Let’s recall Treasury’s first attempt at self-reflection earlier this year:

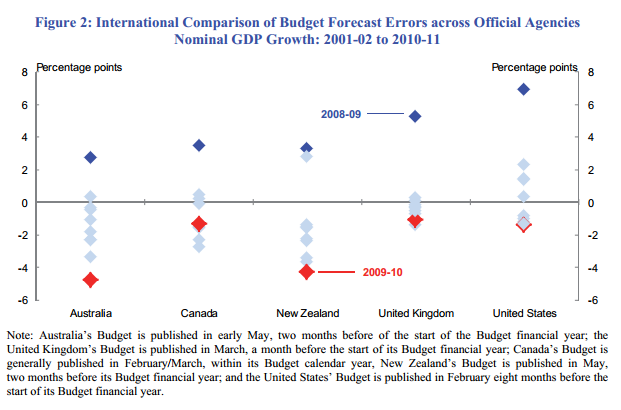

Treasury’s forecasts are comparable with, or better than, those of official agencies overseas, although some caution is required in making cross country comparisons over a period as short as ten years, and given that official agencies prepare forecasts at different times in the year (Figure 2).

That caution being that the chart clearly shows that Australian Treasury misses are larger and more frequent than anyone except for New Zealand.

Today, suddenly, new research has appeared recommending a new approach, “confidence intervals“:

Advertisement

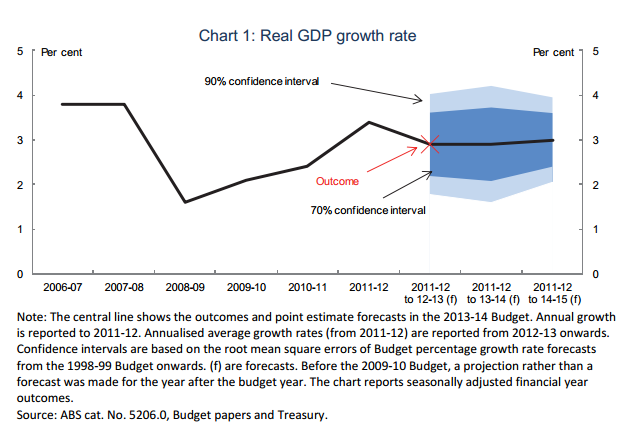

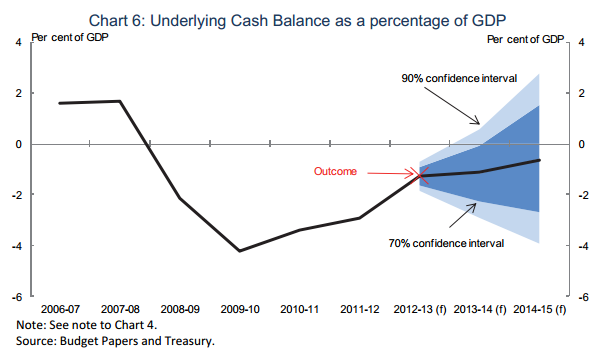

Confidence intervals provide a guide to the degree of uncertainty around forecasts. We have presented confidence intervals around key budget forecasts, which suggest that rather than focusing on precise point estimates, a more nuanced discussion would acknowledge that uncertainty is an unavoidable feature of forecasts, with confidence intervals spanning a wide range of outcomes. This is particularly true of the nominal macroeconomic and fiscal variables, for which uncertainty increases as the forecast horizon lengthens.

Reporting confidence intervals provides a way of improving the understanding of the uncertainty inherent in forecasting. Reporting confidence intervals complements existing approaches to convey uncertainty including the discussion of risks to the forecasts and sensitivity analysis provided in the Budget as well as analysis of ways to improve forecasting performance, such as that in the Treasury Forecasting Review.

The RBA has already moved this way and I have my sympathies. Forecasting is a fool’s errand, which is why we don’t bother with it at MB, but it has to be said that if you’re going to use ranges then accountability is out the window. You can successfully and simultaneously forecast boom growth and near recession:

Advertisement

Or, a huge budget surplus and enormous budget deficit:

The pollies are going to just love this. They’ll never be wrong again. Which seems to be the point. From The Australian:

Treasury secretary Martin Parkinson said it was not practical to include “error bands” around the key budget figures, such as the deficit, telling a post-budget lunch for business economists that the margin of error was too wide.

“It would probably make my life easier, because the error bands would be so large that I would only have to be up here explaining why I got it so wrong probably once in a career, not three times in three years,” he said.

The downgrading of Treasury’s forecasts following this year’s budget was sharply criticised by Joe Hockey during the election campaign and, since his appointment as Treasurer he has said budgets would in future take a more conservative approach to forecasting.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.