Throughout this year, and much of last, I have been arguing two central political economy points. The first is that Australia is on the verge of an economic reckoning of a magnitude that few understand. By that I am referring to our post China boom adjustment. It is most commonly called the end of the “mining boom”. Or even more particularly the “capex cliff”. But it is much bigger than that. It is the end of a series of booms that have left our economy so bloated, and our real exchange rate so high, that we are unable to compete successfully in just about anything that is not buried in the ground or concreted into it. That is why this blog is called Houses and Holes.

The second point I’ve argued is that our economic mandarins of the day, Labor, Liberal, the executive and monetary authorities, would be serving the nation best by getting ahead of this adjustment. They should be preparing the nation for a generational belt-tightening; they should be talking down costs and talking up productivity; they should be enacting new policy settings ensuring that we preserve every potential dollar of export revenue available to the economy; they should have done whatever it took to lower the dollar; they should have innovated policy to ensure housing stayed in its box; they should have done what it took to ensure some diversity in our economic output; they should have given us all the reasons why it was needed, over and over again.

Instead we’ve gone on as if nothing has changed. The Gillard Government wasted years trying to talk up spending in prudent households; the ever so brief Rudd Government mentioned the challenge ahead but then gave into a wild series of thought bubble spending promises; the Abbott Government is new but so far it has accelerated the bailout mentality and promised wealth through house prices. Throughout all three governments, the Reserve Bank has plumped expectations of endless riches via the eternal mining boom, has re-inflated asset prices, and barely mentioned competitiveness (though it has discovered productivity lately). The Treasury has been just as bad, offering repeatedly absurd forecasts for growth, government revenue and surpluses (though it too has discovered productivity lately).

We have, in short, done absolutely nothing to prepare for what is coming. We have pretended it’s not happening in the hope that something will come along.

None of this is new but I wish to make two points today. First, this week has shown that despite our denial, the adjustment is accelerating. Throughout the last three years, MB has argued that we face a long and arduous period of below trend growth because of our multiple adjustments. And so it has proven to be:

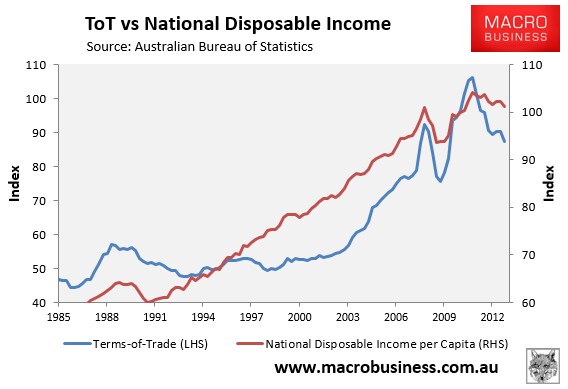

Despite a brief spike in growth in 2011/12, the post GFC period has been the lowest average growth period anyone can remember. We are now growing more slowly than the supposedly broken United States. This week’s national accounts illustrated why very clearly. The terms of trade correction which is central to the adjustment is pulling down national income:

The weak nominal growth that results has implications for the Budget, which will reveal further downgrades and larger deficits next week. Lousy income growth also makes our efforts to grow out of the funk via the old sources of asset inflation and household spending unsustainable, and it means demand is not strong enough to support many businesses, and anything tradable is being dragged under by bloated cost bases, which is what we are seeing in Graincorp and Qantas.

The second point to make today is that the response to these hard facts this week has been even greater denial. The best way forward in our situation is to let markets restructure businesses to become competitive. This should be combined with an historic national program to improve competitiveness so we preserve and build on as much that we’re good at that we can and protect the vulnerable as it happens. The RBA’s efforts to “talk down” the dollar this week are an almost laughably inadequate response. Re-structuring is the only thing that we can do to sustainably preserve our standards of living. If we just prop up dying businesses they’ll bleed us dry just as surely via falling productivity growth.

The new Liberal government has led the bailout mentality this week, blocking the Graincorp buyout, mulling Qantas rescues (though the signs are better today), agreeing to extend the GST to online retail despite it costing more than it makes and generally failing to provide a narrative that explains any of it. I have no doubt that the Labor Party would be just as bad if it were in power, strongly suggested by the winks and nods coming from across the aisle, and the clear focus of comments focusing on the preservation of jobs.

But the failure is so much wider. The press hasn’t grasped the broader trend, with much conservative commentary falling in behind Liberal Party mistakes that contravene their own principles (not all!). And the liberal press tending to discuss each issue in a silo. I’ve had more furious debates on the blog this week than at any time in three years with readers defending sectional handouts. Almost nobody is talking about or wants to confront the underlying issues.

All of this has led me to conclude that we are far less prepared for what is coming than I thought. Yet this is only the thin end of the wedge. It’s going to get much harder and many more businesses will fail under similar pressures. There appears little hope that our leaders will push the nation to get ahead of it either so each issue will be dealt with on its own terms, ensuring confusion and disaffection spreads more widely, and more businesses fail than need to.

A great shock is coming to Australian entitlement in the next three years. It’s called capitalism my friends and it’s here, ready or not.