Fresh from the excellent Elliott Clarke at Westpac:

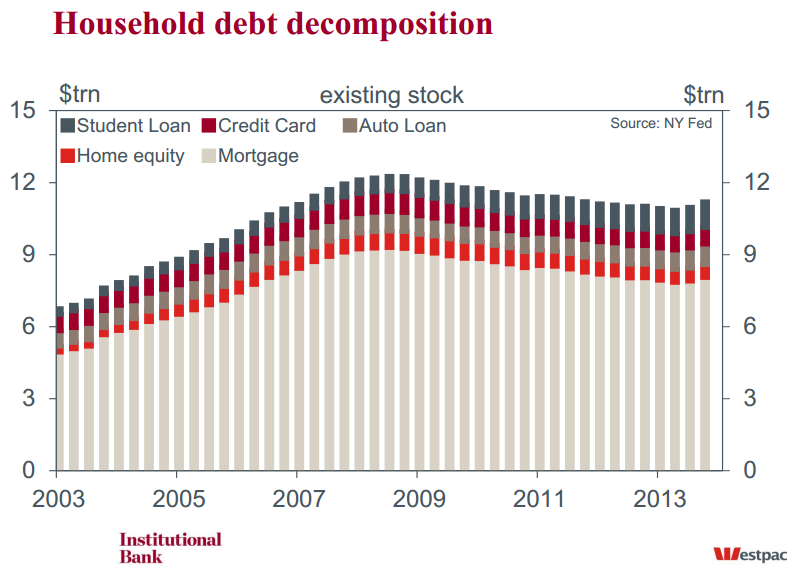

Throughout 2013, we highlighted the usefulness of a relatively new quarterly credit report for the US economy produced by the NY Federal Reserve. Last week saw the release of the February edition of this report, which includes data to the end of 2013.There were two key themes in this issue: the first being that 2013 was the first year since 2008 which saw an increase in household leverage; the second was the composition of this debt, both with respect to the type of credit and the credit standing of end borrowers.

According to the NY Federal Reserve, aggregate consumer debt increased by $241bn in the final quarter of 2013 (+2.1%), taking the annual change for 2013 to $180bn (+1.6%). While mortgages were the primary driver of debt growth in the December quarter, for 2013 as a whole, student and auto loans were the primary contributors – $114bn and $80bn respectively versus a $4bn increase in credit card debt and an $18bn decline in housing debt. These headline results suggest well established households remain unwilling to increase their leverage in a meaningful way, while younger individuals remain focused on improving their education.

Typically we are unable to get disaggregated data to confirm this thesis. But thankfully a one-off article accompanying the February credit report not only allows us to investigate credit growth by age group and loan type, but also by the credit standing of each borrower.

From the available data, it is clear that the vast majority of student debt is accrued by those who are less than 30 years old (69%). Individuals between the ages of 30 and 39 borrowed 15% of total student debt in 2013, with the remainder of the debt borrowed by those aged 40 or above. For the latter group, whether they are borrowing for their own education or that of their children is unknown.

For the other key growth area of 2013 (automotive loans), we see a similar albeit more balanced profile across the age groups. Specifically, 35% of new auto loans went to individuals below 30 in 2013; a further 25% went to those aged between 30 and 39. For both groups, auto debt accrual was disproportionate to their share of the total number of borrowers, 16% and 17% respectively. For the 40 to 49 age bracket, the amount of auto debt accrued was more in line with their share of total borrowers, 21% of debt versus 17% of borrowers. That younger individuals would need to borrow more is not particularly surprising; however, it also stands to reason that lower incomes and existing student debt would make any given loan more difficult to pay back, all else equal.

Turning now to the statistics on borrowing by credit score, we find that it is the lower-rated groups which have been doing the borrowing. Overall, 27% of borrowers have a sub-prime rating (<621); a further 17% have a ‘fair-to-good’ credit rating, between 621 and 680, while 27% of borrowers have an excellent rating, in excess of 780.

What is perhaps more interesting though is when we assess the credit health of the different age groups. Specifically, for those less than 30, 38% of borrowers have a sub-prime rating, and a further 29% of borrowers’ ratings fall into the ‘fair-to-good’ range. Of borrowers between 30 and 39, 41% have a sub-prime rating and an additional 18% fall into the next range up.

While it is to be expected that younger borrowers will have a lower credit rating (because the length of an individual’s credit history and the diversity of their debt portfolio form part of their score), an individual’s payment history and the amount owed (relative to existing limits) are the more crucial factors. The credit attributes of the 30–39 age group noted above, and indeed that of the 40–49 group (34% sub-prime and 17% ‘fair-to-good’), emphasise that weaker ratings arguably primarily stem from the interplay between significant legacy liabilities and soft wage and job outcomes. It is important to note that the same analysis conducted for 2006 suggests there has been little change in either the share of borrowers in each age group or credit category over the past seven years. What has changed is the ability for borrowers to pay down this debt and to access additional forms of financing in the intervening period.

Specifically, while student and auto debt remains available to borrowers of all credit standings, this is not true of mortgage finance for which credit scores matter a great deal. Hence, the impulse to a recovery often provided by household formation remains worryingly latent some five years on from the recession’s end. As for the long-term fiscal position (discussed last week), greater job creation and real discretionary wage growth are necessary if we are to see a persistent strengthening in household demand in the short-to-medium term. Without this, the legacy liabilities of households and their impaired credit standing will remain an enduring burden.

Full chart pack here.