Today’s QE update is another mix of warnings, good and bad data. From the top, the non-manufacturing ISM was strong despite the shutdown:

“The NMI® registered 55.4 percent in October, 1 percentage point higher than September’s reading of 54.4 percent. This indicates continued growth at a faster rate in the non-manufacturing sector. The Non-Manufacturing Business Activity Index increased to 59.7 percent, which is 4.6 percentage points higher than the 55.1 percent reported in September, reflecting growth for the 51st consecutive month. The New Orders Index decreased by 2.8 percentage points to 56.8 percent, and the Employment Index increased 3.5 percentage points to 56.2 percent, indicating growth in employment for the 15th consecutive month. The Prices Index decreased 1.1 percentage points to 56.1 percent, indicating prices increased at a slower rate in October when compared to September. According to the NMI®, 10 non-manufacturing industries reported growth in October. Respondents’ comments are mixed with the majority reflecting an uptick in business. A number of respondents indicate that they are negatively impacted by the government shutdown.

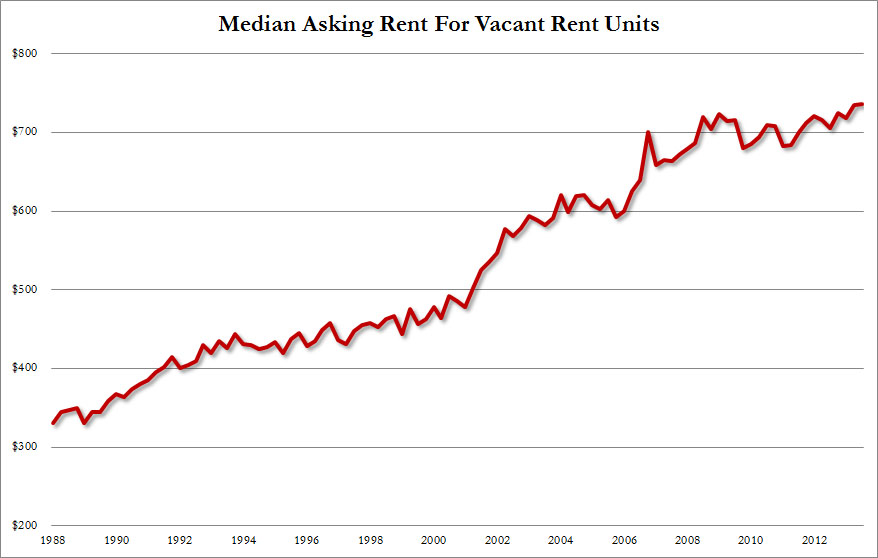

However, there were more signs of a slowing in housing markets. Rents are still growing:

But house prices are slowing, according to property data tracker, Trulia:

Nationally, asking home prices rose 3.0 percent quarter-over-quarter (Q-o-Q) in September – the smallest Q-o-Q change since February. However, the downward trend is harder to spot in the more volatile monthly changes and smoothed out yearly changes. Asking prices rose 2.0 percent month-over-month (M-o-M) and 11.5 percent year-over-year (Y-o-Y), but year-over-year changes should start to shrink in the coming months. At the metro level, 89 of the 100 largest metros had Q-o-Q price increases in September, down from 97 in June.

“Asking home prices give us the first look at where home sale prices are headed, and they point to a slowdown,” said Jed Kolko, Trulia’s Chief Economist. “After rising rapidly in the first half of 2013, asking prices in two thirds of the largest metros are cooling. In fact, asking prices are falling – not just rising more slowly – in 11 of the 100 largest metros, the most markets to see prices slip in six months.”

“Home prices are slowing down thanks to rising mortgage rates, expanding inventory, and fading investor activity, and soon we might thank the federal government as well”.

The slowdown is seasonal as well. The still impressive year-on-year growth was confirmed by Core Logic.

Here is a summary of recent data:

- The ADP employment report showed an increase of 130,000 private sector payroll jobs in October. This was below expectations of 138,000 private sector payroll jobs added. The ADP report hasn’t been very useful in predicting the BLS report for any one month. But in general, this suggests employment growth close to expectations.

- The ISM manufacturing employment index decreased in October to 53.2% from 55.4% in September. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll jobs were mostly unchanged in October. The ADP report indicated a 5,000 increase for manufacturing jobs in October.

- The ISM non-manufacturing employment index increased in October to 56.2% from 52.7% in September. A historical correlation between the ISM non-manufacturing index and the BLS employment report for non-manufacturing, suggests that private sector BLS reported payroll jobs for non-manufacturing increased by about 235,000 in October.Taken together, these surveys suggest around 235,000 jobs added in October – well above the consensus forecast.

- Initial weekly unemployment claims averaged close to 356,000 in October. This was up sharply from an average of 305,000 in September. However there were some computer problems in California, and claims in September were probably too low – and claims in October too high. So this might not be useful this month.

- The final October Reuters / University of Michigan consumer sentiment index decreased to 73.2 from the September reading of 77.5. This is frequently coincident with changes in the labor market, but in this case the decline was probably related to the government shutdown.

- The small business index from Intuit showed a small decrease in small business employment in October.

Conclusion: As usual the data was mixed. The ADP report was a little lower in October than in September, however the ISM surveys suggest an increase in hiring. Weekly claims for the reference week were higher (probably mostly due to computer issues), and consumer sentiment decreased (due to the government shutdown).

There is always some randomness to the employment report – and there are reasons for pessimism (ADP, unemployment claims, consumer sentiment), however with so many questions about the data, I’ll lean towards the ISM surveys and my guess is the BLS will report more than the 120,000 consensus jobs added in October.

And so it was that markets priced in a little more taper prospect, with equities flat and long bond yields rising 1.5% but yet to break their downtrend. Here’s the 30 year:

The US dollar was up as well marginally as well as gold down a touch.

Some of these moves were also the result of being spooked briefly when voting FOMC member Eric Rosengren made a few hawkish noises but overall his interview on CNBC was pretty dovish stuff:

The same cannot be said of another warning from a market heavy-hitter, this time private equity’s Barry Sternlicht:

A little less of a high today.

{kind=link}