In late 2008, amid global housing busts and economic wreckage, the governor of the Reserve Bank of Australia (RBA), Glenn Stevens, said in a speech to Australian economists:

I don’t know anyone who predicted this course of events.

This should give us cause to reflect on how hard a job it is to make genuinely useful forecasts. What we have seen is truly a ‘tail’ outcome—the kind of outcome that the routine forecasting process never predicts.

Self-reflection is welcome and necessary in public officials. Good government is evolutionary. However, Stevens’ statement missed the point. While admitting a failure to foresee the crisis, he also delineated it as a one off, an eccentricity of history.

History tells a different story. Time and again, booms have emerged and given way to bust, panic and recession, or worse, in the real economy. An old wisdom in central banking used to acknowledge this in its practice of “taking away the punch bowl” when booms threatened excess.

As the 2008 comments of Glenn Stevens suggest, these days the RBA likes to kid itself that it is not an active force in these cycles. It pretends that the choices it makes about the price of credit are the output of some marble monetary vending machine, not run by humans, but by hard rules and constitution. If private sector adults are getting a little excited, well, that’s none of its business.

In the past it could hide behind this facade and confidently make statements such as the above. The political economy in which the RBA operated was thoroughly scrubbed of accountability. The media had the bank on a pedestal: because it wanted access, because it needed a foil for abysmal politicians, because the government protected it, because Australian business was (and is) a boys club and because it too had an interest in the perpetuation of Australia’s politico-housing complex.

There was even less accountability in the professional and academic economic community. Nobody criticised the RBA lest they lose access, lose a future job or lose their position of influence in boys club.

Thus through self-interest and peculiarity, the bank’s “independence” came to be seen as equal to unaccountable omnipotence.

These features of our political economy are still very strong. It is this that has enabled the RBA to duck inquiry, trial or punishment for the Securency corruption scandal that was of global dimension (can you imagine the different outcome if the same scandal took hold in the US or UK?). For those that care about such things, it is difficult enough holding to account a constitutionally independent body even without mutually assured dumbness.

But, there is not no accountability. Indeed, the RBA’s high marble wall of silence is being scaled and tunneled under. Driven by the internet, the shift is relatively new and still developing but it’s real and it means the days of untouchable RBA decision-making are over.

The past five years has witnessed the proliferation of a professional community of economic and monetary policy analysts that exist on the merits of their analysis. Whether it is MacroBusiness, MSM bloggers like Chris Joye at the AFR, Greg Jericho at The Guardian, or academic blogs like those of Steve Keen, Bill Mitchell, John Quiggin, Peter Johnson or Sinclair Davidson, even the proliferation of economic charts in stories everywhere, there’s a gathering assault on the boys club that holds up the RBA’s ersatz stone facade.

The result is that history is being changed. The once indomitable edifice of the RBA and its apologists can no longer fully determine its own narrative. When historians look back upon today, and examine the post-GFC period, they will find a multitude of high-caliber analysis and advice provided to the RBA from the many new and highly credible public quarters. Thus history will have a benchmark against which to measure the legacy of the key individuals currently within the bank. That is a form of accountability.

For instance, look at the case of Alan Greenspan in the US. Formerly known as The Maestro and worshiped by markets, insiders and the financial press while he occupied the role of FOMC chairman, in retirement he is a much diminished figure owing to history catching up to his poor decision-making of years before. The US’s own online community of iconoclastic analysts played no small part in his fall.

So, as our new business cycle begins to ripen, how will the historians of tomorrow judge the current RBA?

It’s post GFC period was one of excellence. It managed the disleveraging of households, the rebuilding of the Australian bank’s liability profiles and the largest mining boom in history without any explosion in the economy. Deft indeed.

But the virtual analytical community has been at odds with the choices of the bank in its management of the post-mining boom adjustment. Many of those above, as well titans of Australian economics – Warwick McKibbin, Bob Gregory, Peter Jonson and Ross Garnaut – have argued that a lower dollar and improved Australian competitiveness are the priorities, in order to trigger a renewed expansion in Australia’s tradable sectors.

Yet the RBA was slow to realise that the China boom had ended, slower still to grasp how quickly the investment boom would fall away and, instead of recognising that a global currency war was holding up the dollar and it needed new tools to fight it, it allowed the currency to remain hugely over-valued based upon an ideological notion of “free markets”.

Simple innovation could have brought the dollar down at any time. One easy step that the RBA might have taken in collaboration with APRA has been on display in New Zealand for two years in the use of macroprudential tools; regulatory measures that contain credit while lowering interest rates to bring down the currency. Other methods were mooted too – targeted money printing, Tobin taxes etc – all aimed at the same outcome.

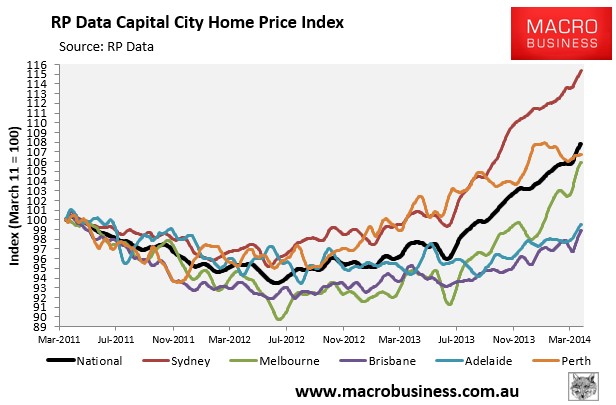

History will record that the people at the RBA very deliberately chose a different path. Perhaps guided by a complacency born of Australia’s post-GFC success, they chose to inflate house prices as their preferred macroeconomic stabiliser (thereby undoing their own previous good work):

Now, as the housing market runs headlong towards its highest ever valuation measured against incomes and GDP, the RBA is confronting a series of problems that it need not have created. The Australian dollar is charging higher and community disquiet about the influence of foreign investment is surging. It’s increasingly obvious to the economic community that house prices have themselves risen enough to become an imminent threat to financial and economic stability and a group of testosterone-juiced analysts is already calling for immediate interest rate hikes specifically to slow the market.

The last time the RBA did that was in 2003, without great negative consequences. But the economy of the time was very different. The terms of trade boom was just taking off and driving a golden era of income and taxation revenue growth. Rate hikes aimed at stalling house prices today will have very different consequences. An unhinged dollar will shoot to new highs, choking the tradeable economy as well as undermining the Budget. The green shoots of consumption will wither with falling income growth as the terms of trade and mining investment cliff steepen. A major recession that could have been avoided will threaten.

But if interest rates don’t rise, then the housing bubble will get bigger and our next external shock will be made far worse than it needed to be. That shock is not as far distant as short-memories might like to think. Global business cycles typically run for 7 or 8 years and we’re in our 6th of this one, with the Chinese rebalancing and US stock market bubble both extant threats.

The RBA elite would counter that they warned us all against speculation as they cut interest rates. And it’s true that the polity must take its share of the responsibility. But it’s still no excuse for the bank, which openly egged-on a house price boom to trigger new housing investment. Glenn Stevens was still doing the same two-step last week in Hong Kong.

The RBA elite has brought itself to a monetary impasse in which it is damned if it tightens and damned if it doesn’t and its legacy is at risk.