Fresh from Fitch’s newly released Global Housing and Mortgage Outlook, 4% growth for the Australian housing market in 2014:

Australia

House Prices: Continued House Price Growth

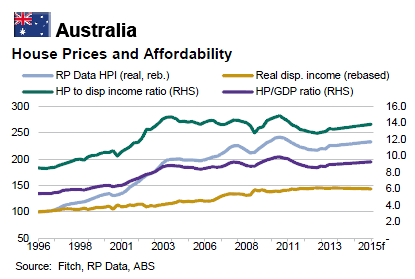

House prices in Australian capital cities rose 11.8% in the 19 months to December 2013. This followed a decline of 7.4% in the previous 19 months to May 2012 (see overleaf). This was mainly a consequence of the Reserve Bank of Australia‟s (RBA) continued cutting of the policy rate to 2.5% from 4.75% between October 2011 and August 2013.

Data from the Australian Bureau of Statistics (ABS) show that in recent years, the supply of new residential properties is running at below longterm averages. At the same time, population growth has been above long-term averages, through both natural growth and increased immigration. There is speculation about undersupply to support prices, although this might not be true for all regions.

Fitch expects continued house price growth of 4% in 2014, although some cities may remain flat. Price growth in Sydney, Melbourne and Perth is likely to continue, though at a slower rate. Affordability: Short-Term Outlook Relatively Strong and Stable Australia, like comparable countries, has seen a steady rise in household DTI levels over the past decade. On a relative scale, the Australian market appears expensive; however the combination of

moderate long term growth and the RBA cutting the policy rate over the past 24 months has eased pressure on affordability levels.

Fitch expects overall affordability metrics to remain stable in 2014 due to the continued low interest rate environment, although cities with strong house price growth in the past 12-18 months may start to experience some affordability pressure.

Mortgage Rates: Little Change Expected in 2014

Mortgage rates are low by historic standards as the RBA policy rate has been further reduced from 4.75% to 2.5% in the 24 months to end 2013 in response to the weakening global demand and peaking in resource investment. Lenders have not passed on the full decrease to discretionary ‘standard variable rates’ (SVR) in an attempt to maintain margins as cost of funds have risen, however, the majority of borrowers have benefited from a discount to the SVR. The average discounted SVR now stands at 5.1%vs. 6.8% 24 months ago.

Fitch expects current mortgage rates and the RBA policy rate to be broadly maintained in 2014, as The RBA guards the economy against the reduction in resource investment and focuses on stimulating the non-mining sectors of the economy.

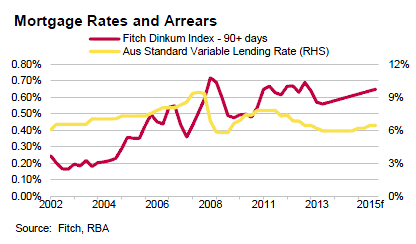

Mortgage Performance: Likely to Slightly Deteriorate

Recent quarterly data from the Fitch Dinkum Prime Index have shown gradual improvement in 30+ days delinquencies of 1.54% in 2Q12 to 1.19% in 3Q13. The improvement in arrears is driven by the low interest rate environment culminating from 2.25% of cuts in the official policy rate by the RBA to a historical low of 2.5% in August 2013 and relatively strong macro fundamentals.

Fitch expects arrears rates to deteriorate slightly through 2014, in line with projections of slower economic growth and higher unemployment. Fitch expects the unemployment rate to rise from 5.7% to 6.2% in 2014 due to the slowdown in economic growth, with Australia‟s real GDP to grow by 2.8% in both 2013 and 2014.

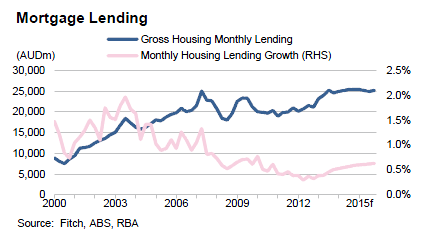

Mortgage Lending: Steadily Growing

Mortgage lending has increased slightly with net mortgage lending averaging 5.0% over the 12 months to October 2013 compared to 4.7% in October 2012. The increase follows a pickup in housing activity in the second half of 2013 as a result of the low interest rate environment. Housing debt as a percentage of disposable income was 134.1% in 2Q13, which has been relatively stable since the last house price peak in 3Q10.

Mortgage lending growth has been driven by investors and existing owner occupiers. First time buyer activity has fallen to historical lows reflecting the increasing house price to income ratios. Fitch expects lending net volumes to continue to grow steadily due to increasing levels of activity in the housing market. Borrowers are expected to continue to be cautious with higher than average household savings being maintained.

Prepayments: Increase Slightly

Mortgage prepayments have declined over the last two-to-three years to 20%-25% from 25%-30%.

Given the slight increase in transactional activity in the Australian housing market, slightly higher levels of prepayment of existing mortgages are expected in 2014.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.