Regular readers will recall that MB uses a “five drivers” model of Australian dollar valuation.

In one sense, revisiting those drivers for a 2014 forecast is not very sensible. Forex markets are more dynamic than that. But it is also true that the drivers will determine the valuation trend over the longer term so they are worth consideration. They are:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth);

- investor sentiment and technicals; and

- the US dollar

For the year ahead, my view is that there is very little chance of local interest rate hikes with falling terms of trade, the capex cliff and a soft labour market likely outweighing the investor mania in housing. Interest rate markets are now pricing 8bps of cuts in the next twelve months after a period of foolhardy flirtation with rate rises:

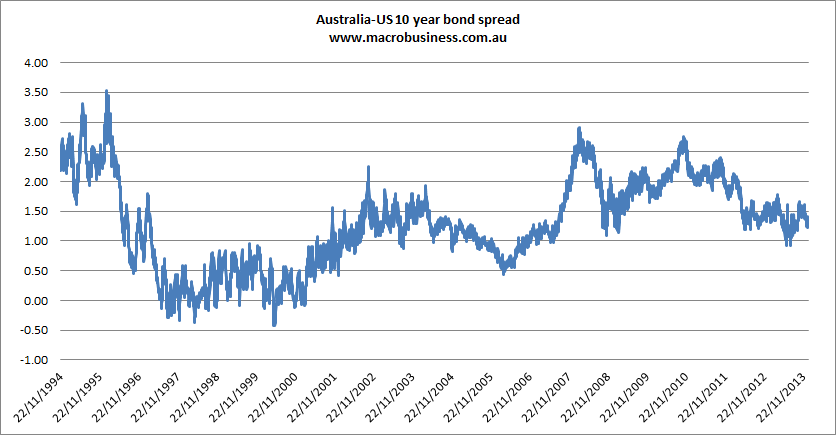

On the other hand, we will likely see slow tightening behind funding currencies like the US dollar with taper probably to move slowly forward. That means the carry spread between Australia and US ten year bond will remain stable or narrow further:

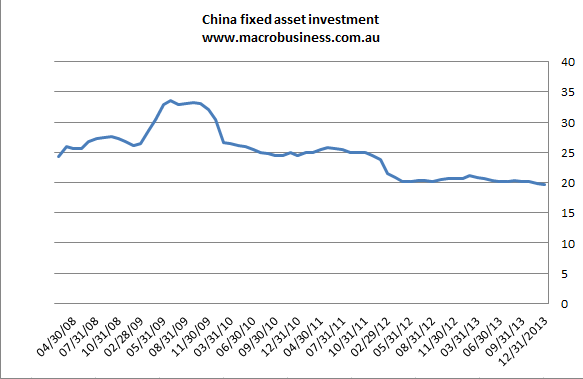

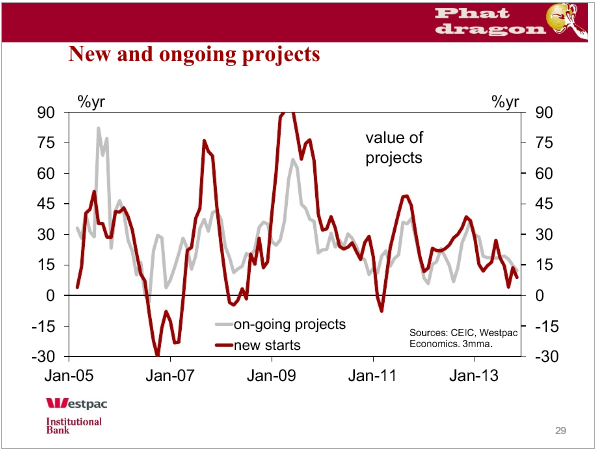

On driver two – global, local and Chinese growth – we face something of a dichotomy. Global growth may accelerate this year but Chinese growth is going to slow over the next six months to 7% and go lower if the rebalancing process is allowed to run its course. Yesterday’s quarterly data was decent but the miss in December investment – the commodity centric component of growth – is a harbinger of more to come:

The emptying fiscal stimulus pipeline is manifest:

Australian growth will follow suit. All things being equal, I expect another year of sub-par growth in the 2% range as the capex cliff, falling terms of trade and national income outweigh the cyclical forces of monetary and fiscal stimulus. On the other hand, the US and global economies aught to chug along closer to 3% this year, faster than Australia.

