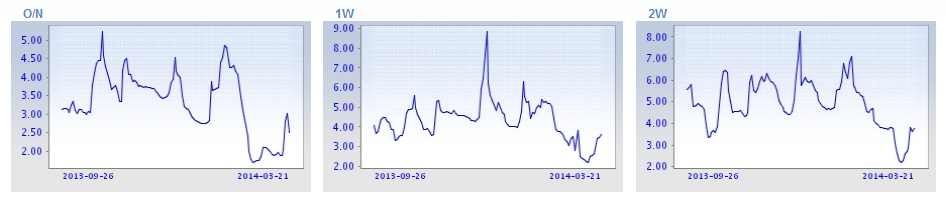

The People’s Bank of China appears to be determined to keep Chinese money tight. Last week it drained a net 50 billion yuan via reverse repo and has succeeded in tightening interbank markets closer to recent ranges:

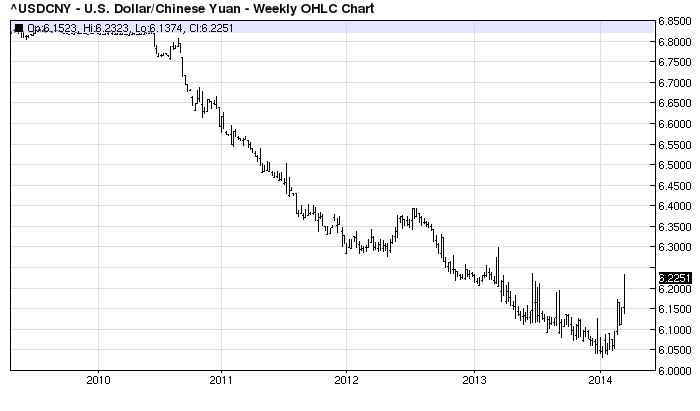

It also kept the heat on local liquidity with its falling yuan:

The jury remains out on how much of the recent loosening was the result of liquidity hoarding by the banks (the pulling back on some lending) and how much was deliberate PBOC loosening. Last week’s PBOC action may suggest the former.

My theory is that the PBOC is aiming more to squeeze the shadow bank sector – which is more vulnerable to interbank pricing and the hot money flows associated with a rising yuan – than it is the banks themselves.

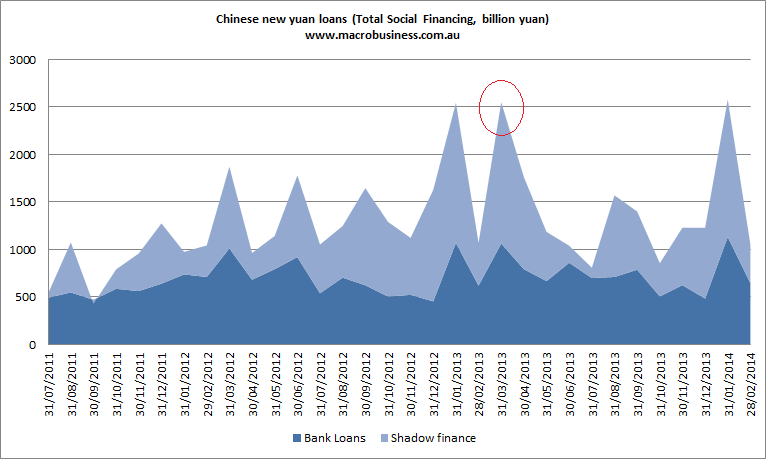

China’s March credit numbers are going to be very important. It’s working from a high base with last year a blowoff, especially for shadow banking:

A falling year on year number will be a clear message of PBOC intent to slow credit. Any increase will need to be substantial to signal the opposite.