FTAlphaville carried some important analysis on Friday about US inflation and the prospects for further rises in bond yields. From HSBC’s Steven Major who reckons short-term yields can only go lower:

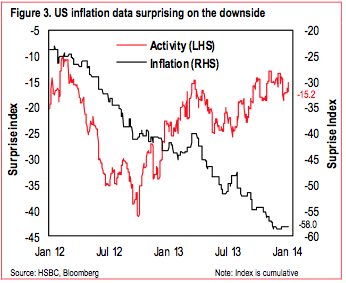

As if understanding the term premium wasn’t enough, the two supposedly predictable contributors to nominal yields – growth and inflation – have been moving in opposite directions. Whilst it is true that the real economic data has been showing an upside surprise, there has been an equal move in the other direction from inflation (see Figure 3). Furthermore, the downside surprises have been evident in most developed markets, with the exception of Japan. The conventional approach to rising growth would be to expect an inevitable future rise in inflation as output gaps are closed and capacity constraints are reached.

This seems to be the thinking behind the forecasts for higher yields. But what if today’s disinflation is a signal of future weakness in the economy? This was highlighted in the Fed’s minutes, and ‘a few participants raised the possibility that recent declines in inflation might suggest that the economic recovery was not as strong as some thought’.

Given the above, the Fed’s attention could soon turn away from the employment rate and over to inflation prints as a result.

According to Alphaville, Barclays agrees:

At the December FOMC press conference, Chairman Bernanke noted that “the Committee now anticipates it will likely be appropriate to maintain the current federal funds rate target well past the time that the unemployment rate declines to below 61⁄2 percent, especially if projected inflation continues to run below its 2 percent goal”. He noted this reflected the view that considerable slack will remain when the UR is at 6.5%, as well as the fact that inflation was low and that “the committee…anticipates keeping rates low at least until it sees inflation clearly moving back toward its 2 percent objective”. We believe that the labor market slack (and the unemployment rate) will likely keep falling faster than current Fed and consensus expectations. Hence, the labor market slack will gradually become less of a justification for keeping policy as accommodative and the burden will shift to the inflation outlook.

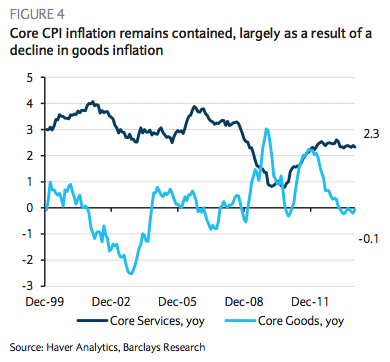

…Recently released inflation data also do not point to a sharp increase in the short term. Core PPI consumer goods inflation has been 1.4% over the past six months, which, while above the recent lows of 0.8%, is still below the levels early in 2013 of close to 2.2%. Pipeline pressures seem to be just bottoming out. The latest CPI print continued to show modest core goods inflation (which accounts for ~ 25% of core inflation and is at -0.07% y/y) and core service inflation of about 2.3% y/y, not strong enough to pull overall core inflation above 2% (Figure 4). The inflation swap market is also pricing in y/y CPI inflation of 1.4% in 2014 and 2% in 2015, with PCE inflation, say 30bp lower, at about 1.7% for 2015. Hence, while the Fed is likely less optimistic about the labor market outlook, its inflation outlook is not out of sync with the market to justify the market trading the path of short rates significantly away from the Fed’s latest rate guidance.

Readers may recall that my own view has been that the path of Fed tightening will be much slower than markets currently expect (it has been so consistently since the GFC) as the US recovery continues to grind ahead rather than accelerate. Low inflation is consistent with this view despite a slowly improving labour market.

Note that in the chart above, the two recent spikes in US inflation (in light blue) have not been wage cost related. They’ve been commodity price related (as an input cost into goods). If you overlay Australia’s terms of trade with the light blue line they are very correlated. Exploding commodity prices were behind the last two global inflation surges, in 2008 during the great China surge and in 2010 owing to the MENA and food crises.

The reasons for this are pretty well understood. The disinflation emanating from cheap Chinese and emerging market goods production has ensured plenty of slack in Western labour markets as well as imported deflation. But the emerging market rise has driven huge inflation in commodity prices, which are supply inelastic.

So, if you want to forecast the path of inflation in the US, you should be looking at China, and on that front the news is largely good. China’s own rebalancing process is itself very deflationary, as we can see in its persistently low CPI and PPI prints. In time, yes, household incomes in China must accelerate and that may cause goods prices to rise eventually. But in the mean time China’s huge industrial overcapacity has to consolidate creating powerful downward price pressures, especially in the commodity complex that it supports.

Add to that the huge supply response unfolding in industrial commodities generally, and the likelihood of a secular trend towards cost-out deflation in mining, and you’ve got a long term lid on global inflation.

That means a slow tapering and/or markets that have a little reason to raise short term rates.

The long end is a different story. The 10 and 30 year bonds in the US is where the Fed has been actively buying. As it pulls back, yields may rise irrespective of anchored short rates. That’s an argument for curve steepening based upon what is essentially an unwinding bubble of safe haven long bond buying. That’s been my base case and it’s too early to shift it, though the low inflation thesis is an argument that I’m paying attention to, especially since neither the 30 year nor 10 year yield have managed yet to break their recent highs just below 3% and 4% respectively.

None of this, it seems to me, changes the bullish argument for US stocks. If bond yields do break down then the weaker growth that that implies should keep the Fed on hold and US stocks will be bid. If yields remain firm then stocks will be bid on the promise of growth and the Fed slowing its taper to contain bond vigilantes. Either way, US stocks remain the other repository of contemporary inflation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.