US data was again disappointing last night and markets surged back on taper taper. The biggest release was Durable Goods Orders which showed a bounce on seasonal adjustment that appears to have accounted for the bad weather:

New orders for manufactured durable goods in January decreased $2.2 billion or 1.0 percent to $225.0 billion, the U.S. Census Bureau announced today. This decrease, down three of the last four months, followed a 5.3 percent December decrease. Excluding transportation, new orders increased 1.1 percent. Excluding defense, new orders decreased 1.8 percent. Transportation equipment, also down three of the last four months, drove the decrease, $4.0 billion or 5.6 percent to $67.3 billion. This was led by nondefense aircraft and parts, which decreased $3.4 billion.

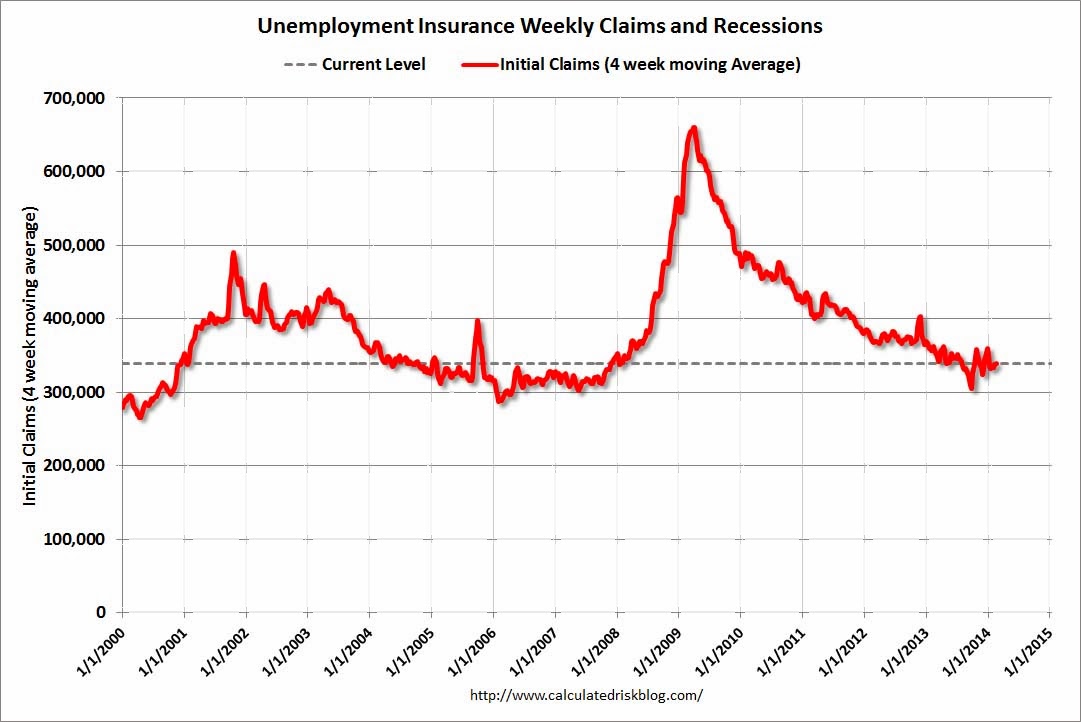

Much better the the minor fall expected. But that’s where the good news stopped. Weekly Jobless Claims were weak and show a clear taper of their own into a sideways trend (chart from Calculated Risk):

In the week ending February 22, the advance figure for seasonally adjusted initial claims was 348,000, an increase of 14,000 from the previous week’s revised figure of 334,000. The 4-week moving average was 338,250, unchanged from the previous week’s revised average.

