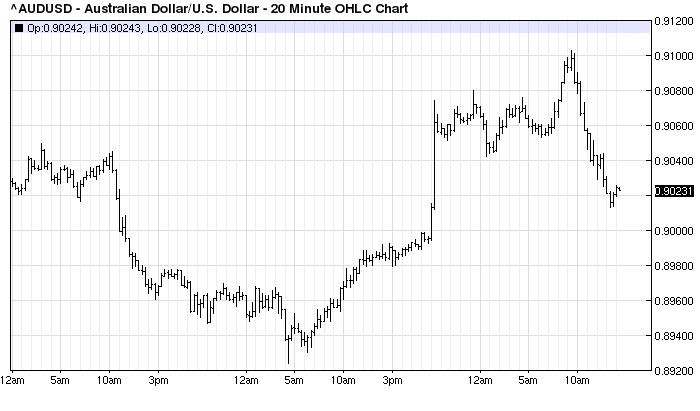

But! The Australian dollar wasn’t interested in any renewed QE:

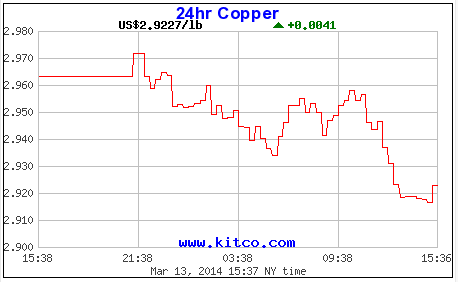

Nor was copper, which is consolidating its break below below the key $3 level:

Advertisement

Of course, stocks didn’t want a bar of more stimulus either so a mixed night for markets with weak US data out-weighed by weakening Chinese data, aborting the Aussie moon shot.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.