From the AFR today comes a potent rebuttal for those of us in favour of selling Graincorp. Don Seaton is the largest shareholder in the company and argues that:

Joe Hockey’s decision to reject the proposed takeover of GrainCorp by Archer Daniels Midland (ADM) has been reported as “nakedly political”, “linked to ADM’s failure to woo growers” and its “troubled history of price-fixing”. It has been painted as a decision that buckled to agrarian socialists. It is none of these things.

The analysis conducted by my lawyers, which was presented to the government, concluded that an ADM-owned GrainCorp would have resulted in the optimisation of a global portfolio that would have prejudiced Australian interests with devastating effects on competition and the economy, not just on grain trading and exporting but also at each and every stage of the grain and oilseed supply chain.

…Hockey’s central – and proper – concern when applying the national interest test to ADM’s takeover offer was the impact on Australian industry of the dangerous levels of concentration in the grain and oilseed supply chain. If ADM had been allowed to acquire GrainCorp, it would have become the most vertically-integrated agribusiness in Australia. It would have been handed control of the vast majority of grain storage and handling facilities and all but two of the bulk port terminals in the eastern States and it would have obtained significant interests in Australian flour milling, oilseed processing and refining and malt production.

That by itself gives rise to enough concerns about vertical foreclosure.

But taken together with ADM’s powerful strategic alliances with Singapore-based Wilmar, through which ADM has access to a vast network of grain, oilseed and flour processing facilities in China and south-east Asia, foreclosure of competitors in multiple Australian agricultural markets would have been inevitable.

In other words, we’d have lost processing capacity to cheaper jurisdictions. OK then, let’s unpack this.

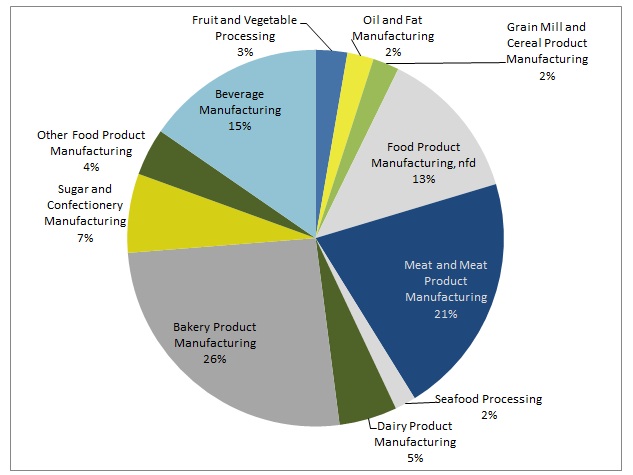

Graincorp is already a monopoly so the first part of the argument is one monopolist complaining about a second taking over his business. If Mr Seaton’s is really concerned about monopolies then why isn’t he campaigning to regulate Graincorp pricing? As well, the claims made about economic devastation are not supported by the evidence. From the Department of Industry:

2% of employment in food processing is in milling. Food processing is itself roughly 1.5% of the economy.

The second part of the argument is more interesting. If Mr Seaton is right that Graincorp’s assets are so uncompetitive then shareholders might be wondering what its board is doing. If much cheaper production for processing of available offshore, why isn’t it already being used? The argument makes no sense unless we also conclude that the Graincorp board is already failing.

I might be persuaded of the merits of Mr Seaton’s position – along similar lines as to why we should support the car industry for now – if, as nation, we were setting about addressing the real problem. That is that we can’t compete in anything that wasn’t buried in the ground millions of years ago or built into it more recently. Temporary protection to prevent the shedding of production if you’re setting about repairing the underlying problem makes sense to me.

But if we don’t address competitiveness, and we are doing precisely the opposite, then it is pointless whining about buyouts. They’ll just keep rolling in and if we keep rejecting them we’ll keep eroding our standards of living as we prop up the indefatigable rentiers.

As I wrote yesterday, free trade is largely in our interests because open market principles were enacted following WWII for two reasons. First, they tend to increase welfare (to a point) as specialisation is efficient. Second, they prevent countries that are short of one resource from invading another to get it.

To this we can add the local imperative of keeping interests at bay in all of our interests.

Crikey, I’d rather we weren’t selling the farm. I spend half my time arguing hopeless cases for fighting Dutch disease. Nothing would give me greater pleasure than to see Graincorp buy ADM. But if you tailor economic settings that destroy your competitiveness then crying to the Nanny State about buyouts is not a solution.