It’s only a week since I check in on the Australian dollar “five drivers” valuation model but a lot has happened and many are probably wondering why the Australian dollar is not following iron ore into the abyss. The five drivers are:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth);

- investor sentiment and technicals; and

- the US dollar

For the first, my view remains that there is still very little chance of local interest rate hikes with falling terms of trade, the capex cliff and a soft labour market likely outweighing the bloom in activity in cyclical sectors. However, the run of decent cyclical data has firmed interest rate market conviction that that we’ll see rate rises in the year ahead. They are now pricing 13bps of hikes in the next twelve months and fell only 5 points today on the iron ore crash and NAB survey reversal from 18bps yesterday. That is still delusionally high and is the primary support for the currency.

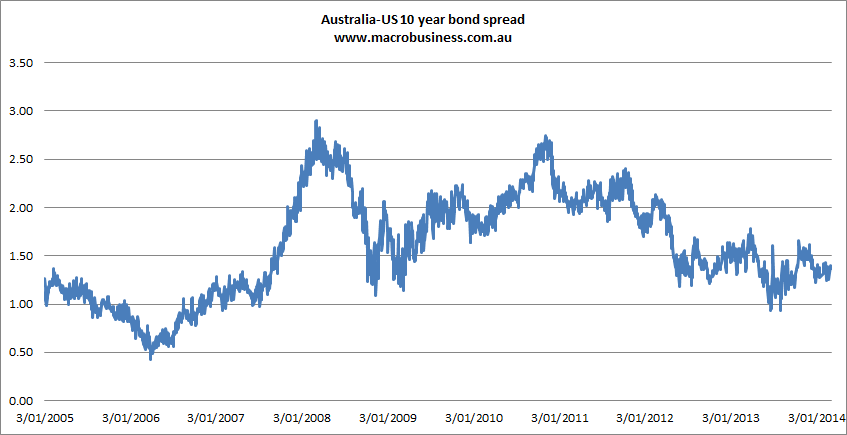

On the other hand, the rise in US bond yields that many expected this year has so far been cut short by a run of terrible economic data. Weather has largely been blamed and is responsible in some (possibly large) measure. That has meant that the carry spread between Australia and US ten year bond has risen a little but remains in its recent range:

The progress of taper at this point is anybody’s guess but assuming the weather is mostly to blame, the economy will snap back quickly and bond yields should rise some more.

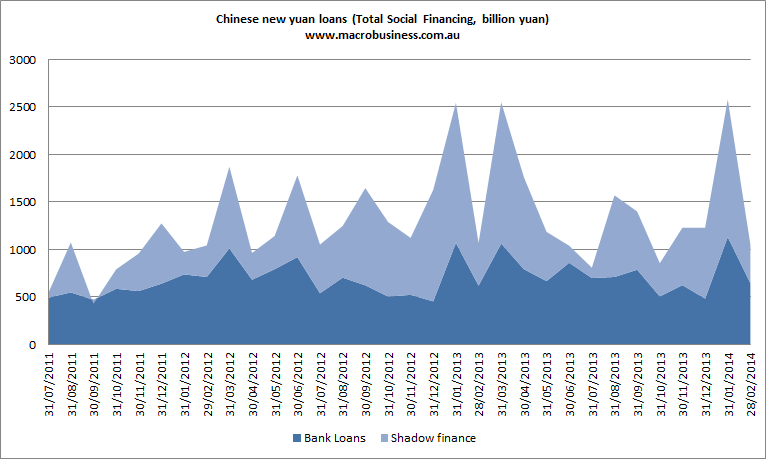

On driver two – global, local and Chinese growth – we face something of a dichotomy. Global growth may accelerate this year (maybe!) but Chinese growth is going to slow over the next six months to 7% and go lower if the rebalancing process is allowed to run its course. Following the economic planning meeting last week and pledge to cut fixed asset investment growth to 17.5% as well as maintain M2 growth rates at 13%, we’ve had poor trade and credit data:

There is also, of course, this:

Australian growth will follow suit. All things being equal, I expect another year of firmly sub-par growth, well under 3%, as the capex cliff, falling terms of trade and national income outweigh the cyclical forces of monetary and fiscal stimulus.

On the other hand, the US and global economies aught to chug along closer to 3% this year, above Australia.