Advertisement

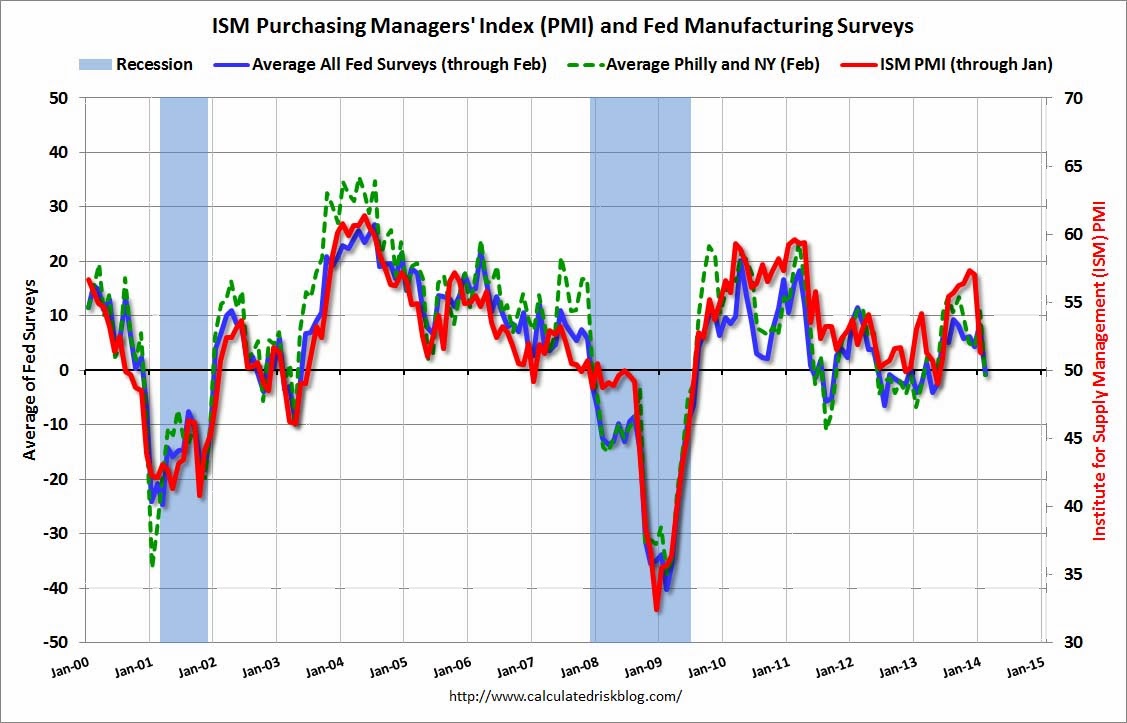

The Kansas City Fed manufacturing index came in virtually unchanged at 4 points:

The month-over-month composite index was 4 in February, similar to the reading of 5 in January and up from -3 in December…new orders, employment, and capital expenditures indexes were mostly unchanged.

As a read on next week’s ISM, the regional surveys have been weak (chart from Calculated Risk):

Advertisement

Janet Yellen appeared in Congress again and was a little more dovish. From Goldman Sachs:

BOTTOM LINE: There were few surprises from day two of Chair Yellen’s semi-annual monetary policy testimony before the Senate Banking Committee (originally scheduled for February 13 but delayed due to snow). At the margin, she indicated a bit more concern about the soft recent data, though not to the degree of signaling an end to the QE tapering process.

MAIN POINTS:

1. Regarding the recent string of weaker economic data, Chair Yellen briefly deviated from her prepared text during her introductory remarks, and noted that “…a number of data releases have pointed to softer spending than many analysts had expected. Part of that softness may reflect adverse weather conditions, but at this point it is difficult to discern how much.” Responding to a question from Senator Schumer on whether that Fed would cease tapering in light of the recent data, Yellen indicated that “if there’s a significant change in the outlook, certainly we would be open to reconsidering, but I wouldn’t want to jump to conclusions.”

2. Yellen did not clearly indicate a preference for any specific change to the forward guidance. At different points in time during the Q&A, Yellen suggested several indicators to supplement the unemployment rate in assessing the amount of slack remaining in the labor market, including the number of individuals working part-time for economic reasons, the broader “U-6” measure of unemployment, the long-term unemployment rate, wage inflation, and labor market flows. She declined to provide any quantitative information on her view of what constitutes full employment.

3. On the potential approach to managing the Fed’s expanded balance sheet during monetary policy exit, Yellen stated that “there is no need to bring down the size of our portfolio to tighten monetary policy. We have a range of tools that we can use to raise the level of short-term interest rates at the time the Committee deems appropriate.” This was consistent with past statements from Chairman Bernanke and represents a change from the June 2011 exit strategy principles. We forecast portfolio reinvestments at least until the time the Fed starts increasing the funds rate.

4. When asked about potential imbalances in financial markets due to the stance of monetary policy, Yellen stated that “at this stage I don’t see concerns.” However, consistent with past statements from Federal Reserve officials, she did highlight “pockets of concern,” including underwriting standards in leveraged lending and farmland prices.

Advertisement

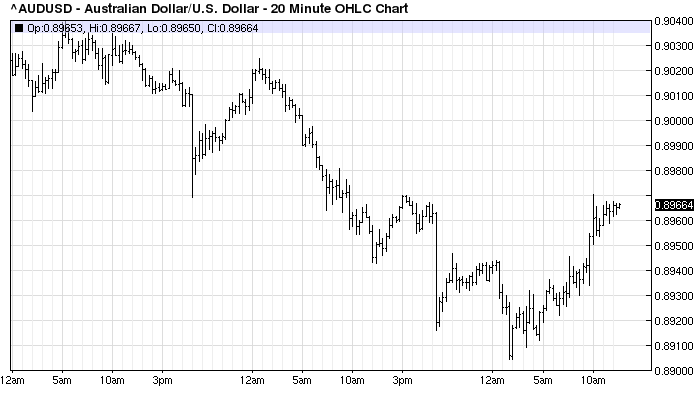

The upshot of that mix was taper taper with the US dollar losing most of yesterday’s gain, bonds being bid and yields falling 1%, gold rallying half a percent, the Australian dollar stupidly erasing yesterday’s capex dump:

And in relief to technicians everywhere, the S&P500 finally managed to close at a record high above 1850 (at least it looks like it with 20 minutes to go!).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.