Cross posted from Prosper By David Collyer

The weighted net annual rate of return on land investment in Melbourne 1880-92 was a remarkably high 34.6 per cent, peaking at 78.3 per cent in 1887, according to a fascinating paper researcher Philip Soos has unearthed Rates of Return on Melbourne Land Investment 1880-92 by doctoral candidate Ron Silberberg[i] of Monash University in 1975.

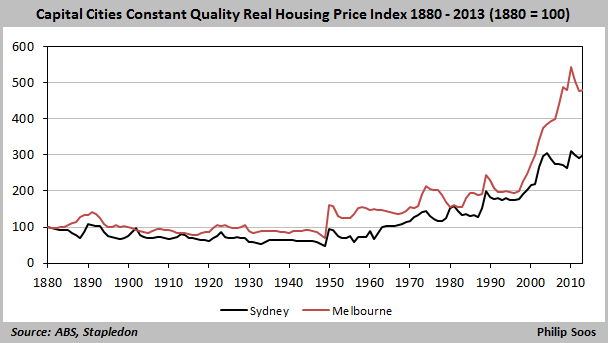

Land prices move in very long cycles. The largest complete bubble episode in Australia’s short history should be studied carefully by all in the land market. Soos’ chart of Australian Constant Quality Real House Price Index 1880-2012 is an excellent place to begin.

{kind=link}

During the period 1880 to 1892, the group of Melbourne investors Silberberg studied held their property for 3.7 years on average before realizing a sale. After 1884, many investors bought land purely for the purpose of lot sub-division (14 per cent of sampled observations), with the allotments in preferred and populous suburbs keenly sought due to the expectation of ongoing price rises that would allow investors to flip the property later for a quick profit. Some of the greatest gains in Melbourne land prices were seen in the 6 to 7 mile radius from the CBD. Many land investors were purchasing semi-rural land with the expectation a future change in land use would gift them a large windfall.

By late 1888, it was patently obvious that ‘the supply of land offered vastly exceeded demand’. Indeed, in November 1888, the Journal of Commerce commented:

‘A very simple calculation of the number of allotments reported to have been sold in the last 12 months, will show that with a population of a million, provision has been made for five millions.’

Silberberg: Average returns after 1884 declined slightly until 1887 and thereafter fell dramatically, becoming increasingly negative after 1888. Two factors contributed to declining profits in the land market. First, after 1888, many investors found themselves in illiquid circumstances and, being unable to fund buyers to purchase their land at increased prices, were in many cases forced to sell at a loss. Second, many mortgagors chose to default on their debts once it became clear that the prospects of land sales were remote except at a loss, while falling land values after 1890 reduced the proportion of equity in their land. The returns for the years 1888 and 1889 demonstrate clearly that buying land after the rapid growth phase had taken place could result in substantial losses to speculators.

…..

Once the expectation that land prices would continue to increase became built into the speculative process, rising levels of demand for land ensured high returns for investors. This expectational optimism contributed in an important way to a belief that the profitability of real estate investment was irreversible. The anticipation of continued land price inflation or confidence in the economic growth of an area was the cornerstone for many a favorable investment result. However, as more and more investors entered the market and demand was satisfied, numerous investors with mortgage-financed properties eventually lost their investments in the years of land market depression, or were forced to be satisfied with low rates of return.

Many property ‘bulls’ with little sense of history are quick to shrug such an episode off, until it is pointed out both Melbourne and Sydney house prices did not recover their 1888 values in real terms until 1950.

Yes it is different today. Now we have banks willing to lend a lifetimes’ income to anyone with a pulse. We have zoning rules to ration and inflate the price of periphery land. We have a tax system that nets minnows and lets big fish pass unhindered. We have a Reserve Bank determined to sustain the bubble with emergency interest rate settings.

One thing unchanged from 1888 is the urge to speculate, to project the gains of the recent past into the future. Yet prescient forecasters would say the most likely future path is ‘revert to mean’. This is not a party to be fashionably late for.

Don’t Buy Now!

Further reading: I highly recommend The Land Boomers by Michael Cannon Melbourne University Press 1966, extended and republished 1995.