Via FTAlphaville comes this from BofAML’s Bin Gao on China’s shadow banking:

The last-minute deal saved a CNY3bn trust product which we expected a high probability of default. The deal will redeem investors’ principal, dollar for dollar, but it won’t pay the back coupon missed last year, amounting to 7.2% of principal. In that sense, this deal constitutes a debt work-out, a technical default, with investors suffering a small default loss.

Our economist expects this case and subsequent few to have little impact on China’s growth, forecasted to be 7.6% for 2014.

As a rate strategist, we are more interested in examining a set of scenarios, and what we see unsettles us.

We will be more specific: the bailout looks very much like the Bear Stearns moment.

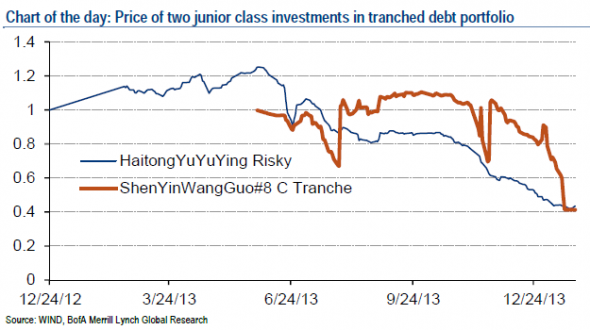

…The evolution then follows with risky debt investments losing value fast. In the US, it started with subprime mortgage funds. In China, leveraged junior tranches of managed debt products are experiencing the same problem, due to a combination of higher rates and fear of worsening credit quality of the underlying names; a few have lost half of its value in the last six months. Cases in point: Haitong’s yueyueying risk-tranche and ShenYinWanGuo’s #8 tranche C have lost more than 60% from its recent peak…

It then goes with the failure of financial institutions. Just like we would never know what would have happened if Bear Stearns was not bailed out, we will never know what would have happened if China Credit Trust (CCT) had to foot the bill of CNY3bn to pay back trust investors. Although the company has CNY10bn net asset, CCT only has CNY3bn liquid assets with CNY1.35bn short-term liability; hence, it would find it difficult to pay the CNY3bn in full. The contagion effect could be quite strong. The company’s CNY10bn equity supported CNY271bn in trust assets as of 2012. At AUM/equity of 27 (as of 2012 and likely higher in 2013), the company actually has one of the lowest leverage ratios. The average AUM/equity of trusts companies is 43 to 1 by 3Q13 with the worst having their ratios rising up to the three-digit territory. In our view, it is only a matter of time before some of these institutions fail.

The FT proper then asks the question, will this lead to a new Lehman moment?

A wealthy pensioner in a southern Chinese city deciding to lend money to a troubled coal miner in the country’s north about which she knew next to nothing might seem a dangerous gamble.

…In the case of Credit Equals Gold No. 1, ICBC clients invested a total of Rmb3bn in a product sold by China Credit Trust, one of the country’s biggest “shadow banks”. The product, a mere sliver of China’s $1.2tn trust market, was underpinned entirely by loans to and equity in coal miner Shanxi Zhenfu Energy Group. It was a rotten investment: the price of coal plummeted and Zhenfu collapsed under the weight of heavy debts.

This is something that policy makers are struggling with. The final solution has probably reinforced people’s perception that trust products bought through banks will be bailed out…There was little detail about where the money came from, but Chinese media have reported in recent days that a bailout was likely to involve ICBC, China Credit and the local government.

…The last-minute rescue raises a thorny question for the future of the Chinese economy. Has the deal confirmed the widespread belief that the government will do whatever it can to stave off trouble, hence fuelling more risk-taking? Or has the near-default taught investors that high yields come with high risks?

Advertisement

That is the Minsky question. Have we reached the point at which fear overwhelms greed and older debts can no longer be funded by new ones? It’s an investment timing question to which nobody has the answer. Clearly not, according to the latest lending data:

In a macroeconomic sense it doesn’t matter. The AFR has it right:

Advertisement

At the very least, global markets are in for a rocky ride this year as each new prospective trust loan default in China sparks fears of a financial crisis.

UBS economist Wang Tao says a banking crisis is unlikely as Beijing can force banks and other financial institutions to stand behind their wealth management products. It can also react to any liquidity squeeze by easing regulations in the formal banking sector to boost lending.

Yes, but they can’t do that and rebalance, only making the problem worse. Whichever path they choose – bailout or liquidation or some combination of the two – it will mean that growth slows down, especially in the former red hot sectors.

Continuing the US sub-prime analogy, China’s equivalent of toxic assets will be those that over-invested in fixed assets and the industrial capacity that fed them. The contagion includes anyone invested in the Australian mines shipping steel-making ingredients.

Advertisement

It’s quite an historic irony. The Chinese built an export machine based upon US sub-prime abundance. When it imploded, taking the export machine with it, authorities responded by unleashing a credit stimulus that recreated the very shadow banking mechanisms at the heart of US sub-prime.

Australia built an export machine based upon China’s sub-prime abundance and as it slows authorities here are responding by unleashing a credit stimulus…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.