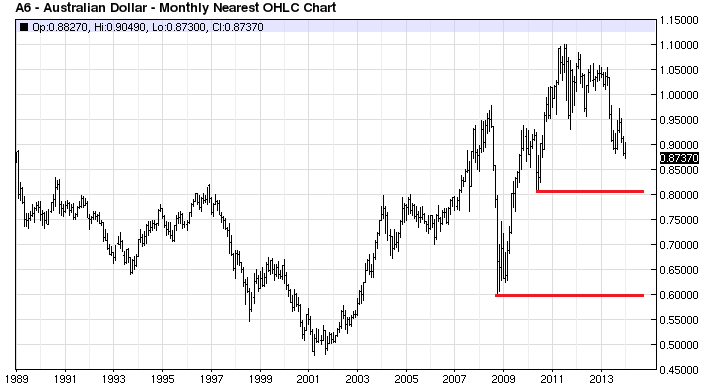

Drivers three and four are also weak for Aussie dollar bulls. On the monthly chart, technicals show a clear break of support in the mid 88’s with no apparent defendable level until just above 80 cents. Beyond that, it is clear air to 60 cents:

Turning to sentiment, the Commitment of Traders report is showing a clear preference among large and small speculators to be short:

There are ebbs and flows but this has consistently been the case for 8 months. I would not underestimate the impact of the RBA on sentiment, either. More and more voices are calling for unorthodox policy intervention and the jawbone is clearly deployed. It will continue this year and if housing rallies further it is my belief that the RBA will first talk up and then act upon macroprudential tools. As well, as I wrote yesterday, the great iron ore correction appears to be upon us and that will do Australian dollar sentiment no favours.

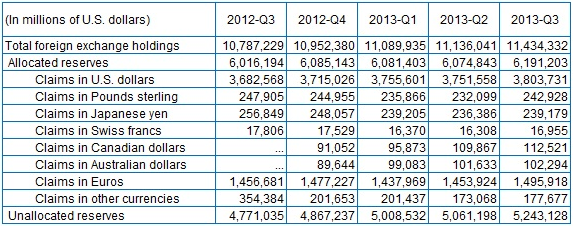

There is one possible positive for sentiment. We know that central banks have been adding Aussie to there reserve portfolios for a few years. That has been a significant real support to higher valuations and general market sentiment around the currency. The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) report shows the accumulation was still aggressive in early 2013:

However, it is interesting to note that as the Aussie has regained its cyclical mojo and gotten cheaper, official buying has slowed to a trickle. That does not strike me as especially committed to the cause. Buying in the twin currency in Canada has remain much stronger. That’s not to say we’ll see a reversal in the holdings. But we aren’t seeing much in the way of bargain hunting either.

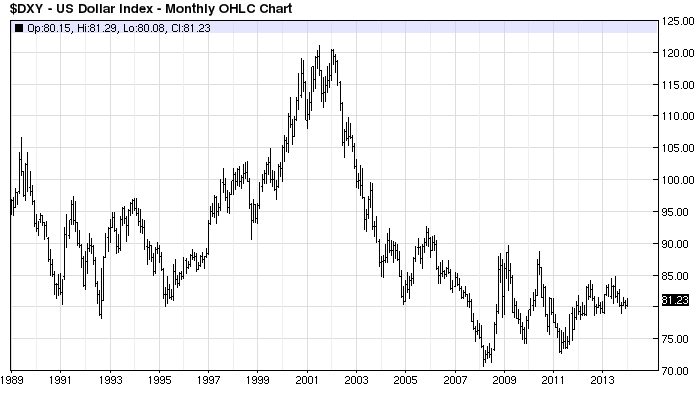

The final driver, the valuation of the US dollar, is looking firm if not overly bullish. Here’s the long term monthly chart:

I’m not sure I see any great upwards momentum for the US dollar this year but it should at least remain steady as growth and tapering grind on, the Budget deficit narrows further and equities remain buoyant.

The upshot is that I reckon we’ll get close to the 80 cent support level this year. Longer term I would not rule out a retest of 60 cents. Markets generally overshoot and I’m of the view that we’ll need to see an eye-popping price to convince what’s left of Australian non-resource tradables that their time has come again.