Drivers three and four are less strong than last week:

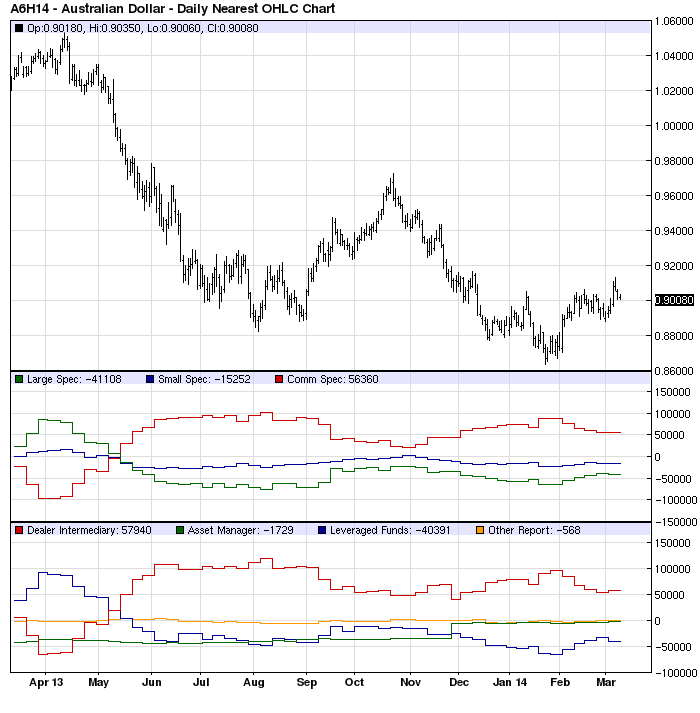

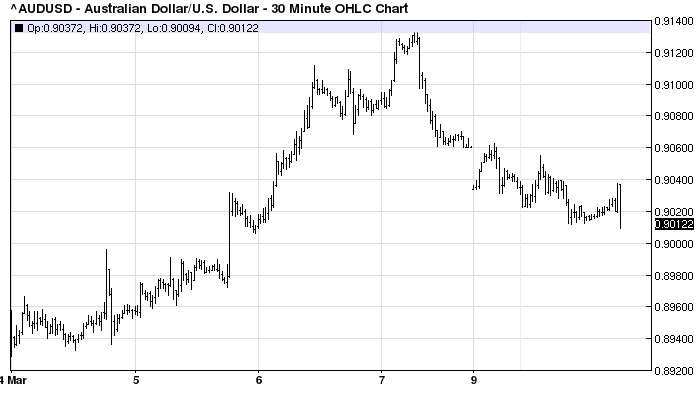

Daily technicals still show a possible inverted head and shoulders bottom forming but the break above 91 cents looks like a falsey. Here’s the daily chart:

Turning to sentiment, the Commitment of Traders report (above) is showing that the large and small speculators that control the market are still short with room to go much shorter. This could be either bullish or bearish but I’ll take the latter now. The RBA has also resumed a little jawboning in the past week and mooted the possibility of macroprudential tools.

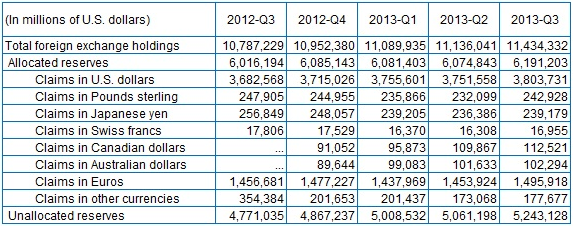

There is one possible positive for sentiment. We know that central banks have been adding Aussie to there reserve portfolios for a few years. That has been a significant real support to higher valuations and general market sentiment around the currency. The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) report shows the accumulation was still aggressive in early 2013:

However, it is interesting to note that as the Aussie has regained its cyclical mojo and gotten cheaper, official buying has slowed to a trickle. That does not strike me as especially committed to the cause. Buying in the twin currency in Canada has remain much stronger. That’s not to say we’ll see a reversal in the holdings. But we aren’t seeing much in the way of bargain hunting either. This has not been updated since December.

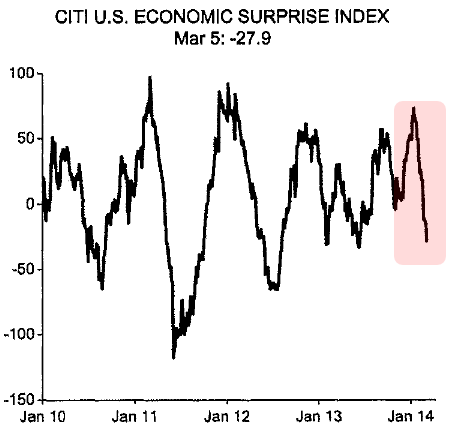

The final driver, the valuation of the US dollar, is looking weak but perhaps not for long. The turn in US data should come and, just as importantly, expectations for the recovery are suddenly muted:

As post-winter data flows, the US dollar should firm with taper expectations.

The upshot is that the conditions for Australian dollar strength are rapidly reversing. My long term view remains unchanged – downside first to 80 cents and then much lower – given I see no real recovery in Australia until its below 80 cents permanently.