JP Morgan deconstructs bitcoin today:

Unlike other asset markets, FX rarely welcomes newcomers for the simple reason that launching a widely-used currency traditionally required creating a sovereign or supra-sovereign entity with a central bank to issue the unit and manage its supply over time.

Hence the audacity of bitcoin: it is a stateless, virtual and peer-to-peer currency, so exists only digitally and is associated with no sovereign, central bank or bank payments system. It is also incredibly illiquid extremely volatile and often caricatured.

After a brief Economics 101 refresher on the required functions of money, this research note addresses various frequently-asked questions around this virtual currency: what is it; how is it created and transferred; what are its advantages and disadvantages for corporates and investors compared to fiat currencies; is it a serious contender for a global payments system; and can it prove more durable long-term than other somewhat fixed-supply currencies like gold.

At the risk of sounding like a luddite, bitcoin looks like an innovation worth limiting exposure to. As a medium of exchange, unit of account and store of value, it is vastly inferior to fiat currencies. Since governments are quite unlikely to accord it the status of legal tender, bitcoin or other virtual currencies would not reach the scale and scope to render them worthwhile for widespread commerce, payments or investment.

Bitcoin’s greatest appeal is the apparent cheapness of peer-to-peer fund transfers, though it is unclear how economical these transactions truly are when the virtual world interacts with the real world. As provocative as its underlying technology may be, bitcoin’s practical role may be no larger than that of an emerging markets currency subject to exchange controls.

For corporates, bitcoin’s appeal is two-fold: no or low transaction costs from a peer-to-peer payments system, and the potential brand recognition from trialing a new technology. These advantages must be weighed against extreme illiquidity and volatility, both of which impede risk management. All-in transaction costs may also be higher once the fees from transferring bitcoins to fiat currencies are included.

Investors normally avoid an instrument with bitcoin’s trading properties. The unit’s main investment appeal is the potential long-term price rise due to limited supply, much like some commodities when the market balance tightens.

At the risk of out-Ludditing JPMorgan, my own view is that all of these virtual currencies are crypto-Austrian ponzi schemes concocted by techno-anarchists. Bitcoin is a pyramid of limited supply underpinned by global demand for something that has no legal value and very likely never will given it threatens the core of what makes every government, everywhere, tick.

Now there are technical risks too:

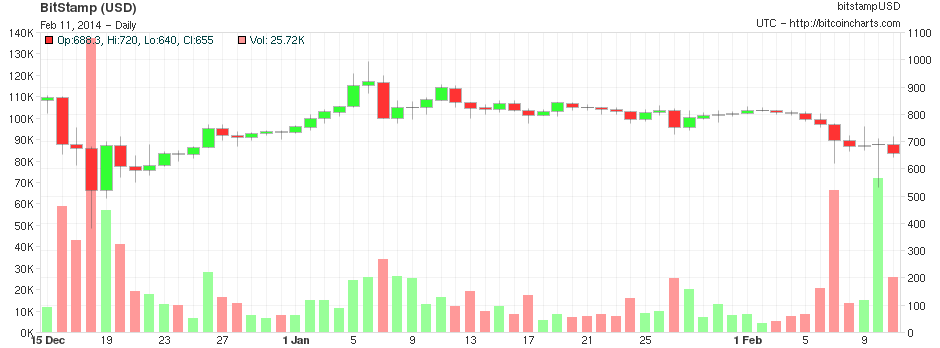

A software glitch, enabling Bitcoin traders to effectively defraud exchanges, has prompted a severe war of words – between the currency organisation and a Japanese trading venue that questioned whether the core messaging technology is fit for purpose.

Yesterday, the price of Bitcoin, the innovative yet secretive virtual currency reportedly used by some traders for illicit activity, dived by 16 per cent after exchange Mt Gox said there was a “bug” in the Bitcoin software.

The Bitcoin Foundation has rejected the comments, insisting that Mt Gox experienced its own technical problems and was not ready for a well-known messaging risk.

Enter at own risk!