Deutsche has a new note this morning asking this question and the answer is discomforting:

Fed policy/change in fixed income flows could be key driver for bank stocks

While the timing is uncertain, most expect the Fed to slow its bond purchase program soon (i.e. taper) and will likely eventually stop it altogether. In addition, fixed income flows have turned negative and seem unlikely to return to the robust levels seen in recent years anytime soon.Benefits of $800b/year of Fed buying/fixed income flows going away

Since QE3 began a little over a year ago, the Fed has added ~$1 trillion to its balance sheet and $3 trillion since late 2008. In addition, flows into fixed income assets have been strong (at least until about 6 months ago), totaling $900b since late 2008. Combined, Fed purchases and investor flows have averaged $800b per year since late 2008. This has likely been a meaningful positive driver to worldwide credit and equity markets and the US banks.Near term impact of Fed taper seems likely to be negative

In the near term, the impact to markets and bank stocks is hard to predict and will likely be very dependent on macro data and the outlook for corporate earnings. On the one hand, if economic growth accelerates to the 3% consensus level in 2014 (from ~2% in 2013), additional P/E multiple expansion for banks (and the overall market) seems likely given rates remain low on an absolute basis, inflation is low and P/E multiples aren’t stretched (although are in line with historical levels). On the other hand, we worry about the potential combination of widening of credit spreads and rising interest rates; and the impact these may have on cost of funding, certain industries that are rate sensitive (like housing, FICC trading) and certain emerging markets.Who will buy when the Fed isn’t

Banks are unlikely to be big buyers given securities levels are already above average and investment banks remain under pressure to further de-leverage. This leave investors, foreign gov’t, pensions & insurance cos. However, it’s not clear if this will be enough to absorb $0.5-1.0t/yr of extra supply vs. recent yrs.

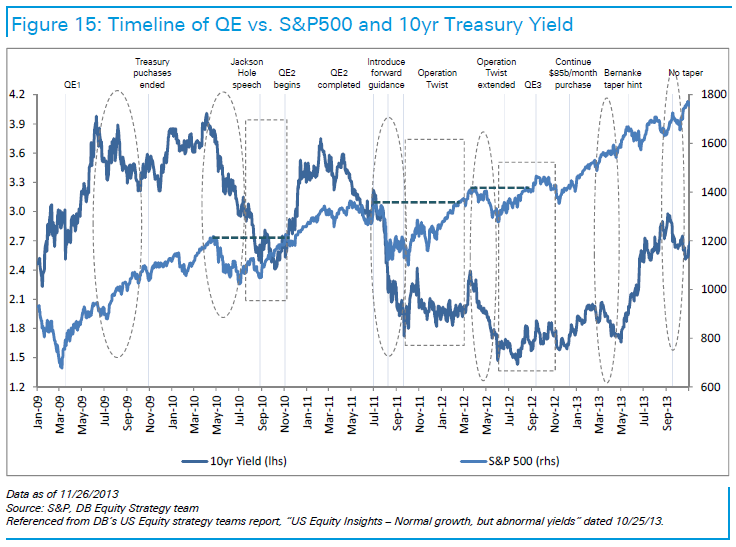

My view is that it is pretty obvious that nobody will be able to fill the hole and as such yields will rise. Here’s Deutsche’s annotated chart of the ten year bond yield:

The only period where markets did not have support from QE for any period was between late 2009 and mid 2010. That’s my benchmark for where yields will go as taper starts. 4% on the 10 year and 4.5-5% for the 30 year.

I retain my doubts that the US economy can take it.