It appears MB has finally beaten some sense into Ross Gittins:

When people hear news reports about redundancies at this factory and that, many conclude we must be heading for recession. This time it ain’t that simple. After a record 21 years since the severe recession of the early 1990s, we’re overdue for another one and, with the economy quite weak at present, it wouldn’t be impossible for us to slide into recession this year.

But the explanation for the planned job losses we’re hearing so much about isn’t a downturn in the economy – it’s continuing change in the structure of the economy – the size of some industries relative to others. Much of the pressure for structural change is coming from advances in technology, particularly the digital revolution. It’s this that’s turning the newspaper industry inside out – no one seems to shed many tears over us – and is in the early stages of cutting a swath through retailing.

Good stuff there from the doyen of confidence economics. But Mr Gittins’ capitulation is also something of a trap, is it not? While other nations experience recessions ours (were it to happen) is only a structural adjustment and not, therefore, of concern, he reckons. That rather begs the question, is a structural recession better or worse than a cyclical one?

Gittin’s digital revolution is one small part of the larger picture of a lack of competitiveness. It’s not actually cause, it’s effect. All digitisation has done is bring extra sectors into the tradable universe, exposing them to cheaper jurisdictions. The structural change underway, then, is the process of sharpening our edge as cheaper and leaner nations cut our mustard across a broadening swath of industries.

Is that an easier process than Gittins’ implied opposite, the cyclical recession? The latter is an acute condition, a process of overheating leading to inflation and a rising cost of money that ultimately chokes the boom and brings on a bust. It’s tough, yes, but it also rebounds quickly, like 1991.

The structural recession is something different. It is more like the chronic malaise of the 1980s. It’s a condition that must grind expectations lower, force people into long-term jobs they don’t want and that are underpaid relative to the recent past. It’s a long term shift to lower living standards lest rising unemployment bring on the cyclical downturn as well.

There is no swift rebound. There is extend and pretend and an exhausting march to the bottom. Take your pick which one you prefer!

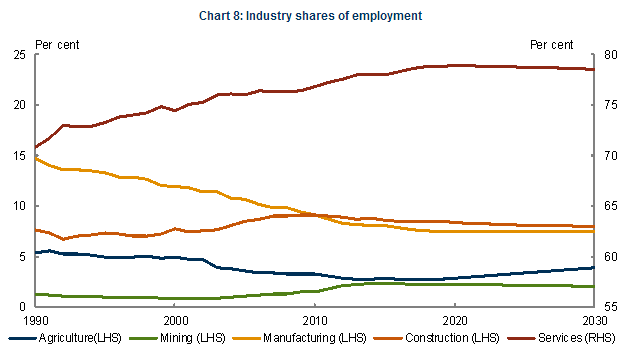

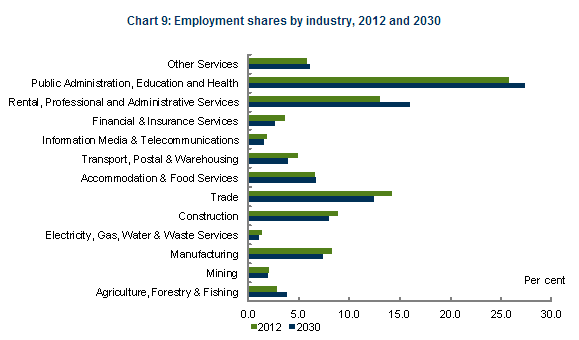

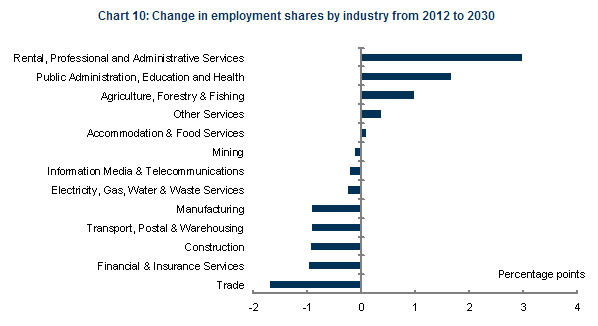

Anyways, Gittins concludes with remarks from David Gruen, head of Treasury’s Macro Group, a man who knows a thing or two about keeping his job during inclement weather, to examine where the job opportunities of the future will arise. Here are the crucial charts from Gruen’s speech:

If these baby-boomers and their macro settings remain in force, my guess is mining will be much lower. Manufacturing as well. Agriculture too will be weighed down by a failure to compete. That mix will mean even higher percentages for administration, health, professionals and much higher for bureaucrats. This is a vision of an aged and fattened economy with its arteries clogged by pencil-pushers. The sick man of the Pacific.

Is that better than a swift clean out and rebuild? I guess so but not by much!