It’s time to prepare for recession. That’s my opinion and there are three overlapping risks for why I think so.

Risk 1: The mining bust

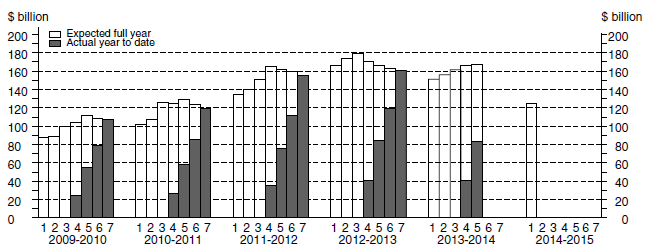

Yesterday’s capex report has confirmed the fears I’ve expressed for two years. The mining boom is not having a soft landing. It is bursting. Consider the kind of falls in business investment reported yesterday. The first estimate for business investment for 2014/15 was $125 billion:

That’s down from $166 this year. If you add a realisation ratio averaging the last three completed years you get to a total closer to $140 billion. That’s roughly a 2% of GDP fall. But, given the extent of weakness, one can rightly ask if a lower realisation ratio isn’t more appropriate. And if it is then the fall could get closer to 3% of GDP (although the blow would be softened somewhat given part of the CAPEX expenditure are imports, whereby a reduction adds to growth). In simple aggregate terms, even a more benign realisation ratio delivers a fall in business investment above 10% which is comparable to the 1982 recession and approaching 1991. Then we’ll do it again in 2015/16!

Business investment creates jobs. Without it, jobs shrink. This is an employment shock in the making, even if the reduction to GDP is offset in part by rising net exports.

Risk 2: Policy blunders

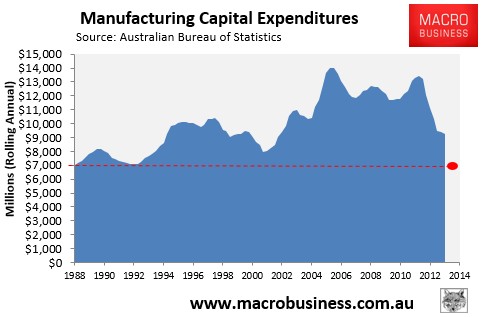

These are stacking up at an alarming rate. Going into the above our fiscal authorities have adopted a hard line on structural change in manufacturing. Letting the car manufacturers go at this stage was a big mistake. Manufacturing should be a part of rebalancing investment but is instead collapsing:

With a soft economy and lousy sales there is every chance that the auto-makers leave earlier than planned, adding to the employment and growth shock.

The second fiscal blunder is the manner in which the Government is conducting its drive to improve competitiveness (which is the right thing to do). There is little sense of management or of shared burden in the process. Rather, it looks like a long held back collapse being egged-on by a desire to destroy unions.

Related is the drive for Budget repair, which is being pursued not within a framework of collective community action as we move beyond the China boom, but via harsh rhetoric and inconsistent political favours.

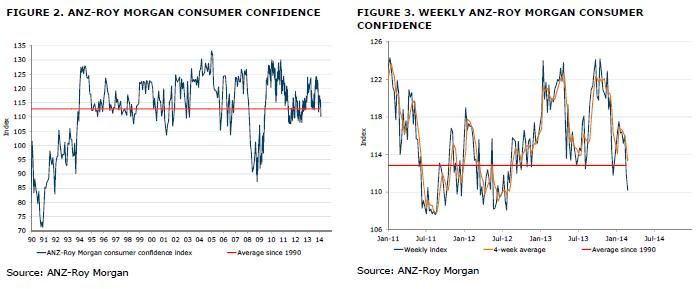

Both are going to spook consumers wrestling with rising unemployment. Indeed both already have with rising unemployment expectations and confidence plunging post-election:

The third blunder is that monetary authorities have reacted too late and haven’t innovated appropriately for their situation with new tools that dramatically lowered the dollar and released pressure on consumers without ramping risk in the housing market. As a result we have a FAR TO HIGH currency and a housing bubble on the threshold of its highest valuation in history and our only redress is to do more of it.

The Australian economy is now, and will remain so for three years, completely dependent upon rising house prices and consumption for growth. The moment they stall or fall the underlying economic weakness will present itself.

Risk 3: China

I don’t know how committed China is to reform. Neither do you. Nobody does. But it doesn’t matter, really. Australia’s situation is three years of falling business investment. If China pursues reform aggressively we’ll face a terms of trade and national income shock in the next year.

If China slows the process down and allows credit to run, it’ll probably endure some kind of financial crisis within the three year time frame anyway. Either way, the risk is that Australia faces significant falls in the terms of trade and an income shock at some point while business investment is still falling.

Conclusion

I’m not forecasting a recession. Aside from anything else, it’s true that headline growth will get a lot of support from net exports and there is room for more rate cuts, as well as government spending. There’s the population ponzi too which means growth per capita has to go backwards almost 2% to even register as a headline recession. Although, if times get tough, it too will stall.

But that doesn’t mean as individuals we can’t get poorer – via rising unemployment and falling real income growth – even if the authorities are happy to bury the fact.

I am simply pointing out that the risks above are very real and as such an investment posture incorporating an unusually high chance of recession is appropriate. I am making this call early and nimble investors may not heed it but for the slower moving it’s better to be preparing on the up slope not the down. That means exiting or avoiding positions in illiquid assets, avoiding exposure to cyclical businesses and hedging via the currency which is going to fall a long way if things go pear-shaped.