Via FTAlphaville comes a take from BofAML that nicely summarises this business (or should i say “speculators” cycle):

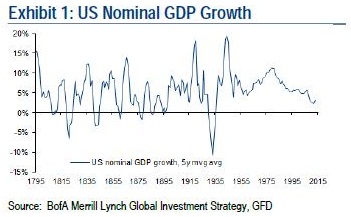

Crimea River … flowing with liquidity…We believe this remarkable bull market in equities has been built on liquidity and pessimism, not on growth and optimism. US Nominal GDP growth has averaged only 3.3% over the last five years, just up from the slowest rate of growth since the 1930s (Exhibit 1).

But a backdrop of excess debt, deflation and deleveraging has not prevented soaring asset prices thanks to a central bank policy of maximum liquidity and a corporate policy of maximum profits. Both have allowed asset prices, particularly equities, to climb a wall of worry: since the beginning of 2009 only $132 billion has flowed into global equity funds, while $1.2 trillion has flowed into global bond funds.

We believe the bull market is far from over. Neither inflation nor recession features in our macro base case. High corporate and investor cash levels are more visible than greed and leverage. And central bankers remain in “whatever it takes” mode.

…The risk to this view is simply that global or technological factors delay “escape velocity”, interest rates remain anchored at zero and excess liquidity ends up causing excess valuations in a narrow range of assets. There are eerie similarities with the 1998-99 period. Back then a series of EM blow-ups beginning in Thailand, ultimately impacted western financial markets forcing the Fed to cut rates, which thereafter ignited a tech bubble (Chart 4).

To summarise, absolutely nothing about global financial stability has changed since the GFC, except it’s deteriorated further. As I say, enjoy it but don’t believe it. Even “buy and hold” Australian fund managers can see it now:

Australian fund managers are ditching the traditional buy-hold strategy and instead looking for trading opportunities as a way to deal with the actions of central banks and gyrations in offshore markets.

Global forecasting group Create Research chief executive Amin Rajan told The Australian Financial Review in a trip to Sydney this week that local fund managers were changing the way they invest in response to client concerns about global politics, rather than economic fundamentals.

“The old way of adopting ‘buy and hold for seven years’ is fading,” he said. “There is a greater element of trading coming into play. Buy-and-hold is still alive and well, but there are a lot of other opportunities in the approach.”

…Buy-and-hold purist Aberdeen Asset Management’s head of Australian equities Robert Penaloza said that though the strategy is far from dead, the approach has changed.

“When we say buy and hold we are not talking about forever, but what we expect to see over the next three to five years.

Advertisement

That’s too far out for this cycle, sunshine. For what it’s worth, my guess is we’re currently in the early months of 2007.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.